Saving for initial equity contributions creates barriers to homeownership for many qualified buyers—USDA loans provide flexible financing solutions. This federally-guaranteed program through the U.S. Department of Agriculture enables eligible buyers to purchase homes in qualifying rural and suburban areas with minimal initial investment requirements, competitive interest rates, and favorable terms. Understanding USDA loan eligibility requirements, income limits, property location rules, and strategic approaches to maximizing program benefits helps you achieve homeownership while building equity in communities across America where many don’t realize this financing option exists.

Ready to explore your options? Schedule a call with a loan advisor.

A USDA loan is a mortgage program guaranteed by the United States Department of Agriculture designed to promote homeownership in eligible rural and suburban areas—the program enables qualified buyers to purchase homes with minimal initial investment while offering competitive terms, making homeownership accessible to moderate-income families in communities the USDA seeks to strengthen through increased residential development and economic stability.

Why does the USDA guarantee home loans? The program supports the agency’s mission of strengthening rural America by encouraging homeownership in less densely populated areas—increased homeownership promotes community stability, economic development, and population retention in rural and suburban communities that might otherwise struggle to attract and retain residents without accessible financing options.

The guarantee structure enables private lenders to offer favorable terms by transferring default risk to the federal government. Lenders originate USDA loans through their normal operations, but if borrowers default, the USDA guarantee covers lender losses up to the guaranteed amount, allowing lenders to extend financing they might otherwise consider too risky given the minimal borrower equity investment.

The USDA offers distinct programs serving different purposes:

USDA Guaranteed Loan Program (Section 502 Guaranteed):

USDA Direct Loan Program (Section 502 Direct):

Which USDA program should you pursue? Most homebuyers use the Guaranteed Loan Program working with approved lenders for faster processing, competitive market rates, and broader availability—Direct Loans serve very low-income applicants who may benefit from subsidized rates and payment assistance, though limited funding and longer timelines make this option less accessible for most buyers.

Several features make USDA loans attractive:

