Purchasing luxury real estate or refinancing high-value properties requires specialized financing that exceeds standard conforming loan limits. Jumbo loans provide the purchasing power needed for premium properties, exclusive neighborhoods, and high-cost markets where property values surpass conventional lending thresholds. Understanding how jumbo financing works, what lenders evaluate, and how to position yourself for competitive terms helps you navigate the luxury real estate market with confidence and secure the capital needed for significant property investments.

Ready to explore your options? Schedule a call with a loan advisor.

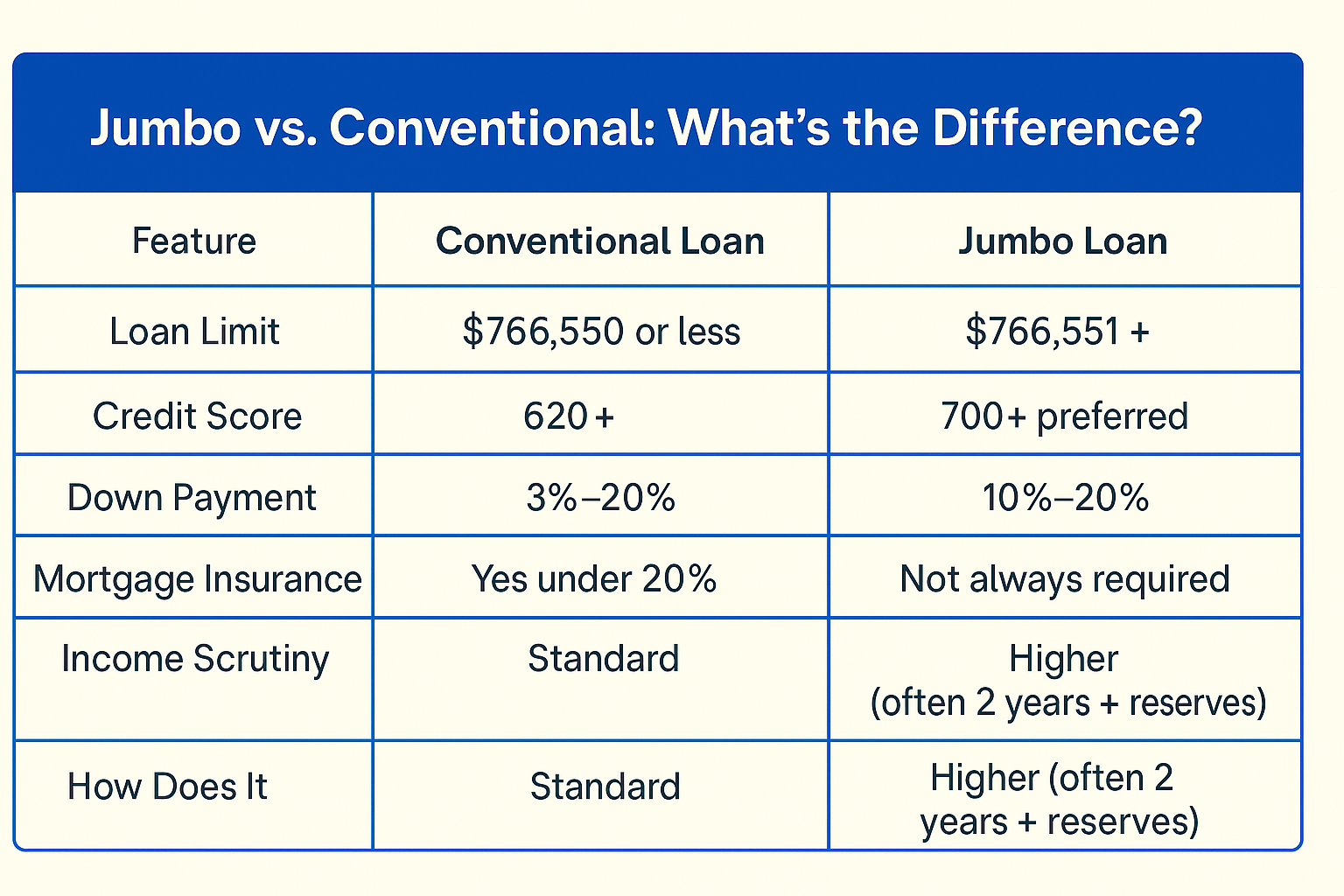

A jumbo loan is a mortgage that exceeds the conforming loan limits established annually by the Federal Housing Finance Agency (FHFA). These limits vary by county based on local housing costs, with most counties following the baseline conforming limit while high-cost areas receive higher thresholds. Any loan amount above these limits requires jumbo financing, which operates outside the government-sponsored enterprise (GSE) system of Fannie Mae and Freddie Mac.

