Military service members, veterans, and eligible surviving spouses face unique challenges when purchasing homes or refinancing existing mortgages. Frequent relocations, deployment schedules, and varied income structures complicate traditional financing approaches. VA loans provide a specialized solution—offering competitive financing structures with flexible initial investment options, enabling qualified military families to purchase homes, refinance existing mortgages, or access home equity with terms designed specifically for those who’ve served. This comprehensive guide reveals how eligible borrowers can leverage VA loan benefits, navigate the Certificate of Eligibility process, and maximize the advantages earned through military service.

Key details you’ll discover:

Ready to explore your options? Schedule a call with a loan advisor.

A VA loan is a mortgage program guaranteed by the U.S. Department of Veterans Affairs, enabling eligible military service members, veterans, and qualifying surviving spouses to purchase homes or refinance existing mortgages with favorable terms. Unlike conventional financing that typically requires substantial initial investments, VA loans allow qualified borrowers to explore flexible funding options that minimize upfront cash requirements beyond closing costs.

The VA doesn’t lend money directly—instead, it guarantees a portion of each loan, protecting approved lenders against losses if borrowers default. This guarantee eliminates the need for private mortgage insurance, reduces lender risk, and enables more favorable terms than comparable conventional financing options.

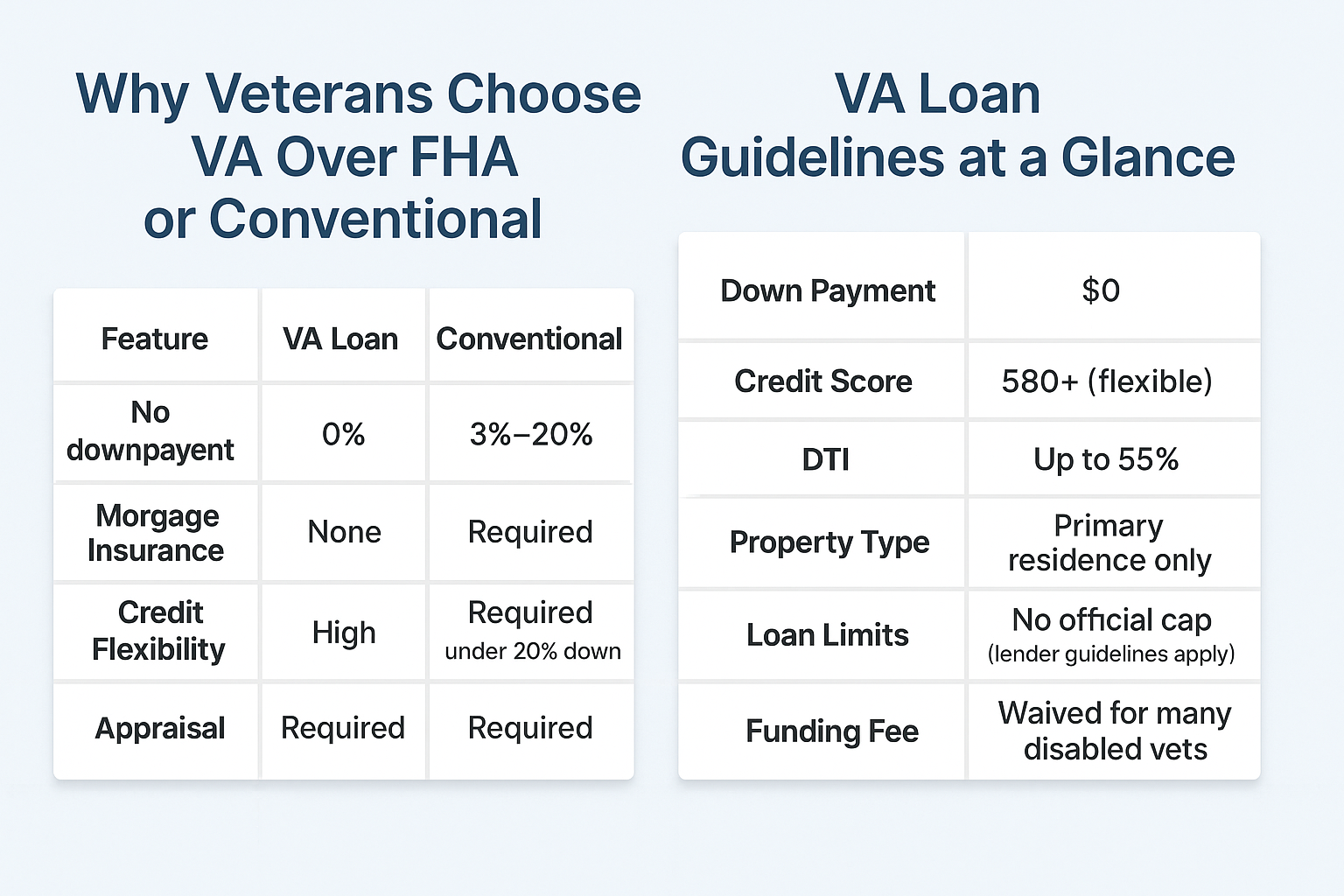

How do VA loans differ from conventional mortgage programs?

VA loans provide several distinct advantages for eligible military families:

These advantages reflect the nation’s commitment to supporting those who’ve served in uniform by making homeownership more accessible and affordable.

See how other military families have successfully used VA financing:

VA loan eligibility centers on military service requirements, creditworthiness, and income sufficiency. Understanding these requirements helps determine whether this financing option fits your circumstances.

What service qualifications make borrowers eligible for VA loans?

VA loan eligibility extends to multiple categories of current and former military personnel:

Active duty service members who have served:

Veterans who completed:

National Guard and Reserve members who have:

Surviving spouses who:

Specific service period requirements vary based on when you served. The VA eligibility requirements page provides detailed timelines for different service eras.

How do you obtain a Certificate of Eligibility for VA loans?