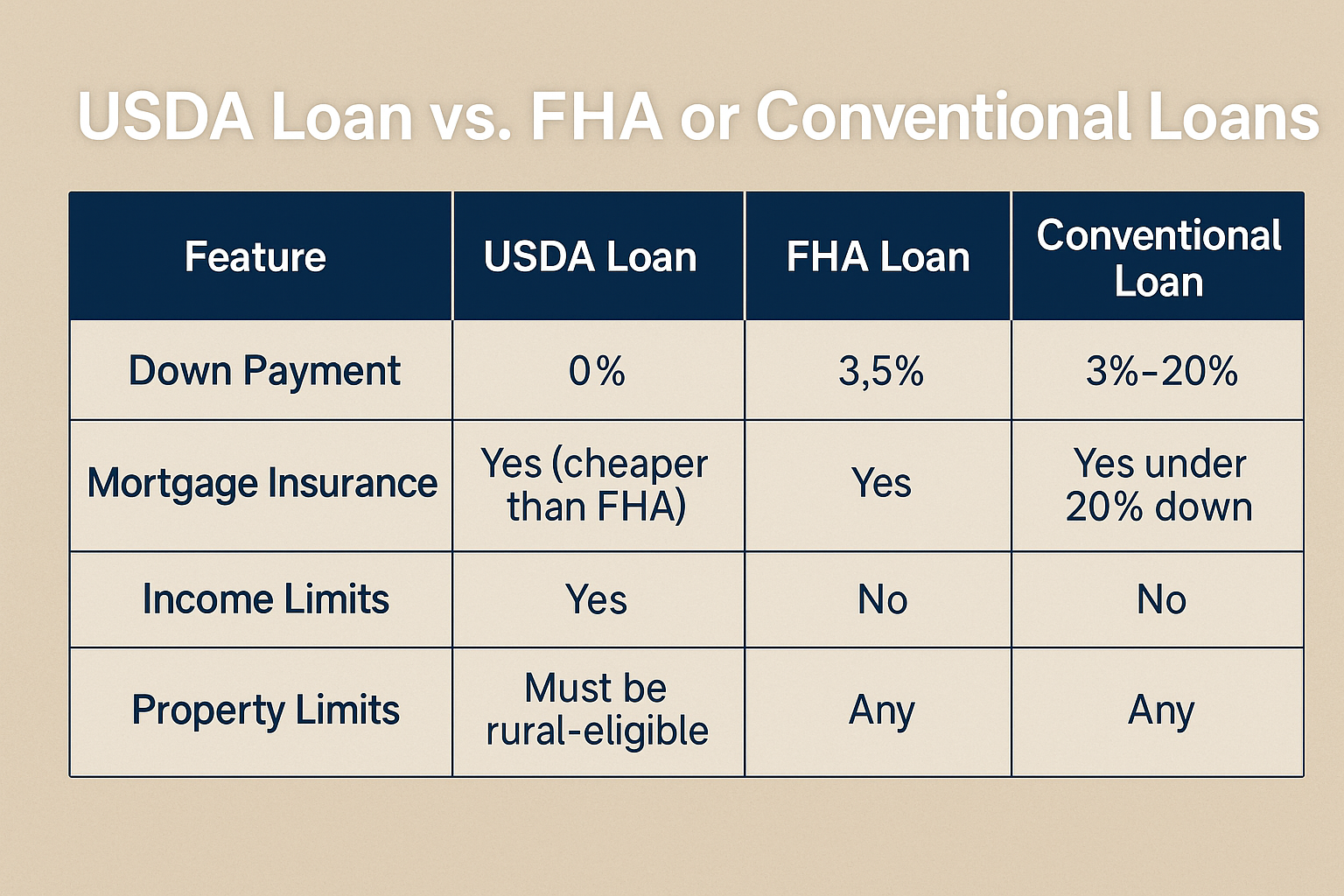

How do USDA loans compare to FHA financing? Both programs offer flexible qualification standards and serve moderate-income buyers, but USDA requires no initial equity contribution while FHA requires contributions, USDA has geographic restrictions while FHA works anywhere, USDA has income limits while FHA doesn’t, and USDA annual fees are lower than FHA mortgage insurance—choice depends on property location eligibility and income qualification.

How do you determine if a property qualifies for USDA financing? Use the USDA’s online eligibility map at eligibility.sc.egov.usda.gov where you can enter specific addresses to check property location qualification instantly—this verification should happen before making offers or even viewing homes to avoid disappointment from finding perfect properties in ineligible areas.

Understanding USDA’s definition of “rural” prevents common misconceptions about where the program works and helps you focus home searches on qualifying areas.

The term “rural” encompasses more than remote farmland:

Eligible areas include:

Ineligible areas:

What determines if an area is USDA-eligible? Population size, density, character, and proximity to urban areas all factor into designations—USDA updates eligible areas periodically based on census data, development patterns, and policy objectives, with some areas gaining or losing eligibility as communities grow or regulations change.

The online tool provides instant verification:

How accurate is the online eligibility map? The system reflects current USDA designations and updates regularly, providing reliable guidance—however, borderline properties or recent designation changes may warrant confirmation with USDA Rural Development offices or experienced USDA lenders familiar with local eligibility nuances.

Many buyers don’t realize USDA eligibility extends to suburban communities:

Examples of qualifying areas:

Why do suburban areas qualify? USDA eligibility focuses on population density and metro area boundaries rather than just distance from cities—many thriving suburban communities fall outside metropolitan statistical area boundaries or maintain population densities below USDA thresholds despite proximity to urban employment centers.

Maximize home search effectiveness:

Smart search approaches:

Areas to investigate:

Can USDA eligibility change for an area? Yes, designations update periodically based on census data and population growth—rapidly developing areas may lose eligibility as they become denser and more urban, while other areas may gain eligibility, making verification at the time of purchase critical rather than assuming past eligibility continues.

Do USDA loans have income restrictions? Yes, household income cannot exceed specific limits based on county median income and household size—limits vary by location with higher allowances in expensive areas and lower thresholds in affordable regions, designed to serve low and moderate-income households rather than high earners who can access conventional financing.