Why do jumbo loans have stricter requirements than conforming mortgages? Because jumbo loans cannot be purchased by Fannie Mae or Freddie Mac, lenders either hold these loans in portfolio or sell them to private investors, assuming greater risk without the GSE guarantee—this increased exposure typically translates to more stringent underwriting standards and documentation requirements.

The fundamental distinction lies in risk distribution. Conforming loans benefit from standardized underwriting guidelines and GSE backing, creating liquidity and consistency across lenders. Jumbo loans lack this standardized support system, requiring lenders to independently evaluate risk and maintain higher quality standards since they can’t easily transfer risk to government-sponsored entities.

Conforming limits adjust annually based on housing market data:

Where can you find current conforming loan limits for your county? The FHFA publishes an interactive map and searchable database at their website, allowing you to enter your property location and determine whether your loan amount requires jumbo financing based on current year limits.

For example, if the baseline conforming limit is $766,550 and you’re purchasing a property for $850,000 in a standard-cost county, you need jumbo financing. However, that same loan amount might fall within conforming limits in a designated high-cost area with limits exceeding $1 million.

Jumbo loans follow two primary paths after origination:

How does the lender’s business model affect jumbo loan availability? Portfolio lenders may offer more flexible underwriting since they’re making their own lending decisions rather than conforming to investor guidelines, while lenders focused on securitization must meet investor standards that often mirror but sometimes deviate from GSE guidelines.

Understanding your lender’s approach helps explain why terms and flexibility vary significantly across jumbo loan providers.

What credit score do you need for jumbo loan approval? Most jumbo lenders establish minimum credit score thresholds significantly higher than conforming loan minimums, typically requiring scores in the excellent range to qualify for competitive terms, though specific requirements vary by lender, loan amount, and compensating factors.

Jumbo underwriting scrutinizes your entire financial picture with greater intensity than conforming loans. Lenders want certainty that borrowers with high-balance loans possess the financial sophistication, stability, and resources to manage substantial debt obligations through various economic conditions.

Strong credit positioning dramatically improves jumbo loan approval odds and pricing:

How do recent credit inquiries affect jumbo loan approval? While rate shopping for mortgages within a focused timeframe typically counts as single inquiry, numerous non-mortgage credit applications shortly before your jumbo loan application may signal financial stress or major purchases that increase your debt obligations.

Jumbo lenders typically require substantial liquid reserves beyond your initial equity contribution and closing costs:

Can you use retirement accounts for jumbo loan reserves? Many lenders accept retirement account balances toward reserve requirements, though they may apply discount factors (commonly 60-70% of value) to account for potential taxes and penalties on early withdrawal, or may require the accounts be accessible without penalty.

Jumbo lenders evaluate income with heightened scrutiny:

See how other borrowers have successfully used jumbo financing:

What documents do jumbo lenders require beyond standard mortgage applications? Jumbo underwriting typically demands more extensive documentation than conforming loans, including additional asset verification, detailed income documentation covering longer timeframes, letters explaining any unusual financial patterns, and comprehensive analysis of all debt obligations and payment histories.

The elevated documentation burden reflects lenders’ need for complete financial clarity when approving high-balance loans that carry greater absolute risk exposure despite potentially strong borrower profiles.

Employed borrowers typically provide:

Why do jumbo lenders sometimes require tax returns even for W-2 employees? Tax returns provide comprehensive income verification including side income, investment earnings, rental property cash flow, and business interests that might not appear on pay stubs but affect your overall financial picture and ability to manage jumbo loan obligations.

Business owners and self-employed borrowers face more extensive requirements:

Jumbo lenders analyze self-employment income to ensure stability and sustainability rather than one-time events or declining business performance.

Comprehensive asset documentation verifies reserves, initial equity, and overall financial strength:

How do jumbo lenders verify large deposits in bank accounts? Any significant deposits that don’t clearly correlate to documented income sources require explanation and documentation—lenders want to verify funds come from acceptable sources rather than undisclosed debt, borrowed funds, or other sources that might affect your true financial position.

