Self-employed borrowers often find their tax returns don’t reflect their true earning capacity due to legitimate business deductions. Bank statement loans bypass traditional income documentation by analyzing your actual cash flow through business or personal bank deposits. Whether you’re a business owner, freelancer, or independent contractor, this qualification method recognizes the income that flows through your accounts rather than what appears on your tax returns.

Ready to explore your options? Schedule a call with a loan advisor.

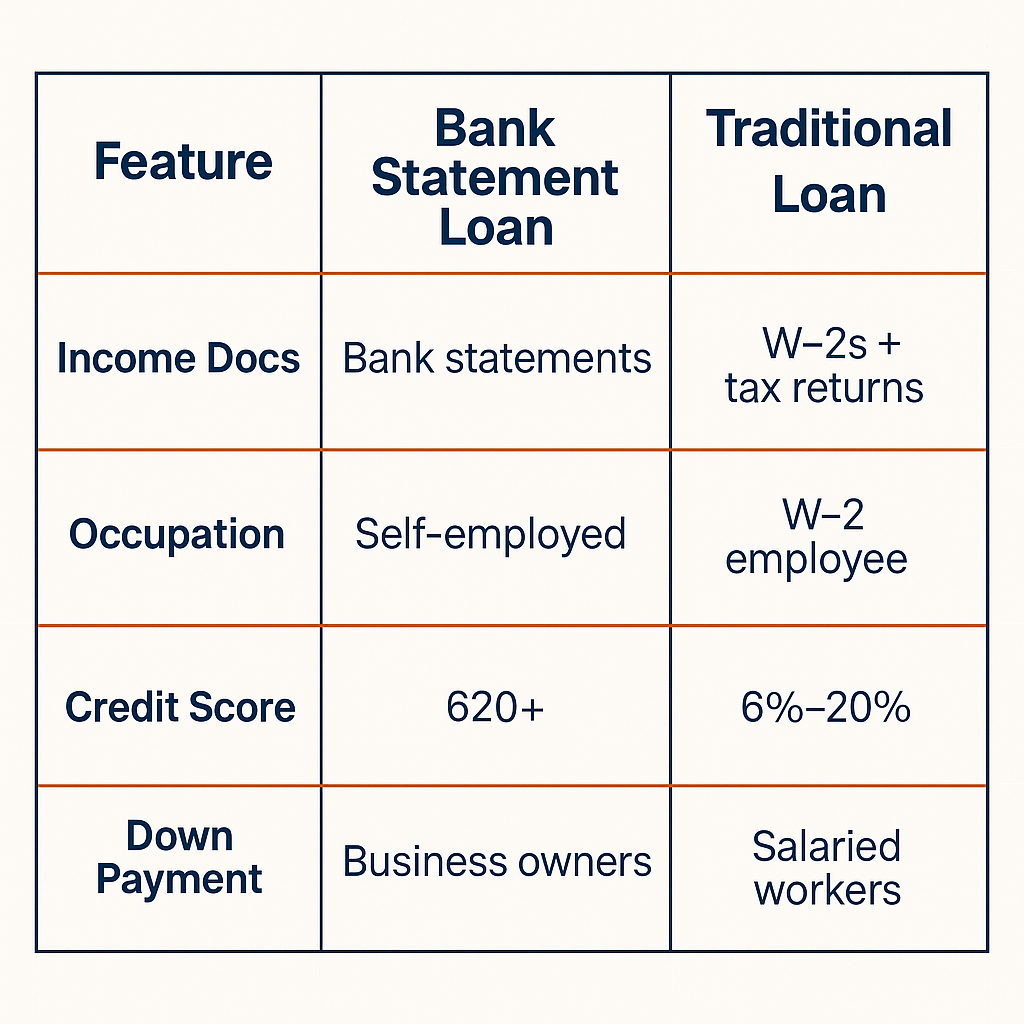

A bank statement loan represents a mortgage qualification approach designed specifically for self-employed borrowers whose tax returns don’t reflect their true earning capacity. Instead of analyzing tax returns with complex Schedule C deductions, depreciation, and business expenses, lenders verify your income by reviewing deposits in your personal or business bank accounts.