Understanding income calculation methods and limits helps you determine qualification and plan strategically if you’re near threshold boundaries.

Income assessment includes all household members:

Included income sources:

Household member inclusion:

Why does non-borrower household income matter? USDA limits address total household resources available for housing costs—including all adult household members’ income ensures the program serves truly moderate-income families rather than situations where high-earning household members could provide financial support but aren’t on the mortgage.

Limits adjust for household size and location:

Household size categories:

Geographic variations:

Example income limits (vary by location):

Where do you find your area’s income limits? Visit the USDA Rural Development website at rd.usda.gov, search for income eligibility, select your state, and find your county to see current limits—lenders can also provide county-specific limits during pre-qualification conversations.

USDA requires thorough income verification:

Standard employment documentation:

Self-employment documentation:

Other income documentation:

How does self-employment affect USDA qualification? Self-employed applicants must provide more extensive documentation with two years of tax returns showing business income—USDA calculates qualifying income similar to conventional lending, analyzing tax returns after business deductions, requiring stable income history and adequate earnings after expenses.

If you’re near income limits, consider these approaches:

Can you exclude any household member income? Only if they genuinely won’t live in the home—you cannot manipulate household composition just to qualify, as USDA requires honest reporting of all adults who will occupy the property, with fraud consequences for misrepresenting household circumstances.

What credit score do you need for USDA loans? While USDA doesn’t establish absolute minimum credit scores, most lenders require scores in the mid-600s for standard automated underwriting approval—borrowers with lower scores may still qualify through manual underwriting emphasizing payment history, though this process involves more scrutiny and documentation beyond automated approval systems.

Understanding complete financial requirements helps you prepare applications and identify areas needing attention before applying.

USDA emphasizes payment patterns over scores:

Credit score considerations:

Payment history focus:

What’s manual underwriting and when does it apply? Human underwriters review applications that don’t meet automated approval thresholds—this process examines complete financial pictures including payment histories, extenuating circumstances, compensating factors, and overall creditworthiness beyond algorithmic scoring, taking longer but enabling approvals that automated systems might decline.

Past financial difficulties require disclosure:

Bankruptcy:

Foreclosure:

Short sales or deeds-in-lieu:

Collections and judgments:

Can you qualify for USDA loans with recent credit problems? Possibly, especially with manual underwriting, if you demonstrate financial recovery, provide documentation of extenuating circumstances beyond your control, show reestablished positive credit patterns, and have strong compensating factors like stable income and employment.

USDA allows reasonable debt levels:

Standard DTI guidelines:

Debt-to-income calculations include:

Compensating factors allowing higher DTI:

What if your debt-to-income ratio is too high? Pay down revolving credit balances, pay off installment loans with low remaining balances, increase income through raises or additional employment, reduce purchase price to lower housing payment, or wait to improve financial position before applying.

Cash reserves demonstrate financial stability:

USDA reserve expectations:

Acceptable reserve assets:

How much cash should you have beyond closing? While USDA doesn’t mandate substantial reserves for most transactions, maintaining some liquid assets after closing provides cushion for unexpected expenses, demonstrates financial prudence to underwriters, and protects you from stress if emergencies arise shortly after purchase.

Ready to discuss your purchase scenario? Submit a purchase inquiry to explore your options.

Are USDA loan costs higher than conventional mortgages? USDA loans involve guarantee fees similar to FHA mortgage insurance but generally lower—upfront guarantee fee of 1% of loan amount plus annual fee of 0.35% of outstanding balance make USDA one of the most affordable government-backed programs, particularly compared to FHA’s higher mortgage insurance costs and conventional PMI for minimal equity contribution scenarios.

Understanding complete cost structure helps you budget accurately and compare USDA to alternative financing options.

USDA charges fees supporting the guarantee fund:

Upfront guarantee fee:

Annual guarantee fee:

Example total guarantee fee cost:

Can guarantee fees be avoided or eliminated? No, guarantee fees are mandatory program components enabling the federal backing that allows minimal initial investment—these fees fund the guarantee program making USDA lending viable and sustainable for taxpayers and participants.