Jumbo loans require thorough property documentation:

Luxury properties, unique homes, and properties with extensive land may require specialized appraisers with experience valuing high-end real estate.

What debt-to-income ratio do you need for jumbo loan approval? While conforming loans often allow debt-to-income ratios approaching 50% with strong compensating factors, jumbo lenders typically prefer more conservative ratios, though exact thresholds vary by lender, loan amount, credit profile, and reserves.

Debt-to-income (DTI) calculations measure your monthly debt obligations against gross monthly income, providing lenders insight into how comfortably you can manage additional housing debt while maintaining existing obligations.

Jumbo lenders evaluate two distinct ratio calculations:

Why do jumbo lenders care about both ratios separately? The front-end ratio isolates housing affordability regardless of other debt, while back-end ratio shows total financial obligations—borrowers might qualify on back-end ratio while exceeding front-end thresholds, signaling housing costs are disproportionate to income even if total debt remains manageable.

If your ratios exceed lender preferences, several strategies can improve your profile:

Can you exclude certain debts from jumbo loan DTI calculations? Debts being paid by others with documented payment history, loans with fewer than 10 months remaining, or obligations clearly paid from business accounts rather than personal income may receive special consideration, though policies vary by lender.

Some jumbo programs offer qualification flexibility through alternative structures:

Explore alternative qualification:

Can self-employed borrowers get jumbo loans? Yes, self-employed individuals, business owners, and entrepreneurs regularly secure jumbo financing, though they face additional documentation requirements and potential scrutiny of business stability, income consistency, and future earnings reliability that employed borrowers don’t encounter.

Traditional jumbo underwriting analyzes tax returns to determine qualifying income, which creates challenges for business owners who maximize deductions to minimize taxable income—this strategy reduces reported income that lenders use for qualification even though actual cash flow may be substantially higher.

Standard jumbo underwriting calculates self-employment income by:

Why does depreciation get added back for self-employed jumbo loan qualification? Depreciation is a non-cash deduction that reduces taxable income without affecting actual cash flow—lenders add it back because you didn’t actually spend this money, making it available for debt obligations.

This methodology works well for businesses with stable income and minimal deductions but creates qualification barriers for:

Several specialized programs accommodate self-employed jumbo borrowers:

Bank Statement Jumbo Loans – Analyze business or personal bank deposits over 12-24 months to calculate income rather than using tax returns, bypassing the deduction challenge entirely while focusing on actual cash flow.

1099 Income Loans – Verify contractor income using 1099 forms without requiring complete business tax returns, useful for independent contractors without complex business structures.

CPA Letter Programs – Some portfolio lenders accept certified accountant letters explaining income, business health, and sustainability to supplement or replace traditional tax return analysis.

Asset-Based Jumbo Loans – Eliminate income documentation entirely, instead qualifying based on substantial liquid asset holdings that demonstrate ability to manage debt obligations regardless of reported income.

How do bank statement jumbo loans calculate qualifying income? Lenders review deposit patterns in business or personal accounts, calculate average monthly deposits, and apply an expense factor (typically 25-50%) to account for business costs, resulting in qualifying income that often exceeds tax return calculations.

Real examples of self-employed jumbo loan success:

Your business structure affects jumbo loan documentation:

Can you use business income if you own less than 25% of a company? Most lenders require at least 25% ownership to use business income for qualification, as minority stakeholders lack control over distributions and business decisions affecting income continuity.

Are jumbo loan credit requirements higher than conforming mortgage standards? Yes, most jumbo lenders establish minimum credit score thresholds significantly above conforming loan minimums, reflecting the larger absolute risk exposure on high-balance loans and the lack of GSE backing that reduces lender flexibility on credit exceptions.

While conforming loans might accept credit scores in certain ranges with compensating factors, jumbo programs typically require excellent credit profiles to access competitive terms and sometimes to qualify at all.

Credit requirements vary by lender and loan structure:

How do jumbo lenders evaluate borrowers with limited credit history? Thin credit files with few accounts or short history create challenges even with perfect payment records—jumbo lenders prefer demonstrated ability to manage multiple credit types over time, making alternative credit documentation sometimes necessary.