Before applying for VA financing, you need a Certificate of Eligibility (COE) documenting your qualification. Obtain your COE through:

Required documentation varies by service category:

Most borrowers obtain COEs within minutes through online applications or lender requests. Paper applications typically process within 5-10 business days.

What financial qualifications must VA loan applicants meet?

Beyond military eligibility, VA loans require sufficient income to support mortgage obligations and reasonable credit history:

Income sufficiency – Demonstrate stable, predictable income that comfortably covers:

Credit standards – Maintain responsible credit management including:

Residual income – Meet VA’s unique residual income requirements that calculate remaining funds after subtracting all monthly obligations. These requirements vary by:

The VA’s residual income approach provides more realistic affordability assessment than conventional debt ratios alone, recognizing that families need adequate funds for utilities, food, transportation, and emergencies beyond just paying debts.

Calculate your personalized scenarios with these tools:

What is VA loan entitlement and how does it work?

VA loan entitlement represents the amount the VA guarantees to lenders if a borrower defaults. This guarantee protects lenders and enables them to offer favorable terms without requiring private mortgage insurance or substantial initial investments.

The VA provides two layers of entitlement:

Basic entitlement – The initial guarantee amount available to all eligible veterans, which covers a portion of the loan amount

Bonus entitlement – Additional guarantee capacity that extends coverage for higher loan amounts in more expensive housing markets

Combined, these entitlement tiers enable qualified borrowers to purchase homes at various price points across different markets without initial equity contributions, provided they meet income and credit standards.

Can you use VA loan benefits more than once?

Yes. Veterans can use VA loan benefits multiple times throughout their lives. Your entitlement restores after:

Even with partial entitlement in use, many veterans retain sufficient remaining entitlement to purchase additional properties. The VA entitlement information page provides detailed guidance on calculating available entitlement and restoration processes.

Veterans with sufficient entitlement can hold multiple VA loans simultaneously. This flexibility benefits military families who:

Each property must meet VA occupancy requirements at the time of purchase, but you can convert former primary residences to rentals after establishing occupancy.

What is the VA funding fee and who pays it?