USDA rates compete favorably with other programs:

Rate positioning:

Factors affecting your rate:

Why do USDA rates vary between lenders? Each approved lender establishes pricing within program parameters based on business model, desired profit margins, volume expectations, and risk assessments—shopping multiple USDA lenders helps identify optimal pricing rather than assuming uniform rates across all lenders.

Standard mortgage costs apply to USDA loans:

Typical closing costs:

How much should you budget for closing costs? Generally 2-5% of purchase price for total closing costs including the upfront guarantee fee—actual costs vary by property location, loan amount, title insurance rates, and lender-specific charges.

USDA allows flexibility funding closing costs:

Seller concession limits:

Closing cost financing:

Gift funds:

How can you minimize cash needed at closing? Negotiate strong seller concessions toward closing costs, ask seller to pay some prepa

id items, shop lenders for competitive fees, consider timing closing date to reduce prepaid interest, and use gift funds from family if available.

Calculate your USDA loan scenarios:

What property requirements must homes meet for USDA financing? Properties must be safe, sanitary, and structurally sound meeting HUD minimum property standards—homes need adequate heating, plumbing, and electrical systems, sound roofing and foundation, functional utilities, and safe access, ensuring borrowers purchase homes in acceptable condition rather than requiring extensive repairs immediately after purchase.

Understanding property standards prevents pursuing homes that won’t qualify and helps you evaluate whether properties need repairs before closing.

USDA adopts HUD property requirements:

Structural requirements:

Mechanical systems:

Safety and health concerns:

Property size and utilities:

What happens if a property doesn’t meet USDA standards? The appraiser identifies deficiencies in their report—sellers must address required repairs before closing, you can negotiate repair costs, or you may walk away if repairs are extensive and sellers won’t cooperate, protecting you from purchasing homes with significant issues.

Certain problems frequently arise during USDA inspections:

Issues requiring resolution:

Property types requiring extra scrutiny:

Can you purchase a fixer-upper with USDA financing? Not for homes needing extensive work—properties must be move-in ready and habitable, though minor cosmetic issues are acceptable if they don’t affect safety, sanitation, or structural integrity, distinguishing between homes needing updates versus those requiring major repairs.

Rural properties often have private systems:

Well water requirements:

Septic system requirements:

What if well or septic systems fail inspection? Sellers typically must repair or replace failed systems before closing—costs can be substantial (septic replacement often $10,000-$30,000), making pre-inspection due diligence important before making offers on properties with private systems.

USDA finances residential sites with limitations:

Acreage restrictions:

Income-producing property:

Why does USDA restrict acreage and income? The program supports residential homeownership, not agricultural operations or commercial ventures—large parcels generating farming income should use USDA Farm Service Agency programs designed for agricultural lending rather than residential housing programs.

Can you refinance a USDA loan? Yes, USDA offers streamline refinancing for existing USDA borrowers and standard refinancing when switching from other loan types to USDA—streamline refinancing provides simplified processing with reduced documentation, while regular USDA refinancing requires full underwriting but enables homeowners in eligible areas to access USDA benefits.

Understanding refinancing options helps you optimize your financing as circumstances change or rates improve.

Simplified refinancing for existing USDA borrowers:

Streamline eligibility requirements:

Streamline process simplifications:

Net tangible benefit requirement:

What are typical USDA streamline requirements? Rate reduction of at least 0.5% for loans under 24 months old, no minimum reduction for loans over 24 months as long as monthly savings occur, or ARM to fixed conversion—specific requirements vary by lender overlays beyond basic USDA rules.

Full underwriting for non-streamline situations:

Standard refinance purposes:

Standard refinance requirements:

Can you do cash-out refinancing with USDA? Limited cash-out is possible though uncommon—USDA generally discourages cash-out refinancing with restrictions on the amount you can extract, and most borrowers needing significant cash-out explore conventional or FHA options providing more flexibility for equity extraction.