How does bank statement income verification work? Lenders collect 12-24 months of bank statements and analyze deposits to calculate your average monthly income. Rather than using the net income shown on tax returns—which often appears artificially low due to legitimate business deductions—a bank statement loan recognizes the actual cash flowing through your accounts.

The methodology acknowledges a fundamental truth about self-employment: smart business owners minimize taxable income through strategic deductions including vehicle expenses, home office costs, equipment purchases, meals, travel, and depreciation. While these strategies reduce tax liability, they also reduce the income shown on tax returns that conventional lenders use for qualification. A bank statement loan solves this disconnect.

Several borrower profiles find exceptional value in a bank statement loan structure. These programs serve business owners and self-employed professionals whose financial strategies prioritize tax efficiency over reported income.

Business owners with significant write-offs represent ideal candidates for a bank statement loan. If your accountant helps you legally minimize taxes through aggressive but legitimate business deductions, your tax returns likely show minimal net income despite strong cash flow. A bank statement loan evaluates your actual deposits rather than taxable income.

Independent contractors and freelancers who operate as sole proprietors often write off substantial business expenses. While these deductions save thousands in taxes annually, they devastate mortgage qualification under traditional programs. A bank statement loan recognizes your gross revenue rather than penalizing your tax planning.

Real estate investors and agents frequently show minimal taxable income due to depreciation, vehicle expenses, marketing costs, and other business deductions. A bank statement loan accommodates real estate professionals building their own property portfolios alongside their businesses.

Restaurant owners, contractors, and cash-intensive businesses may have income flowing through accounts that doesn’t perfectly align with complex business tax returns. A bank statement loan focuses on demonstrated deposits rather than intricate tax documentation.

Recently self-employed professionals who transitioned from W-2 employment may lack two years of business tax returns required by conventional programs. Some bank statement loan structures accommodate borrowers with shorter self-employment history when strong bank deposits demonstrate earning capacity.

Explore all loan programs to understand your full range of options.

Understanding the specific documentation requirements helps you prepare for a smooth application process. A bank statement loan simplifies qualification compared to traditional self-employment verification but requires thorough bank account documentation.

Required documentation typically includes:

Do you need personal or business bank statements? The answer depends on your business structure and where your income deposits. Sole proprietors typically use personal bank statements showing all business deposits. LLC owners, S-corporation shareholders, or partnership members might use business bank statements. Some borrowers provide both personal and business statements for comprehensive income documentation.

How many months of bank statements do lenders require? Most bank statement loan programs require 12 or 24 months of consecutive bank statements. The 12-month option typically applies to borrowers with very strong credit, substantial reserves, and stable deposit patterns. The 24-month requirement provides more comprehensive income analysis and accommodates borrowers with seasonal businesses or variable income.

What if you have multiple bank accounts? Many self-employed borrowers maintain separate checking accounts for different business lines, personal expenses, or savings strategies. Lenders can typically aggregate deposits across multiple accounts to calculate your total qualifying income, though you’ll need to provide complete statement sets for each account used in the calculation.

Do you still need tax returns? While the bank statement loan doesn’t use tax returns for income calculation, most lenders still request your most recent year or two of personal tax returns. These documents verify you’re filing taxes, confirm self-employment status, and provide additional financial context—but the actual income shown doesn’t determine your qualification.

Understanding the income calculation methodology helps you estimate your potential qualification before applying. A bank statement loan uses a more intuitive approach than traditional tax return analysis, but specific formulas vary by lender.

What’s the basic calculation method? Lenders review all deposits in your bank statements and add them up to determine gross monthly income. They then apply an expense factor—typically 25-50%—to account for business costs that don’t appear as separate expenses in your statements. The remaining amount becomes your qualifying income.

Why do lenders deduct an expense percentage? Even though your bank deposits represent actual cash received, lenders recognize you incur business costs. The expense factor accounts for typical business obligations without requiring detailed expense documentation. A 50% expense factor means lenders assume half your deposits represent business costs, leaving the other half as net qualifying income.