Past credit challenges create different waiting periods depending on severity:

Can you get a jumbo loan after bankruptcy? While possible after appropriate waiting periods and credit rebuilding, post-bankruptcy jumbo qualification requires exceptional credit management following discharge, substantial reserves, strong income stability, and typically larger equity contributions than borrowers without previous credit events.

Optimize your credit profile before jumbo loan application:

What down payment do you need for jumbo loans? While specific requirements vary by lender and program, jumbo loans typically require more substantial initial equity contributions than conforming loans, with many programs establishing minimum thresholds and offering better terms with larger contributions.

Your initial equity position affects multiple underwriting factors simultaneously—the amount you invest reduces lender risk, demonstrates financial commitment, influences pricing tiers, impacts reserve requirements, and may affect whether you need mortgage insurance or face coverage limitations.

Different property uses carry distinct equity expectations:

Why do second homes and investment properties require more equity for jumbo loans? Lenders view non-primary residences as higher risk because borrowers facing financial stress will prioritize their primary residence payments over secondary properties, increasing default risk on vacation homes and rental properties.

Increasing your initial investment beyond minimums delivers multiple advantages:

Can you avoid mortgage insurance on jumbo loans? Many jumbo programs don’t require mortgage insurance at all regardless of equity contribution, though some programs do implement coverage requirements—when required, sufficient equity contributions eliminate this additional cost.

If you lack sufficient liquid savings for desired equity contribution, consider alternatives:

Are gift funds acceptable for jumbo loan down payments? Yes, most jumbo lenders accept gift funds from family members for all or part of your equity contribution, though they require gift letters stating the funds don’t need to be repaid, documentation of the donor’s ability to provide funds, and sometimes paper trail showing fund transfer.

Calculate your jumbo loan scenarios:

Are jumbo loan rates higher than conforming mortgage rates? Rate relationships between jumbo and conforming loans fluctuate based on market conditions, investor demand, portfolio lender appetite, and economic factors—sometimes jumbo rates exceed conforming rates while other periods see competitive or even lower jumbo pricing.

Understanding what drives jumbo loan pricing helps you time your borrowing and understand whether quoted terms represent competitive offers or opportunities to shop more aggressively.

Multiple variables affect the terms you’ll receive:

Why do jumbo rates sometimes beat conforming mortgage rates? When portfolio lenders have balance sheet capacity and seek quality loan assets, or when private-label securities market demand is strong, competition for jumbo borrowers with excellent profiles can drive pricing below conforming rates that carry GSE fees and standardized pricing.

Jumbo borrowers can choose between rate structures:

Fixed-rate jumbo mortgages provide payment certainty:

Adjustable-rate jumbo mortgages offer initial lower pricing:

When should you consider adjustable-rate jumbo loans? If you plan to relocate, refinance, or pay off the loan within the initial fixed period, the lower initial pricing can reduce costs compared to fixed-rate alternatives—however, you assume rate increase risk if circumstances change and you hold the loan through adjustment periods.

Strategies to secure competitive jumbo terms:

How do jumbo loan requirements differ for second homes and investment properties? Non-primary residence jumbo financing typically requires larger equity contributions, higher credit scores, lower maximum debt-to-income ratios, increased reserve requirements, and may receive different pricing compared to primary residence loans.

Lenders apply stricter standards recognizing that borrowers facing financial pressure prioritize primary residence payments, making vacation homes and rental properties more likely to default during economic stress.

Vacation properties and second homes intended for personal use face unique requirements:

Can you use rental income from your second home for jumbo loan qualification? If you plan to rent the property, it should be treated as investment property rather than second home—lenders may discover rental intent through tax returns, rental history, or property management arrangements, potentially violating occupancy certifications.

Rental properties and investment real estate require specialized consideration:

How do jumbo lenders calculate rental income for qualification? Most lenders require executed lease agreements, may discount rental income by a percentage (commonly 25%) to account for vacancies and expenses, and will verify rental income on tax returns if you’ve owned the property previously.

Debt Service Coverage Ratio loans offer alternative qualification for investment property jumbo financing:

Explore investment property options:

Ready to discuss your purchase scenario? Submit a purchase inquiry to explore your options.

Jumbo loan timelines generally align with conforming mortgages for straightforward applications, typically requiring 30-45 days from application to closing. However, complex financial situations, self-employment documentation, multiple properties, unique assets, or unusual property types may extend timelines due to additional underwriting analysis and documentation requirements.

