Renovating your home shouldn’t mean depleting your savings or settling for high-interest credit cards. Home improvement loans offer a strategic path to fund upgrades that enhance your living space while potentially increasing your property’s market value. Whether you’re updating a kitchen, adding square footage, or making essential repairs, understanding your financing options helps you make informed decisions that align with your financial goals and renovation timeline.

Ready to explore your options? Schedule a call with a loan advisor.

A home improvement loan is financing specifically designed to fund renovations, repairs, or upgrades to your residential property. Unlike personal loans used for any purpose, these loans are structured around your renovation project’s scope, with lenders often requiring project documentation, contractor estimates, and in some cases, inspection milestones before releasing funds.

How does a home improvement loan differ from a home equity loan? While both can fund renovations, home improvement loans represent a broader category that includes multiple financing structures, from unsecured personal loans to government-backed programs like FHA 203(k) loans that combine purchase or refinance with renovation costs in a single mortgage.

The fundamental advantage lies in accessing capital without liquidating investments or disrupting your emergency fund. You maintain liquidity while spreading renovation costs over time, potentially benefiting from tax deductions if the improvements qualify under IRS guidelines for capital improvements versus repairs.

Different renovation scenarios call for different financing approaches:

Each structure carries distinct advantages depending on your equity position, credit profile, project timeline, and whether you’re simultaneously purchasing or refinancing.

Can you borrow more than your current home value for renovations? Yes, with certain renovation loan programs that evaluate your property’s after-repair value (ARV) rather than current market value, significantly expanding your borrowing capacity for transformative projects.

Traditional lending focuses on current value as collateral. If your home is worth $400,000 and you owe $300,000, conventional approaches limit borrowing to the $100,000 equity difference minus any equity requirements. This constraint prevents many homeowners from funding substantial improvements that would dramatically increase property value.

ARV-based lending changes this dynamic. If your $400,000 home will appraise at $550,000 after renovations, lenders may structure financing around the higher future value. This approach particularly benefits:

The lender typically orders two appraisals: current “as-is” value and projected “as-completed” value based on your renovation plans and contractor estimates. Your borrowing capacity derives from the higher projected value, though lenders maintain risk management through renovation escrow accounts that release funds at completion milestones.

Securing ARV-based financing requires thorough project documentation:

Lenders review this documentation to validate the projected value increase is realistic and achievable within the proposed timeline and budget.

Should you refinance and take cash out for renovations simultaneously? When market conditions favor refinancing your existing mortgage, combining this with cash-out for renovations can optimize your overall debt structure while funding improvements in a single transaction.

Consider a scenario where you currently maintain a mortgage from several years ago. If prevailing market conditions offer refinancing opportunities, extracting equity simultaneously for renovations avoids the complexity and expense of two separate transactions. You close once, pay one set of closing costs, and streamline the entire process.

This strategy delivers multiple benefits:

The refinance-plus-improvement approach works particularly well when you’re already considering refinancing for other reasons—perhaps to eliminate mortgage insurance, shift from an adjustable rate to fixed terms, or modify your repayment timeline.

Separate home improvement financing sometimes makes more strategic sense:

Evaluate the total cost analysis including current mortgage terms, refinancing expenses, and your expected occupancy timeline.

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

What documents do lenders require for home improvement loan approval? Documentation requirements vary by loan structure, but most lenders evaluate your income stability, creditworthiness, existing debt obligations, property value, and renovation project specifics before approving financing.

Understanding these requirements before applying helps streamline the process and avoid delays. Lenders need to verify both your ability to repay and the reasonableness of your renovation plans.

All home improvement loan applications require baseline financial verification:

How does employment type affect home improvement loan documentation? Self-employed borrowers, business owners, 1099 contractors, and those with non-traditional income often face additional documentation requirements compared to W-2 employees, though specialized loan programs accommodate these situations.

Renovation financing requires additional documentation beyond standard loan applications:

Lenders use this documentation to verify your renovation plans are realistic, properly scoped, and likely to deliver the projected value increase that justifies the loan amount.

Can you get a home improvement loan with 1099 income or bank statement documentation? Yes, specialized loan programs accommodate self-employed borrowers, business owners, and those with non-traditional income through alternative documentation methods that verify income differently than standard W-2 employee processes.

These programs may evaluate:

Explore all loan programs to find documentation approaches that match your income situation.