USDA borrowers can refinance to different loan types:

When to consider leaving USDA:

Programs to consider:

How much equity do you need to refinance out of USDA? Conventional refinancing typically requires maintaining meaningful equity after refinancing, while FHA allows refinancing with minimal equity—evaluate whether leaving USDA’s low annual fees for conventional or FHA mortgage insurance makes financial sense based on your equity position and rates available.

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

USDA loans require properties to be move-in ready meeting minimum property standards—extensive renovations, major repairs, or homes in poor condition don’t qualify for standard USDA financing, though the USDA does offer a Section 504 loan and grant program for repairs and improvements to existing USDA-financed homes in specific situations for very low-income borrowers.

What if you want to buy a home needing repairs? Consider FHA 203(k) renovation loans allowing you to finance both purchase and repairs in one loan, conventional renovation financing if you have adequate resources, or purchasing with cash or hard money then refinancing to USDA after completing improvements if the property’s in an eligible area.

Property condition considerations:

Yes, USDA finances manufactured homes meeting specific requirements—the home must be built after June 15, 1976 to HUD manufactured home standards, permanently affixed to a foundation, titled as real property rather than personal property, and meet all standard USDA property requirements for safety and condition.

Manufactured home requirements:

What’s the difference between manufactured and mobile homes? Manufactured homes built after June 15, 1976 meet HUD Code federal construction standards and can qualify for mortgage financing including USDA, while mobile homes built before that date to lesser standards typically cannot qualify for standard mortgage programs.

Manufactured home considerations:

Yes, you can own other properties and still qualify for USDA loans—the USDA loan must be for your primary residence, but owning additional homes, investment properties, or vacation properties doesn’t automatically disqualify you, though underwriters will scrutinize whether you genuinely intend to occupy the USDA-financed home as your main residence.

Situations involving multiple properties:

What documentation proves primary residence intent? Employment location near new property, school enrollment for children, driver’s license and voter registration changes, utility transfers, and explanation letters describing relocation reasons all support genuine intent to occupy the USDA-financed home as your primary residence.

Multiple property considerations:

USDA loan timelines generally align with conventional financing for straightforward applications—most USDA loans close within standard 30-45 day periods once applications are complete, though the USDA-required appraisal and rural property characteristics may extend timelines, and lender experience with USDA processing significantly affects speed and efficiency.

Factors affecting USDA closing timeline:

How can you expedite USDA closing? Submit complete applications with all documentation upfront, respond immediately to lender requests, schedule appraisals and inspections promptly, maintain clear communication with all parties, work with experienced USDA lenders, and set realistic timeline expectations in purchase contracts.

Timeline strategies:

Yes, self-employed applicants qualify for USDA loans with appropriate documentation showing stable business income—requirements include two years of self-employment history, personal and business tax returns, year-to-date profit and loss statements, and income analysis following standard mortgage underwriting practices that calculate earnings after business expenses and deductions.

Self-employed documentation requirements:

How do lenders calculate self-employed income for USDA? Similar to conventional lending—analyzing tax returns after adding back non-cash deductions like depreciation, subtracting one-time income, averaging over two years, and ensuring stable or increasing income trends demonstrate reliable earnings supporting mortgage obligations.

Self-employment considerations:

For self-employed borrowers with complex income:

No, USDA loans don’t require perfect credit—the program emphasizes payment history over credit scores with automated underwriting typically requiring mid-600s scores while manual underwriting considers lower scores with compensating factors, recognizing that rural and moderate-income borrowers may have limited credit access or past financial challenges.

Credit considerations for USDA:

What compensating factors help with challenged credit? Strong recent payment history, stable employment over several years, low debt-to-income ratios, cash reserves beyond closing requirements, minimal housing payment increase from current costs, and overall financial responsibility demonstrated through explanations and documentation.

Credit improvement strategies:

Why does lender experience matter for USDA loans? USDA lending involves program-specific requirements, income calculations, property eligibility nuances, and appraisal standards that inexperienced lenders may handle inefficiently—working with USDA-knowledgeable lenders prevents delays, ensures accurate guidance, facilitates smoother processing, and increases approval odds through proper application structuring.