Factors affecting jumbo loan timelines:

Expedite your jumbo loan approval by gathering documentation proactively, responding quickly to requests, selecting experienced jumbo lenders, maintaining clear communication throughout the process, and allowing realistic timelines rather than creating unnecessary pressure.

While jumbo loans typically require excellent credit profiles, borrowers with credit challenges can potentially secure financing through portfolio lenders with flexible underwriting, by providing substantial compensating factors like large equity contributions and extensive reserves, or by improving credit profiles before applying to meet traditional jumbo standards.

What compensating factors help jumbo loan approval with lower credit scores? Substantial liquid reserves far exceeding requirements, very low debt-to-income ratios, large equity contributions well beyond minimums, stable long-term employment in recession-resistant fields, strong relationship with portfolio lender, or significant assets with the institution all provide compensating strengths.

Alternative approaches for challenged credit:

While specific equity requirements vary by lender and program, many jumbo borrowers benefit from equity contributions beyond minimum thresholds to access better pricing tiers, reduce total interest costs, avoid potential mortgage insurance, strengthen their qualification profile, and provide larger equity cushions protecting against market fluctuations.

What is the optimal down payment strategy for jumbo loans? The answer depends on your alternative uses for capital—if you have high-yield investment opportunities, strong risk tolerance, or prefer maintaining liquidity for business opportunities, minimum equity contributions might make sense, while risk-averse borrowers or those without compelling alternative investments often benefit from larger equity positions.

Consider these factors when determining your equity contribution:

Jumbo condo financing faces additional scrutiny beyond single-family properties, with lenders evaluating both individual unit suitability and overall project health including financial reserves, litigation status, owner-occupancy ratios, commercial space percentages, and whether the condo association maintains adequate insurance and follows sound financial management practices.

What makes a condo project ineligible for jumbo financing? Common disqualifiers include pending or active litigation involving the homeowners association, insufficient reserve funds for common area maintenance, high percentages of investor-owned units, significant commercial space, incomplete construction or unsold developer units, unusual rental restrictions, or deferred maintenance creating potential future assessment risks.

Jumbo condo considerations:

Before making offers on luxury condos, verify the project meets jumbo lending requirements to avoid surprises during underwriting.

What advantages do portfolio lenders offer for jumbo financing? Banks and credit unions that hold jumbo loans on their balance sheets rather than selling them can offer more flexible underwriting, customized terms, relationship-based pricing, streamlined documentation for existing customers, and creative solutions for complex financial situations that don’t fit standardized investor guidelines.

Portfolio jumbo lending represents a relationship-driven approach where the lender evaluates your complete financial picture and makes individualized credit decisions rather than applying rigid investor guidelines designed for loan purchases.

These institutions can provide unique advantages:

How do you find portfolio jumbo lenders? Local and regional banks, credit unions with membership requirements, private banks serving high-net-worth individuals, and community banks focused on relationship banking most commonly hold jumbo loans in portfolio rather than selling them.

Maximize portfolio lender benefits through strategic relationship development:

Can relationship banking really affect jumbo loan terms? Yes, portfolio lenders often provide preferential pricing, reduced fees, or increased flexibility to valuable customers with substantial deposits or investment relationships, as they view you holistically rather than just as a loan applicant.

Certain scenarios particularly benefit from portfolio jumbo lending:

When should you refinance your jumbo loan? Consider refinancing when market conditions offer substantially better terms, when your credit profile has improved significantly since originating your current loan, when you need to extract equity for other purposes, or when you want to restructure debt by consolidating other obligations.

Jumbo refinancing follows similar principles to initial jumbo purchases but with additional considerations around break-even analysis, existing loan terms you’re refinancing away, and whether you’re simply improving terms or also extracting equity.

This structure simply replaces your existing mortgage with improved terms without extracting equity:

When rate-and-term refinancing makes sense:

How much must rates improve to justify jumbo refinancing? Break-even analysis compares your closing costs against monthly savings—if you’ll recoup costs within your expected occupancy period and total interest savings exceed all transaction costs, refinancing typically makes financial sense.

Calculate your refinance scenario:

Extract equity while potentially restructuring your mortgage:

Common reasons for jumbo cash-out refinancing:

How much equity can you extract through jumbo cash-out refinancing? Lenders typically limit cash-out refinancing to specific maximum loan-to-value ratios that vary by property type, with primary residences generally allowing higher ratios than second homes or investment properties, and each lender maintaining their own guidelines.