Can you get a lower expense factor? Some programs offer expense factors as low as 25% or even 0% for specific industries or borrower profiles. Lower expense factors result in higher qualifying income, enabling larger loan amounts. Factors affecting your expense percentage include:

How do lenders handle non-income deposits? Bank statements often show deposits beyond business income including transfers between accounts, loan proceeds, reimbursements, or returns. Experienced underwriters distinguish between income-generating deposits and non-income transfers when calculating your qualifying capacity.

What about seasonal businesses? Many self-employed borrowers experience seasonal income fluctuations—landscapers busy in summer, tax preparers swamped in spring, or retailers peaking during holidays. Lenders typically average deposits over the full 12-24 month period to smooth seasonal variations and establish consistent monthly qualifying income.

Calculate your bank statement loan scenarios:

The fundamental distinction lies in how lenders evaluate your income and which documentation determines your qualifying capacity. Traditional mortgages require extensive tax return analysis while a bank statement loan focuses on actual deposits.

Traditional mortgage qualification for self-employed borrowers:

Bank statement loan qualification approach:

Why do business deductions hurt conventional qualification so much? Every legitimate business expense you claim—vehicle costs, home office deductions, equipment purchases, business meals, professional development, insurance, supplies—reduces your net income on Schedule C. While these deductions save you thousands in taxes, they devastate mortgage qualification by lowering the income number lenders use for approval.

A bank statement loan recognizes this disconnect. Your actual earning capacity appears in your bank deposits, not in your strategically minimized taxable income.

Ready to discuss your purchase scenario? Submit a purchase inquiry to explore your options.

A bank statement loan program accommodates diverse property categories, providing flexibility for various real estate goals. Understanding which property types qualify helps you plan your home purchase or investment strategy.

Eligible property categories:

Can you purchase investment properties with a bank statement loan? Yes, many bank statement loan programs accommodate investment property purchases. Self-employed borrowers building real estate portfolios can leverage their business bank deposits to qualify for rental acquisitions without analyzing rental income projections through traditional underwriting.

Are there property value limits? Bank statement loan programs typically extend beyond conventional conforming limits, accommodating luxury properties and high-value acquisitions. Many programs approve properties well into the multi-million dollar range, making them particularly valuable for successful business owners purchasing upscale homes.

What about property condition requirements? Most bank statement loan programs require properties in good condition suitable for immediate occupancy. Properties needing extensive repairs, significant safety issues, or major system replacements may require renovation financing or alternative program structures.

See how other self-employed borrowers have successfully used bank statement financing:

Credit profile evaluation remains important for a bank statement loan qualification, though specific requirements vary by lender and program. Understanding the credit standards helps you assess your readiness to apply.

Minimum credit score expectations – Most bank statement loan programs establish baseline credit score requirements ranging from 600 to 700 depending on the specific program structure, equity contribution, and compensating factors. Higher credit scores typically provide access to more competitive pricing and lower expense factors in income calculation.

How does credit history impact approval? Lenders evaluate your credit report for payment patterns, credit utilization, derogatory marks, and overall credit management. Consistent on-time payments on credit cards, business debts, auto loans, and previous housing obligations demonstrate financial responsibility even when your tax returns show minimal income.

Can you qualify with past credit challenges? Many bank statement loan programs accommodate borrowers with previous credit issues including collections, charge-offs, late payments, or even past foreclosures when sufficient seasoning has occurred. The focus shifts to demonstrating credit recovery and current responsible financial management alongside your documented bank deposits.

Does bankruptcy disqualify you from a bank statement loan? Previous bankruptcy—whether Chapter 7 or Chapter 13—doesn’t automatically disqualify you. Most programs require waiting periods ranging from 2-4 years after discharge or dismissal, depending on the bankruptcy type and the presence of extenuating circumstances.

Yes, many borrowers benefit from combining personal and business bank statement analysis to maximize qualifying income. If you operate as a sole proprietor with business deposits flowing into personal accounts while also maintaining a business checking account, lenders can typically aggregate deposits across both account types.

This approach requires providing complete statement sets for all accounts used in the income calculation and ensuring no double-counting of transfers between accounts. Experienced underwriters track fund flows to identify true income deposits versus internal transfers.