Finding and working with qualified USDA lenders helps ensure successful transactions.

Not all mortgage lenders offer USDA financing:

USDA-approved lender types:

How to find USDA lenders:

Verifying USDA lending experience:

Why avoid inexperienced USDA lenders? Learning on your transaction causes delays from misunderstanding requirements, incorrect income calculations, property eligibility mistakes, processing inefficiencies, and potential denials from improper structuring—experienced lenders navigate complexities smoothly producing better outcomes.

Evaluate lenders beyond interest rates:

Important factors:

Questions for potential USDA lenders:

Should you work with local or national lenders? Both can work well—local lenders may understand regional property markets and local USDA office nuances, while national lenders often have higher volume creating processing efficiency and competitive pricing through scale, making experience and service more important than geographic scope.

Brokers provide access to multiple USDA lenders:

Broker advantages:

Broker considerations:

When do brokers provide most value? Complex situations benefiting from multiple lender options, borderline qualifications needing lender with flexible overlays, or situations where shopping rates across institutions helps secure optimal pricing.

How can seller concessions reduce your cash needed for USDA purchases? Sellers can contribute up to 6% of the home’s purchase price toward buyer’s closing costs, significantly reducing out-of-pocket requirements—negotiating strong concessions in purchase agreements enables USDA homeownership with minimal cash investment, particularly valuable given USDA’s already flexible initial investment requirements.

Strategic negotiation maximizes USDA program benefits.

USDA permits generous seller assistance:

Concession limits:

Eligible uses for seller concessions:

What cannot be covered by seller concessions? Any required initial investment must come from buyer’s funds, gifts, or approved down payment assistance—seller concessions cannot satisfy equity contribution requirements if program requires contributions beyond financed amounts.

Strategic approaches maximize seller assistance:

Effective negotiation strategies:

Market conditions affecting negotiations:

How do you present concession requests? Include in initial purchase offer as integral part of the transaction—”Purchase price $200,000 with seller contributing $8,000 (4%) toward buyer’s closing costs”—presenting as package deal rather than separate requests increases acceptance rates.

Multiple funding sources can work together:

Possible combinations:

Down payment assistance programs:

Can you use multiple assistance sources together? Yes, as long as each source individually meets program requirements and combined assistance doesn’t exceed property value or create other issues—coordinating multiple sources requires careful documentation and lender coordination to ensure compliance.

See how other borrowers have successfully used USDA financing:

If USDA loans aren’t the right fit, consider these related options:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

USDA Rural Development Single Family Housing Programs – Official USDA resource covering guaranteed and direct loan programs, eligibility requirements, income limits, property standards, and application processes for rural homeownership.

USDA Property Eligibility Map and Address Lookup – Interactive tool allowing you to enter specific addresses to verify USDA location eligibility, search by map, and understand property qualification in real-time.

Consumer Financial Protection Bureau Mortgage Resources – Federal consumer protection agency providing educational materials on mortgages, borrower rights, shopping for loans, and understanding loan programs including government-backed options.

National Association of Realtors Rural and Resort Property Resources – Real estate professional organization offering market data, property search tools, and resources for buyers and sellers in rural markets where USDA financing is commonly used.

Mortgage Bankers Association Government Lending Resources – Trade association providing industry research, market trends, and educational materials on government-backed mortgage programs including USDA guaranteed loans.

HUD Housing Counseling Agencies – HUD-approved housing counseling agencies offering free or low-cost homebuyer education, budget counseling, and guidance on government loan programs including USDA financing options.

Federal Reserve Consumer Credit Resources – Central bank educational materials explaining mortgage markets, interest rates, loan programs, and economic factors affecting housing finance and homeownership accessibility.

USDA State Rural Development Offices – State-specific USDA Rural Development offices providing local guidance, eligible area information, approved lender lists, and direct assistance with program questions.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and contractors in your area.

Ready to get started? Apply now or schedule a call to discuss your situation.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.