The VA funding fee helps sustain the loan program for future generations of military borrowers. This one-time charge varies based on several factors:

Service category – Regular military, Reserves, and National Guard members pay different amounts

Loan purpose – Purchase loans, refinances, and subsequent uses have varied fee structures

Initial investment amount – Larger equity contributions reduce the funding fee percentage

Disability status – Veterans receiving VA disability compensation are exempt from funding fees entirely

Most borrowers finance the funding fee into their loan amount rather than paying it at closing, spreading the cost over the life of the mortgage. Use the VA funding fee chart to determine your specific fee based on your circumstances.

Who qualifies for VA funding fee waivers?

Several categories of veterans avoid funding fees entirely:

Funding fee exemptions provide significant savings, potentially reducing overall loan costs by thousands of dollars depending on the loan amount.

The VA loan program includes several specialized options serving different borrowing needs. Understanding each type helps you select the most appropriate financing for your situation.

How do VA purchase loans work for buying homes?

VA purchase loans enable eligible military families to buy primary residences with competitive terms and flexible initial investment options. These loans work for:

VA purchase loans require properties to meet minimum property requirements ensuring homes are safe, sound, and sanitary. Properties must be move-in ready without significant repairs or safety hazards.

View VA loan purchase case studies to see how other military families have used this financing successfully.

When should you consider a standard VA refinance?

VA rate-and-term refinances allow you to replace existing mortgages with new VA loans that may offer better terms. This option works particularly well when you:

Unlike the streamlined IRRRL (discussed below), standard VA refinances require:

However, standard VA refinances offer advantages the IRRRL doesn’t provide:

View VA loan refinance case studies to explore real scenarios where this option made financial sense.

How do VA cash-out refinances provide access to home equity?

VA cash-out refinances let you tap into accumulated home equity by refinancing for more than your current mortgage balance. The difference converts to cash you can use for:

VA cash-out refinances work with any existing mortgage type—whether VA, FHA, conventional, or others. You need:

The funding fee for cash-out refinances differs from purchase loans and standard refinances, so factor this cost into your decision-making process.

View VA cash-out refinance case studies to understand when accessing equity makes strategic sense.

What makes the VA IRRRL different from standard VA refinances?

The IRRRL (Interest Rate Reduction Refinance Loan), also called the VA Streamline Refinance, provides a simplified path to refinance existing VA loans. This specialized option offers:

Streamlined processing – Minimal documentation requirements compared to standard refinances

No appraisal required – Most IRRRLs proceed without new property valuations

Reduced verification – Limited income and credit review in many circumstances

Quick closings – Faster processing timelines due to simplified requirements

Lower funding fees – Reduced fee structure compared to other VA loan types

The IRRRL serves one primary purpose: reducing your interest costs on an existing VA loan. Key restrictions include:

Use an IRRRL when you want to reduce your existing VA loan costs quickly and simply. Choose a standard VA refinance when you need more flexibility to modify loan terms, access equity, or change borrowers.

View VA IRRRL case studies to see simplified refinancing in action.

Can you use VA benefits to build a new home?

VA construction loans combine land purchase and construction financing in a single-close transaction, enabling eligible military families to build custom homes with competitive VA terms. These specialized loans cover:

VA construction loans require:

The construction-to-permanent structure provides certainty throughout the building process—you lock in your permanent financing terms before construction begins, avoiding refinancing risks after project completion.

View VA construction loan case studies to explore how military families build custom homes using VA benefits.

Ready to discuss your specific situation? Submit a purchase inquiry to explore your options.

What property standards must homes meet for VA financing?

The VA mandates minimum property requirements (MPRs) ensuring homes are safe, sound, and sanitary. These standards protect both veterans and the VA by preventing financing of properties with significant defects or safety hazards.

VA appraisers evaluate properties against specific criteria:

Structural soundness – Homes must have solid foundations, intact roofs, and stable structural systems without significant damage or deterioration

Safe electrical systems – Wiring must meet local codes without fire hazards or safety risks

Adequate heating – Properties require permanent heating systems capable of maintaining comfortable temperatures in living areas

Clean water supply – Homes need access to potable water meeting local health standards

Functional plumbing – Properties must have working plumbing systems including adequate bathroom facilities

Pest-free conditions – Homes cannot have active termite or pest infestations requiring treatment

Safe access – Properties require legal access via public roads or easements

Proper drainage – Sites must have adequate drainage preventing water accumulation or foundation damage

What property problems prevent VA loan approval?