Self-employed borrowers often receive large irregular deposits including annual bonuses, project completions, real estate commissions, or seasonal income. Lenders accommodate irregular deposit patterns by averaging income over the full 12-24 month statement period rather than requiring consistent monthly amounts.

How lenders handle irregular deposits:

This averaging approach naturally smooths income fluctuations common in self-employment, making qualification accessible even when month-to-month deposits vary significantly.

Unlike the extensive deposit sourcing required for down payment verification in conventional mortgages, bank statement loan income analysis focuses on patterns rather than individual deposit explanations. Lenders understand self-employment income arrives in diverse forms from multiple sources.

However, you may need to explain unusually large deposits, transfers between accounts, loan proceeds, or non-income items that could artificially inflate your deposit totals. Clear business operations with straightforward income patterns require minimal explanation.

Most bank statement loan programs require demonstrating 12-24 months of consistent bank deposits, effectively requiring at least one year of self-employment history. However, specific programs accommodate borrowers with shorter self-employment periods when:

The shorter your self-employment history, the more important compensating factors become in securing approval.

Competitive program structures reflect the specialized underwriting approach for self-employed borrowers. While specific pricing varies based on individual scenarios, understanding the general pricing framework helps you evaluate whether a bank statement loan fits your financial strategy.

What factors influence pricing on a bank statement loan? Several elements affect your specific rate structure:

Are rates higher than conventional mortgages? A bank statement loan typically carries slightly higher pricing compared to traditional W-2 employment mortgages due to the alternative documentation approach. However, the pricing differential often proves minimal compared to the qualification advantages—many self-employed borrowers cannot qualify conventionally at any rate due to tax return income limitations.

Can you improve your rate with stronger qualification factors? Demonstrating multiple years of increasing deposits, maintaining excellent credit, providing 24 months of statements instead of 12, offering larger equity contributions, or showing substantial cash reserves often provides access to more competitive pricing tiers within bank statement loan programs.

The total value evaluation should consider both pricing and qualification accessibility. For self-employed borrowers who would qualify for significantly lower loan amounts using tax returns—or who cannot qualify conventionally at all—a bank statement loan often represents the optimal financing solution despite potentially higher costs.

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

Understanding the specific benefits helps you evaluate whether this program aligns with your financial situation as a business owner. A bank statement loan offers distinct advantages for self-employed professionals whose tax strategies create qualification challenges.

Key advantages include:

Significantly higher qualifying income – By focusing on gross deposits rather than net taxable income, most self-employed borrowers qualify for substantially larger loan amounts. Business owners with $200,000 in gross revenue but $50,000 in net income after deductions might qualify based on $150,000+ using bank statement analysis versus $50,000 using tax returns.

Rewards tax-efficient business strategies – Instead of penalizing smart tax planning, a bank statement loan recognizes that business deductions reduce tax liability without proportionally reducing your ability to afford housing obligations. Your accountant’s tax-saving strategies no longer sabotage your mortgage qualification.

Simpler documentation requirements – Skip the complex tax return analysis including Schedule C reconstruction, depreciation add-backs, and intricate business financial statements. Bank statements provide straightforward income verification without extensive supplementary documentation.

Faster approval process – Without extensive business tax return analysis and complicated income calculations, underwriting proceeds more efficiently. Many business owners experience compressed timelines from application to approval compared to traditional self-employment mortgages.

Accommodates various business structures – Whether you operate as a sole proprietor, LLC, S-corporation, or partnership, a bank statement loan can accommodate your structure by analyzing the appropriate bank accounts where your income flows.

Works with shorter self-employment history – Some programs accommodate borrowers with 12 months of consistent deposits rather than requiring 2 years of business tax returns, providing earlier homeownership access for new business owners.

If a bank statement loan isn’t the right fit, consider these alternatives for self-employed financing:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to uncover your goals.

Business bank accounts showing payroll expenses, contractor payments, or other business disbursements require careful analysis. Lenders distinguish between gross revenue deposits and operational expenses flowing through the account to isolate your actual qualifying income.

If your business bank statements show $500,000 in annual deposits but $300,000 flows immediately to employee payroll and vendor payments, lenders focus on the net amount available to you. This scenario might benefit from providing both business accounts (showing gross revenue) and personal accounts (showing your actual compensation) for clearer income documentation.