Should you finance improvements before listing your home for sale? Strategic renovations funded through short-term financing can significantly increase sale price and marketability, often delivering returns that exceed financing costs when projects target high-impact improvements.

Sellers frequently face a dilemma: their property needs updates to command premium pricing, but they lack liquid capital to fund improvements before listing. Home improvement loans solve this timing problem by providing upfront capital repaid at closing from sale proceeds.

This approach particularly benefits:

What renovations deliver the highest return on investment? Kitchen updates, bathroom renovations, flooring replacement, fresh paint, and curb appeal improvements typically generate strong returns relative to cost, while highly personalized or over-improved features may not recoup investment in every market.

Before financing pre-sale improvements, analyze whether projected returns justify the costs:

If updated homes in your market command significantly higher prices and your property requires only moderate investment, financing improvements often proves financially advantageous.

Focus on improvements that maximize marketability relative to investment:

Avoid over-personalized renovations, luxury upgrades that exceed neighborhood norms, or extensive projects that significantly delay your listing timeline.

How do home improvement loan rates compare to other financing options? Interest structures and repayment terms vary significantly based on whether you choose secured financing backed by your home equity versus unsecured personal loan approaches, with secured options typically offering more competitive pricing due to collateral protection.

Understanding rate structures helps you evaluate true borrowing costs across different loan types. The lowest advertised pricing may not represent your actual cost once you factor in your specific credit profile, loan structure, and total repayment timeline.

Multiple variables affect the terms you’ll receive:

Are home improvement loan interest rates fixed or variable? Both options exist depending on loan structure, with fixed-rate installment loans providing payment predictability while variable-rate lines of credit may offer initial flexibility with exposure to market rate fluctuations.

When evaluating different home improvement loan options, analyze total project cost rather than focusing solely on nominal pricing:

A slightly higher rate on a flexible credit line might cost less total if you repay quickly, while a fixed-rate installment loan provides certainty for longer repayment periods.

Calculate your home improvement loan scenario:

Should you use a lump sum loan or a line of credit for home improvements? Your project timeline and scope determine the optimal financing structure—one-time installment loans work well for defined projects with fixed budgets, while revolving credit lines offer flexibility for phased renovations or uncertain timelines.

Matching your loan structure to renovation plans prevents paying interest on unused funds while ensuring capital availability when contractors need payment.

These provide all funds at closing in a single disbursement:

This structure works well when you have detailed contractor bids, a licensed contractor ready to begin work, necessary permits approved, and a clear project timeline from start to completion.

These provide access to funds you draw as needed:

How do renovation escrow accounts work with home improvement loans? Some lenders hold renovation funds in escrow accounts, releasing portions as contractors complete specific project milestones verified through inspections, protecting both borrower and lender from contractor performance issues.

Different renovation approaches favor different financing structures:

Project Type | Recommended Structure | Reasoning |

Kitchen remodel with fixed contractor bid | Lump sum installment | Defined scope, clear budget, set timeline |

Series of smaller improvements over time | Revolving credit line | Phased approach, uncertain total scope |

Major addition with architect and permits | Escrow-based renovation loan | Milestone-based progress, inspection requirements |

Emergency repairs plus future upgrades | Revolving credit line | Immediate needs plus flexibility for future projects |

Pre-sale improvements | Short-term bridge financing | Quick access, repayment from sale proceeds |

Consider how your project will actually unfold—if you’re managing multiple contractors, dealing with permit delays, or making decisions as work progresses, flexible credit lines may better serve your needs despite potentially different rate structures.

Can self-employed borrowers qualify for home improvement loans? Yes, multiple loan programs specifically accommodate business owners, 1099 contractors, freelancers, and others with non-traditional income through alternative documentation methods that verify income and repayment capacity without requiring standard W-2 employee documentation.

Traditional lending heavily relies on W-2 income documentation and tax returns showing stable employment. This approach creates challenges for self-employed borrowers whose business structures, deductions, and income reporting don’t fit conventional underwriting models.

Specialized loan structures accommodate various non-traditional situations:

How do bank statement home improvement loans work? Lenders analyze personal or business bank account deposits over a specific timeframe (typically 12-24 months), calculating average monthly income from deposit patterns and applying this to debt-to-income ratio analysis without requiring tax returns.

This approach particularly benefits business owners who maximize business deductions that reduce reported taxable income but maintain strong cash flow that demonstrates repayment capacity.

While alternative programs reduce traditional documentation, they require other verification:

These programs typically require stronger credit profiles and larger reserve requirements compared to standard documentation loans, offsetting the reduced income verification through other risk factors.