Several conditions typically require correction before VA financing approval:

Sellers typically address these issues through repairs before closing. Alternatively, VA renovation loans can include repair costs in the financing, though this approach adds complexity to the transaction.

What types of properties qualify for VA financing?

VA loans work for several property categories:

VA loans generally don’t finance:

No. VA loans require borrowers to occupy properties as primary residences. You must move into the home within 60 days of closing and maintain it as your primary residence for at least one year, barring extraordinary circumstances like military orders.

However, you can convert former primary residences to rental properties after meeting the occupancy requirement. This flexibility helps military families who relocate frequently—you can purchase a new primary residence with a VA loan while retaining and renting your previous home.

What timeline should borrowers expect for VA loan processing?

VA loan approval timelines vary based on loan type and application complexity:

Purchase loans typically close in 30-45 days from application to closing, including:

IRRRLs often process faster, sometimes closing within 20-30 days due to streamlined documentation and limited appraisal requirements.

Cash-out refinances and standard refinances typically require 30-45 days similar to purchase loans.

Starting the process early, maintaining organized documentation, and responding promptly to lender requests accelerates timelines.

No. Unlike some government programs, VA loans don’t impose maximum income limits. Eligibility depends on military service, not income level. However, you must demonstrate sufficient income to support your mortgage obligations and maintain adequate residual income for living expenses.

Higher incomes generally strengthen applications by demonstrating strong repayment capacity, but the VA doesn’t exclude high earners from the program.

Yes. Self-employed veterans qualify for VA financing using documentation including:

Lenders analyze self-employment income carefully, often averaging earnings across multiple years to account for natural business fluctuations. Stable or increasing income trends strengthen applications, while declining patterns may require additional explanation.

For alternative self-employment financing options:

The VA doesn’t mandate specific minimum credit scores, but most lenders prefer scores above 620 for streamlined processing. Veterans with lower scores may still qualify through manual underwriting examining overall credit patterns rather than relying solely on numerical scores.

Factors that strengthen applications with lower credit scores:

Even with qualifying scores, lenders examine complete credit profiles including payment patterns, debt levels, and recent credit activity to assess overall creditworthiness.

Is it possible to hold multiple VA loans simultaneously?

Yes, provided you have sufficient remaining entitlement. Veterans with full entitlement available can typically obtain second VA loans for new primary residences. Common scenarios include:

Each property must serve as your primary residence at the time of purchase, meeting the occupancy requirement. After establishing occupancy, you can convert properties to rentals while purchasing new primary residences with additional VA loans.

Calculate your available entitlement and determine whether sufficient capacity remains for multiple properties. The VA entitlement information page provides detailed guidance on using entitlement for multiple properties.

What occupancy rules apply to VA-financed properties?

VA loans require borrowers to establish properties as primary residences within 60 days of closing. This occupancy requirement ensures VA benefits serve their intended purpose—helping military families obtain primary housing, not investment properties or vacation homes.

At closing, borrowers certify their intent to occupy properties as primary residences. This certification represents a legal commitment that the VA takes seriously. Violation of occupancy requirements can result in:

Legitimate exceptions exist for circumstances beyond borrower control, such as:

Document any circumstances preventing timely occupancy and communicate with your lender immediately to explore available options.

Can you rent out a VA-financed property after living there?

Yes. After meeting the initial occupancy requirement (typically one year), you can convert VA-financed properties to rentals. This flexibility particularly benefits military families who relocate frequently due to permanent change of station (PCS) orders.

When converting to rental use:

Many military families build substantial real estate portfolios by purchasing homes with VA loans during each relocation, then retaining and renting properties when transferring to new duty stations.

What makes VA loan assumability valuable?

VA loans include assumability features allowing qualified buyers to take over existing VA loans and their terms. This benefit can make properties more attractive to buyers, especially when current market conditions offer less favorable terms than your existing loan.