Transitioning from traditional employment to business ownership creates unique qualification scenarios. If you have extensive W-2 history in the same industry followed by 12 months of strong self-employment bank deposits, some programs accommodate this transition by considering both your employment history and current business income.

Transition qualification strategies:

Bank statement loan programs focus on checking account deposits representing business revenue or self-employment income. Savings account interest, investment dividends, or capital gains shown in brokerage statements typically don’t qualify as business income for bank statement analysis.

However, some hybrid programs consider various income sources by combining bank statement analysis for business income with traditional documentation for investment income, creating comprehensive qualification for borrowers with diversified income streams.

Modern self-employed professionals often receive income through digital platforms including PayPal, Venmo, Cash App, cryptocurrency exchanges, or payment processors. These deposits appear in bank statements when transferred to traditional accounts, making them accessible for bank statement loan qualification.

Digital income considerations:

Many self-employed borrowers operate under DBAs (Doing Business As), trade names, or business entities with names different from their personal names. When deposits show business names or client names that don’t match your personal name, you’ll need documentation connecting you to the business.

Documentation for business name verification:

Sole proprietors frequently commingle business and personal expenses in a single checking account. While not ideal accounting practice, this reality doesn’t disqualify you from a bank statement loan. Lenders analyze total deposits to determine income, and the expense factor applied accounts for both business and personal obligations.

However, cleaner separation between business and personal finances may result in more favorable underwriting review and potentially lower expense factors, leading to higher qualifying income.

Even if your tax returns show business losses for previous years, a bank statement loan focuses on current deposits rather than historical tax return income. If your business experienced difficulties in prior years but recent bank statements demonstrate recovery with strong consistent deposits, you can qualify based on current performance.

This approach particularly benefits business owners who weathered economic challenges, business transitions, or startup losses but now show sustainable revenue in their bank accounts.

Lenders typically verify that income patterns remain consistent from initial application through closing. If your business deposits drop significantly during the approval process—perhaps due to seasonal slowdowns, client losses, or business changes—this may trigger additional review or require updated documentation.

Maintaining qualification consistency:

Foreign national borrowers operating businesses in the United States and maintaining U.S. bank accounts may qualify for specialized bank statement loan programs depending on visa status, business documentation, and lender guidelines. The combination of non-citizen status and self-employment income requires careful program selection.

Foreign national bank statement qualification typically requires:

Many entrepreneurs operate several businesses simultaneously or maintain multiple income streams through various ventures. A bank statement loan can accommodate multiple income sources by analyzing all business bank accounts where these income streams deposit.

Multiple business considerations:

Ready to get started? Apply now or schedule a call to discuss your situation.

Official Government Guidance:

CFPB Alternative Income Verification Mortgage Information – Consumer Financial Protection Bureau resource explaining alternative documentation mortgages, qualified mortgage standards, and income verification methods for self-employed borrowers beyond traditional tax return analysis.

IRS Self-Employment Tax Guidelines – Internal Revenue Service comprehensive resource on self-employment tax calculations, quarterly payment requirements, and business income reporting that affects mortgage qualification for business owners.

IRS Schedule C Business Expense Information – Internal Revenue Service official guidance on Schedule C profit or loss from business, explaining business expense deductions that reduce taxable income but may not reflect actual cash flow for mortgage qualification.

Industry Organizations:

Fannie Mae Self-Employed Income Documentation Guidelines – Official Fannie Mae underwriting standards for self-employed borrowers explaining traditional income calculation methods and documentation requirements that bank statement loans provide alternatives to.

National Association of Self-Employed Resources – Industry organization providing education, advocacy, and resources for self-employed professionals including guidance on financial management, business banking, and recordkeeping practices that support mortgage qualification.

Educational Resources:

SBA Small Business Financial Management – Small Business Administration guidance on business financial management, cash flow analysis, and accounting practices that support strong bank statement documentation for mortgage applications.

IRS Business Banking Account Information – Internal Revenue Service resource on business banking accounts, recordkeeping requirements, and financial documentation best practices for self-employed professionals and business owners.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and financial advisors in your area.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.