Can you use home improvement loans for rental property renovations? Yes, though qualification and structure differ from primary residence financing, with programs evaluating rental income potential or property cash flow rather than solely focusing on personal income documentation.

DSCR (Debt Service Coverage Ratio) loans for investment properties calculate whether the property’s rental income covers the mortgage payment plus renovation loan obligations, making your personal income less relevant to qualification.

Explore specialized programs:

View all loan programs to find options matching your income documentation situation.

Are home improvement loan interest payments tax deductible? Interest may be deductible if the loan is secured by your home and funds are used for substantial improvements that add value, prolong useful life, or adapt the property to new uses, though tax laws have specific limitations and requirements that warrant consultation with tax professionals.

Understanding tax implications helps you structure financing to maximize potential benefits while remaining compliant with IRS guidelines that distinguish between repairs, improvements, and capital projects.

The IRS draws important distinctions:

Why does the distinction between repairs and improvements matter for taxes? Improvements and restorations may be added to your home’s cost basis, potentially reducing capital gains when you eventually sell, while routine repairs generally cannot be added to basis or deducted unless the property is a rental.

For personal residence improvements, several factors affect deductibility:

Consult tax professionals for guidance specific to your situation, as tax laws change and individual circumstances vary significantly.

How do tax rules differ for investment property improvements? Rental property improvements follow different tax treatment, with costs potentially depreciable over time and interest generally deductible as rental property business expense, subject to passive activity loss limitations and other factors.

Investment property owners should work with tax professionals to optimize depreciation strategies, understand material participation rules, and coordinate improvement timing with overall tax planning.

The IRS provides detailed guidance on home improvement tax treatment in Publication 523 for primary residences and Publication 527 for rental property.