When you sell a VA-financed property, qualified buyers can assume your existing loan by:

Buyers assuming VA loans benefit from:

Does selling remove your obligation on assumed VA loans?

Not automatically. When buyers assume your VA loan, you remain liable unless you obtain formal liability release from the lender. To release liability:

If a non-veteran assumes your loan, you typically remain liable even after selling. If that buyer later defaults, the VA could pursue you for any losses. Always seek formal liability release when allowing loan assumptions.

Additionally, your VA entitlement remains tied to the assumed loan until either:

Explore all loan programs to understand your complete range of options.

Do VA loans finance properties with multiple units?

Yes. VA loans can finance properties with up to four units, provided you occupy one unit as your primary residence. This option enables veterans to:

Multi-unit properties must meet VA minimum property requirements for all units, not just your occupied space. Each unit requires:

Lenders typically use rental income from additional units when calculating qualifying income, strengthening your ability to afford larger properties. However, they usually discount expected rental income by a certain percentage to account for vacancies and expenses.

Failing to meet VA occupancy requirements represents a serious issue with potential consequences:

Immediate concerns:

If you cannot establish occupancy due to legitimate circumstances:

The VA recognizes that unexpected circumstances sometimes prevent occupancy. Early communication and honest disclosure typically lead to workable solutions, while attempting to hide occupancy violations creates far more serious problems.

What special provisions exist for Native American veterans?

The VA offers a specialized program called the Native American Direct Loan (NADL) program serving veterans who are Native American or married to Native Americans. This program enables:

The NADL program addresses unique challenges Native Americans face accessing traditional financing on trust lands where fee-simple ownership doesn’t exist. Not all tribes participate in the program—check with the VA Native American Direct Loan program for current participating tribes and availability.

How do past credit issues affect VA loan eligibility?

The VA doesn’t prohibit financing for veterans with previous bankruptcies or foreclosures, though waiting periods and seasoning requirements apply:

After Chapter 7 bankruptcy:

After Chapter 13 bankruptcy:

After foreclosure:

Lenders may impose stricter requirements beyond VA minimums. Previous VA loan foreclosures require additional considerations and potentially longer waiting periods.

What paperwork is required for VA loan applications?

Comprehensive documentation requirements include:

Military service documentation:

Income verification:

Self-employment documentation (if applicable):

Asset verification:

Credit and identity:

Organized, complete documentation accelerates processing and reduces delays from missing information or unclear circumstances.

Can family members contribute funds toward VA loan purchases?

Yes. VA loans allow gift funds from acceptable sources to cover closing costs or other transaction expenses. Acceptable gift donors include:

Gift documentation requires:

Lenders verify gift funds carefully to ensure they represent true gifts rather than disguised loans that would increase your debt obligations. Gifts must be fully transferred before closing, and you’ll need to maintain documentation proving the source.

How do VA and FHA loans differ?

Both programs serve borrowers who might struggle with conventional financing, but key differences include:

Initial investment requirements:

Mortgage insurance:

Property standards:

Eligibility:

Assumability:

VA loans typically provide better overall value for eligible military families due to the absence of mortgage insurance and competitive structures.

When should veterans choose conventional financing over VA loans?

Most eligible veterans benefit from using VA loans, but conventional financing sometimes makes sense when:

Conventional loans offer:

However, conventional loans typically require:

Calculate scenarios using both loan types to determine which approach provides better overall value for your specific situation.

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

What condominium requirements apply to VA financing?

VA loans can finance condominiums, but projects must meet VA approval standards covering:

Financial stability – The condo association must maintain adequate reserves and demonstrate sound financial management

Owner-occupancy ratios – A minimum percentage of units must be owner-occupied rather than rented

Project completion – New construction projects must reach specific completion thresholds before individual unit financing

Legal structure – Projects must have appropriate legal formation with proper documentation

Insurance coverage – Associations must carry adequate hazard and liability insurance

Check the VA condominium approval database to verify whether specific projects qualify before making purchase offers. Not all condominiums meet VA standards, so verification prevents wasted time on properties that won’t qualify.

Can you use VA benefits for manufactured housing?