Compare scenarios:

Expect similar documentation to your original jumbo loan:

Is jumbo refinance documentation easier since you already have the loan? Sometimes, particularly with your existing lender who already knows your file, but market conditions and your financial situation may have changed significantly requiring full underwriting analysis—don’t assume documentation will be dramatically simplified.

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

What mistakes do borrowers make when applying for jumbo loans? Common errors include making major financial changes during the application process, failing to compare multiple lenders, neglecting to optimize their credit profile before applying, choosing inappropriate loan structures for their situation, underestimating reserve requirements, and not thoroughly documenting complex income sources.

Avoiding these pitfalls helps ensure smooth jumbo loan approval and positions you for the most competitive terms available given your financial profile.

Lenders verify your financial situation immediately before closing, and significant changes can derail approved loans:

Actions that jeopardize jumbo loan approval:

Why do lenders re-verify everything before closing jumbo loans? The increased absolute risk on high-balance loans makes lenders particularly sensitive to last-minute changes that might affect your ability to manage the substantial debt obligation—what might be minor on conforming loans becomes significant on jumbo mortgages.

Jumbo loan markets are less standardized than conforming mortgages, creating significant pricing variations:

Compare at minimum:

How much can jumbo loan pricing vary between lenders? Differences of significant percentages in pricing or thousands of dollars in fees occur regularly in jumbo markets due to varying business models, portfolio appetite, and underwriting flexibility—comprehensive shopping often identifies materially better opportunities.

Minor credit management improvements can shift you into better pricing tiers or strengthen borderline applications:

Strategic credit optimization for jumbo loans:

Plan credit optimization at least 3-6 months before your anticipated jumbo loan application for maximum impact.

Many borrowers underestimate liquid assets needed after closing:

Reserve calculation mistakes:

Before applying, verify you’ll meet reserve requirements comfortable margin after your initial equity contribution and closing costs.

Self-employed borrowers and those with diverse income often sabotage their applications through inadequate documentation:

Self-employment documentation errors:

Work with experienced jumbo loan officers who can guide self-employed borrowers through documentation requirements before submission.

What specialized jumbo loan programs exist for wealthy individuals? Private banks, wealth management divisions, and specialized lenders offer ultra-high-net-worth jumbo programs featuring very high loan limits, asset-based qualification without income documentation, relationship pricing based on total assets, and concierge service including dedicated lending teams.

These programs cater to borrowers with substantial wealth who may have complex income structures, desire privacy, value relationship banking, or don’t fit traditional underwriting despite obvious financial capacity.

Qualify based on liquid asset holdings rather than income:

How asset-based jumbo qualification works:

What assets count toward asset-based jumbo loan qualification? Most programs accept checking, savings, money market accounts, stocks, bonds, mutual funds, and sometimes retirement accounts (possibly with discounts), while excluding illiquid assets like real estate, business interests, collectibles, or assets with restricted access.

Real examples:

High-net-worth individuals with substantial banking relationships access premium jumbo services:

Private banking jumbo advantages:

How do pledged asset lines work for jumbo properties? Rather than selling investments for your equity contribution or taking traditional loans, you pledge investment portfolio as collateral, maintaining investment upside potential while accessing liquidity for real estate purchases.

Non-U.S. citizens purchasing U.S. real estate access specialized programs:

Foreign national considerations:

Can foreign nationals get jumbo loans without U.S. credit history? Yes, specialized programs evaluate foreign credit reports, bank statements, asset documentation, and income verification from home countries, using property equity position as primary underwriting focus rather than U.S. credit systems.

Yes, jumbo construction-to-permanent loans finance building custom homes by providing construction financing that converts to permanent mortgage upon completion, though these programs require detailed architectural plans, licensed builder contracts, property appraisals based on completed plans, and typically larger equity contributions due to construction risk.

How do jumbo construction loans disburse funds? Rather than lump sum distribution, construction loans release funds in draws as building milestones complete and pass inspection—this protects both borrower and lender from contractor performance issues while ensuring quality construction matching approved plans.

Construction loan considerations:

Property division during divorce affects jumbo loans significantly—one spouse retaining the property must typically refinance to remove the other from loan obligations, or if selling, jumbo loan payoff comes from proceeds before equity division, with timing considerations around market conditions and refinancing qualification.