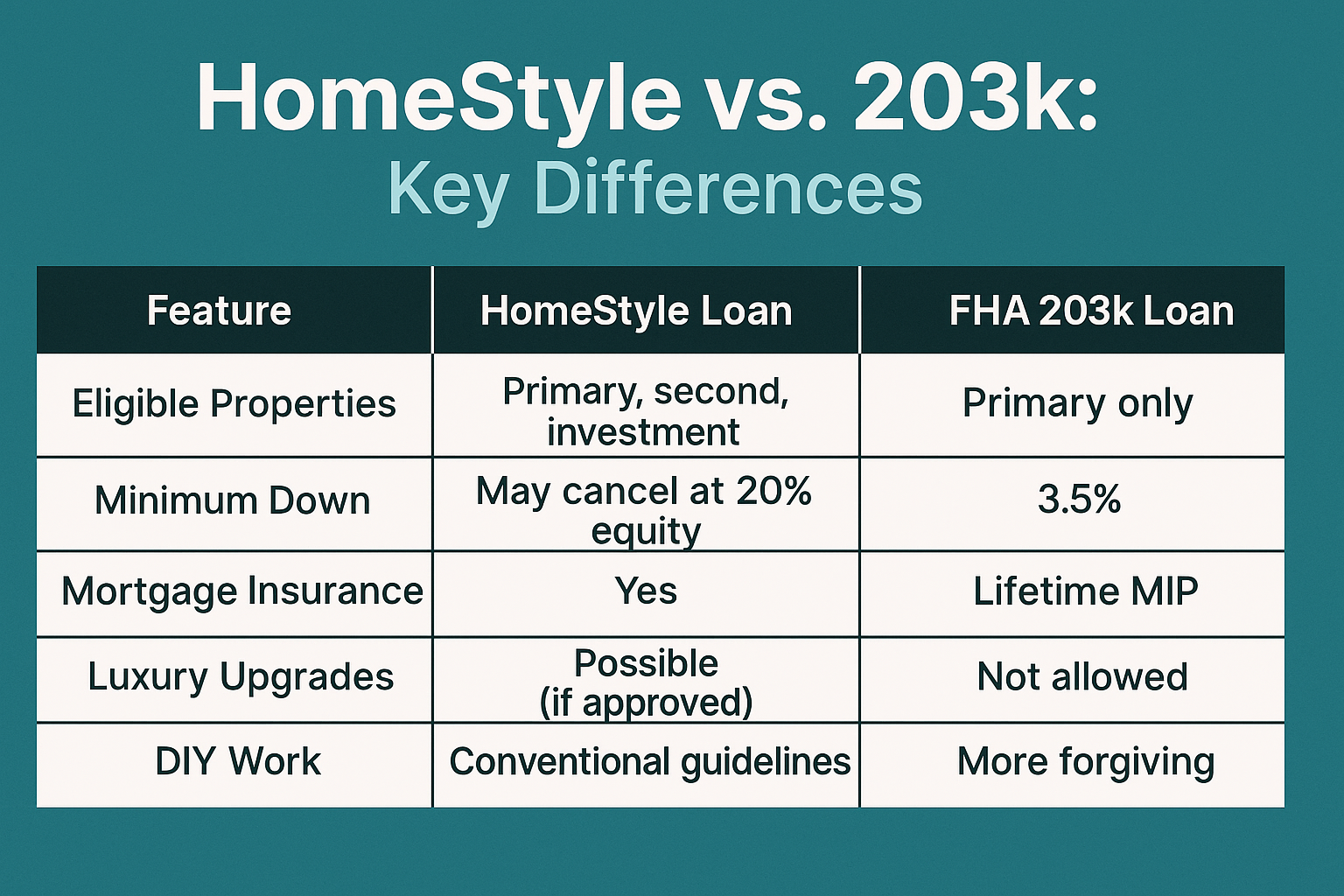

What government home improvement loan programs are available? Several federal programs facilitate renovation financing through FHA 203(k) loans, VA renovation loans, and USDA repair programs, each designed for specific borrower types and property situations with competitive terms backed by government guarantee.

These programs often provide advantages over conventional financing for borrowers who qualify, including potentially flexible credit requirements, competitive pricing, and the ability to finance both purchase and improvements in a single transaction.

The FHA 203(k) program allows borrowers to finance both home purchase (or refinance) and renovation costs through a single mortgage:

What types of improvements qualify for FHA 203(k) financing? Eligible projects range from minor repairs to major renovations including structural alterations, room additions, kitchen and bathroom remodels, energy efficiency upgrades, accessibility modifications, and remediation of health and safety issues.

The program particularly benefits:

Veterans and eligible service members can access renovation financing through VA-backed programs:

The USDA offers renovation assistance for rural properties:

Where can you find details on government home improvement loan programs? The Department of Housing and Urban Development provides comprehensive program information at HUD.gov, including eligibility requirements, approved lender lists, and application processes.

Can home improvement loans finance energy efficiency upgrades that reduce monthly costs? Yes, many borrowers use renovation financing to fund energy efficiency improvements that generate ongoing utility savings, potentially offsetting financing costs while improving comfort and increasing property value through reduced operating expenses.

Strategic energy investments often deliver compounding benefits: immediate comfort improvements, reduced monthly utility bills, increased property marketability, and potential tax credits or utility rebates that offset installation costs.

These improvements typically deliver strong returns relative to investment:

How do you calculate whether energy improvements justify financing costs? Compare projected monthly savings from reduced utility bills against monthly financing costs, calculating your break-even timeline and total savings over your expected occupancy period.

Many energy improvements qualify for financial incentives that reduce net cost:

Research available incentives before finalizing project scope, as some programs require pre-approval or have application deadlines.

Specialized financing programs target energy improvements:

The Database of State Incentives for Renewables & Efficiency provides comprehensive information on available programs by location.

What mistakes do borrowers make when choosing home improvement loans? Common errors include borrowing more than necessary, choosing inappropriate loan structures for their project timeline, failing to budget for contingencies, selecting contractors based solely on price, and not comparing total borrowing costs across different financing options.

Avoiding these pitfalls helps ensure your renovation financing supports your goals without creating unnecessary financial stress or limiting future flexibility.

How much should you borrow above contractor estimates for contingencies? Experienced renovators typically add buffer for unexpected issues, change orders, and cost overruns that frequently emerge during construction, particularly in older homes where hidden problems surface once work begins.

Underfunding your project creates stress when unexpected issues arise:

Budget realistic contingencies based on project scope:

Choosing contractors based solely on lowest bid often backfures:

Protect yourself through thorough contractor vetting:

Many lenders require licensed, insured contractors for renovation loan approval, so establish these relationships early in your planning process.

Should you use a HELOC or cash-out refinance for home improvements? The optimal choice depends on your current mortgage terms, total borrowing needs, project timeline, and whether you’re already considering refinancing for other reasons—each structure offers distinct advantages in different scenarios.

Common structure mismatches:

Analyze total costs across different structures using calculators before committing to one approach.