Yes, but manufactured homes must meet specific requirements:

The land and manufactured home must be purchased together in a single transaction. VA loans don’t finance manufactured homes on leased land or in manufactured home communities where you don’t own the lot.

Do VA loans cap financing amounts?

For veterans with full entitlement, VA loans generally don’t impose maximum loan amounts. You can borrow whatever amount lenders approve based on your income and credit qualifications.

However, the concept of “loan limits” still matters for:

Veterans with partial entitlement – If you’ve used VA benefits previously without restoring full entitlement, limits apply based on remaining entitlement capacity

Conforming loan limits – Properties exceeding local conforming loan limits may require some initial investment to avoid second-tier liens

Lender policies – Individual lenders may impose their own maximum loan amounts based on risk management preferences

In high-cost areas, veterans can finance expensive properties without any equity contribution, provided their income supports the mortgage obligations and they have full entitlement available.

Yes. Veterans can refinance VA loans into conventional financing when this strategy makes sense. Reasons to consider this include:

However, refinancing to conventional financing usually means:

Calculate both scenarios carefully before converting VA loans to conventional financing. In most cases, VA loans provide better long-term value for eligible veterans.

What happens to VA loans during divorce proceedings?

Divorce complicates VA loan situations in several ways:

If both spouses signed the loan:

Options for resolution:

Entitlement considerations:

Consult with both your divorce attorney and mortgage professionals to understand implications and develop the best strategy for your circumstances.

What types of properties can’t use VA loans?

Several property categories don’t meet VA financing requirements:

Some property types require specialized VA loan programs—like manufactured homes needing HUD code compliance, or Native American veterans purchasing on trust lands needing the NADL program.

What steps restore VA benefits after previous use?

Restore full VA loan entitlement by:

One-time restoration without selling – Available once if you’ve repaid a previous VA loan but still own the property, allowing you to use benefits again while retaining the first home

Full restoration after selling – Automatically restores when you sell VA-financed properties and pay off the loans completely

Restoration through assumption – Regain entitlement when qualified veterans assume your existing VA loans with formal substitution of entitlement

Required documentation:

Most entitlement restorations process quickly through the VA’s electronic systems. Submit your request as soon as you’ve satisfied previous VA loans to ensure benefits are available when you need them.

What requirements apply to Guard and Reserve members?

Yes, National Guard and Reserve members qualify for VA loans after completing six years of service. Specific requirements include:

Active Reserve or Guard service including:

Alternative qualification paths:

Guard and Reserve members obtain Certificates of Eligibility the same way as regular military veterans, using DD Form 214 plus points statements showing total qualifying service time.

Ready to get started? Apply now or schedule a call to discuss your situation.

If a VA loan isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

VA Home Loans Overview and Benefits – Comprehensive Department of Veterans Affairs resource explaining loan program benefits, eligibility requirements, and application processes for all VA financing options.

VA Loan Eligibility Requirements – Official eligibility criteria detailing service requirements for active duty members, veterans, National Guard, Reserves, and surviving spouses.

VA Funding Fee Chart and Exemptions – Current funding fee schedules showing amounts based on service type, loan purpose, and initial investment levels, plus exemption criteria.

VA Certificate of Eligibility Application – Online portal for veterans to obtain Certificates of Eligibility electronically through the eBenefits system.

VA Minimum Property Requirements – Detailed standards covering property condition requirements, appraisal processes, and minimum acceptable property characteristics.

VA Condominium Approval Database – Searchable database of VA-approved condominium projects nationwide, updated regularly as projects gain or lose approval status.

Consumer Financial Protection Bureau Mortgage Guide – Federal consumer protection agency providing unbiased information about mortgage financing, closing processes, and borrower rights applicable to all loan types.

HUD Housing Counseling Services – Directory of HUD-approved housing counselors offering free or low-cost assistance with mortgage questions, financial planning, and homeownership education.

Military OneSource Financial Resources – Department of Defense program offering free financial counseling, education, and resources specifically for military families navigating home purchases and mortgages.

Defense Finance and Accounting Service – Official military pay information and resources helping service members document income for mortgage applications.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.