Can you remove a spouse from a jumbo loan without refinancing? Most lenders won’t release co-borrowers from loan obligations without full payoff or refinancing since original underwriting included both borrowers’ income and credit—removal changes the risk profile substantially and violates the original lending agreement.

Divorce strategies for jumbo properties:

Divorcing parties should work with attorneys understanding real estate implications, engage mortgage professionals early about refinancing feasibility, obtain property valuations and loan payoff quotes, and understand tax implications of various division scenarios.

Conforming loan limits determining jumbo thresholds vary significantly by county based on local median home values, with high-cost areas including much of California, metro New York, Washington D.C., Hawaii, and other expensive markets receiving substantially higher conforming limits than baseline levels.

Where can you find conforming loan limits for your specific county? The Federal Housing Finance Agency maintains an interactive map and searchable database at FHFA.gov allowing you to enter your property address or county and determine current year conforming loan limits, which change annually based on housing market data.

Location considerations:

Understanding your local limit determines whether you need jumbo financing or can potentially use conforming loan programs.

Yes, borrowers can carry multiple jumbo mortgages on different properties simultaneously, though qualification becomes progressively complex as lenders must evaluate combined debt obligations, reserves covering all properties, management of multiple high-balance loans, income supporting total debt, and overall financial capacity to handle substantial aggregate leverage.

How do multiple jumbo loans affect qualification for additional financing? Each existing jumbo loan’s payment appears in debt-to-income calculations, reserve requirements multiply to cover all properties, lenders scrutinize income stability more closely, credit profile must demonstrate consistent payment management, and equity in multiple properties affects overall risk assessment.

Multiple jumbo loan strategies:

Interest-only jumbo structures allow you to pay only interest during an initial period (commonly 5-10 years) before beginning principal amortization, reducing initial payment obligations while maintaining ultimate repayment, though you don’t build equity during interest-only period and face payment increases when amortization begins.

When do interest-only jumbo loans make sense? Borrowers expecting significant future income increases, those planning to sell before amortization begins, investors focusing cash flow on other opportunities, ultra-wealthy individuals who prefer liquidity over equity building, or those with irregular income patterns matching interest-only flexibility.

Interest-only considerations:

What happens when the interest-only period ends? Payments increase significantly as principal amortization begins, calculated to fully repay the loan over remaining term—borrowers must plan for this payment adjustment through income growth, refinancing, property sale, or asset liquidation.

Both fixed and adjustable-rate structures exist for jumbo loans, with fixed-rate mortgages providing payment certainty throughout the loan term while adjustable-rate mortgages offer lower initial pricing during fixed periods before periodic adjustments begin, and the optimal choice depends on your occupancy plans, risk tolerance, and rate outlook.

How do jumbo ARM adjustment periods work? After an initial fixed period (typically 5, 7, or 10 years), rates adjust periodically (commonly annually) based on an index plus margin, with adjustment caps limiting how much rates can change per adjustment and over the loan life, providing some protection against dramatic payment increases.

ARM considerations:

Fixed-rate advantages:

If a jumbo loan isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

Federal Housing Finance Agency Conforming Loan Limits – Official FHFA interactive map and searchable database showing current year conforming loan limits by county, helping determine whether your financing needs require jumbo loan products.

Consumer Financial Protection Bureau Jumbo Mortgage Information – Federal consumer protection agency resource explaining jumbo loan basics, differences from conforming mortgages, and consumer rights throughout the lending process.

IRS Publication 936: Home Mortgage Interest Deduction – Official IRS guidance on mortgage interest deductibility including limitations on deduction amounts, qualified residence rules, and reporting requirements for itemized deductions.

Mortgage Bankers Association Research on Jumbo Lending – National trade association providing market research, industry trends, and analysis of jumbo mortgage markets including origination volumes, pricing trends, and market conditions.

Urban Institute Housing Finance Policy Center – Research organization analyzing housing finance markets including jumbo lending trends, policy implications, and market dynamics affecting high-balance mortgage availability.

Freddie Mac Understanding Mortgage Rates and Limits – Weekly mortgage market survey tracking rate trends including jumbo versus conforming rate relationships and historical data for market analysis.

Federal Reserve Consumer Resources on Mortgages – Central bank educational resources explaining how monetary policy affects mortgage markets, interest rate factors, and economic conditions influencing lending.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and contractors in your area.

Ready to get started? Apply now or schedule a call to discuss your situation.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.