What costs beyond interest rates affect home improvement loan expenses? Origination fees, appraisal charges, title insurance, recording fees, and other closing costs can total several thousand dollars, making a slightly lower nominal rate more expensive overall if it comes with higher fees.

Calculate total borrowing cost:

A loan advertising competitive pricing may prove more expensive than alternatives when you factor in all costs, particularly if you plan to repay quickly.

Can you borrow too much for home improvements relative to neighborhood values? Yes, excessive improvements that push your property value far above comparable homes in your area often fail to recoup investment if you sell, as buyers typically won’t pay premium prices that exceed neighborhood norms regardless of your investment.

Research comparable sales before financing luxury upgrades:

Match improvement quality and scope to your neighborhood’s character unless you plan very long-term ownership where personal enjoyment justifies the investment.

What credit score do you need for home improvement loan approval? Requirements vary significantly by loan program and structure, with conventional equity-based financing typically requiring stronger credit profiles while alternative programs may accommodate lower scores with compensating factors like substantial equity, strong income, or significant reserves.

Understanding what lenders evaluate helps you prepare applications and address potential concerns before they delay approval.

Lenders analyze several credit factors:

How do recent late payments affect home improvement loan approval? While a single late payment may not disqualify you, patterns of late payments, recent 30-day late marks on mortgages, or multiple recent late payments across accounts signal higher risk and may require explanation letters or compensating factors.

Lenders need confidence in your repayment capacity:

Self-employed borrowers, business owners, and those with non-traditional income should explore specialized programs that accommodate alternative documentation:

What debt-to-income ratio do you need for home improvement loans? Most programs prefer total monthly debt obligations (including the new loan payment) to remain below specific thresholds relative to gross monthly income, though acceptable ratios vary by loan program, credit strength, and compensating factors.

Lenders calculate two ratios:

Improve your ratios by:

How much equity do you need for home improvement loans? Secured financing using your home as collateral requires sufficient equity to protect lender interests, with specific requirements varying by program—some conventional programs require substantial equity while government-backed options may work with minimal equity positions.

Equity calculations compare:

Borrowers with limited equity should explore:

The approval timeline depends on loan structure complexity, documentation completeness, and whether property appraisal is required. Simple unsecured personal loans may approve within days, while secured financing involving appraisals, title work, and renovation plan review typically requires several weeks from application to fund disbursement.

Factors affecting timeline:

Expedite the process by:

Borrowers with challenged credit can access renovation financing, though options narrow and pricing typically reflects higher risk. Strategies include secured financing leveraging substantial equity, adding co-borrowers with stronger credit, alternative documentation programs, working with specialized lenders, or taking time to improve credit before applying.

What can you do to improve home improvement loan approval chances with challenged credit? Provide detailed explanation letters for negative items, demonstrate recent positive payment history, show strong income and employment stability, offer larger reserves, increase your equity contribution, or address incorrect information on your credit report.

Alternative paths for challenged credit:

Credit cards rarely represent optimal renovation financing due to pricing structures, but may serve specific limited purposes. Small projects you can repay within promotional periods might work, while major renovations requiring extended repayment warrant structured loan products with competitive terms.

When credit cards might make sense:

When to avoid credit cards:

What factors should you evaluate when comparing home improvement loan options? Beyond interest rates, analyze total borrowing costs including all fees, repayment term flexibility, prepayment options, fund disbursement structure, lender reputation and service quality, and alignment between loan structure and your project timeline.

Create a comparison framework:

Factor | Offer A | Offer B | Offer C |

Loan structure | Lump sum | Credit line | Cash-out refi |

Total borrowing cost | All-in calculation | All-in calculation | All-in calculation |

Upfront fees | Itemized list | Itemized list | Itemized list |

Prepayment penalties | Terms | Terms | Terms |

Fund disbursement | Method and timeline | Method and timeline | Method and timeline |

Repayment flexibility | Options | Options | Options |

Request good faith estimates from multiple lenders showing all costs, then use calculators to compare total repayment costs under different scenarios.

How can you minimize total interest costs on home improvement loans? Develop a repayment strategy before borrowing that includes realistic monthly payment budgets, prepayment plans when cash flow allows, and potential refinancing opportunities if market conditions shift significantly during your repayment period.

Borrowing without a clear repayment plan often leads to extended debt duration and higher total costs than necessary.

Even modest additional payments dramatically reduce total interest and repayment timeline:

Do home improvement loans have prepayment penalties? Some loan structures include prepayment penalties that charge fees if you repay early, particularly on larger loans where lenders expect to earn interest over longer terms—always review prepayment terms before selecting a loan.

Integrate home improvement loan repayment with broader financial planning:

Market conditions may create refinancing opportunities during your repayment period:

Monitor market conditions and your financial profile for potential refinancing windows that could reduce total costs or improve your financial flexibility.

Calculate your home improvement loan scenario:

Ready to discuss your purchase scenario? Submit a purchase inquiry to explore your options.

How does rental property home improvement loan interest deductibility work? Interest on loans used to improve rental properties generally qualifies as deductible business expense on Schedule E of your tax return, subject to passive activity loss limitations and proper documentation proving fund usage for qualifying improvements rather than personal use.

Rental property owners should:

The IRS provides comprehensive guidance in Publication 527 covering rental income and expenses.

Do you have to pay off home improvement loans when you sell your property? Yes, all loans secured by the property must be paid at closing from sale proceeds, while unsecured personal loans remain your obligation regardless of property sale—this distinction affects how much net proceeds you’ll receive.

Secured home improvement debt:

Unsecured debt:

Yes, renovation financing exists for second homes and investment properties, though terms, qualification requirements, and structures differ from primary residence financing. Investment property programs often focus on rental income or debt service coverage rather than solely personal income, while second home programs may require larger reserves and equity positions.

How do DSCR loans work for investment property improvements? Debt Service Coverage Ratio loans evaluate whether the property’s rental income will cover all debt obligations including the improvement loan, making your personal income less relevant to qualification—particularly useful for investors with multiple properties or complex personal income situations.

Explore investment property options:

Property division during divorce creates unique challenges with home improvement loans. If one spouse retains the property, they typically must refinance to remove the other spouse from loan obligations or assume the loan with lender approval. If selling, improvement loan balances are paid from proceeds before equity division.

Can one spouse be removed from a home improvement loan without refinancing? Most lenders won’t release a co-borrower from loan obligations without full loan payoff or refinancing, as the original underwriting included both borrowers’ income and credit—removal changes the risk profile substantially.

Divorcing couples should:

Can retirees on fixed income qualify for home improvement loans? Yes, multiple programs accommodate retirees through alternative qualification methods including asset-based lending that evaluates liquid reserves rather than income, reverse mortgage programs that don’t require monthly payments, and conventional programs that recognize retirement income from pensions, Social Security, and investment distributions.

Options for senior borrowers:

Seniors should consider:

Explore senior-focused options:

Want to explore if a reverse mortgage fits your situation? Submit a reverse mortgage inquiry to learn more.

Should you use a construction loan or home improvement loan for major renovations? Construction loans apply to ground-up building or extremely substantial renovations essentially creating a new structure, while home improvement loans fund renovations to existing livable properties—the distinction affects loan structure, draw schedules, and qualification requirements.

Construction loans typically:

Home improvement loans:

Are ADU construction costs eligible for home improvement loan financing? Yes, adding accessory dwelling units, in-law suites, or rental units qualifies as home improvement and can be financed through renovation loan programs, though lenders will evaluate the project’s impact on property value and may have specific requirements for permitted legal secondary units.

ADU financing considerations:

Lenders evaluate whether the ADU will be:

ADU projects often benefit from after-repair value lending since the improvement substantially increases property worth.

How do bridge loans work for renovation timing? Bridge loans provide short-term financing when you need immediate renovation funds before receiving expected capital from property sale, business proceeds, or other sources—particularly useful for pre-sale improvements or projects with imminent payoff sources.

Bridge loan characteristics:

Common bridge scenarios:

If a home improvement loan isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

FHA 203(k) Rehabilitation Loan Program – Official HUD resource detailing standard and limited 203(k) programs, eligible improvements, contractor requirements, and application processes for combining purchase or refinance with renovation financing.

IRS Publication 523: Selling Your Home – Comprehensive IRS guidance on home sale exclusions, capital improvements that increase cost basis, and tax treatment of various home-related expenses for primary residences.

IRS Publication 527: Residential Rental Property – Official IRS resource explaining tax treatment of rental property expenses, depreciation rules for improvements, and deductibility guidelines for investment property financing.

Consumer Financial Protection Bureau Home Loan Resources – Federal consumer protection agency providing educational resources on mortgages, refinancing, home equity loans, and borrower rights throughout the lending process.

National Association of Home Builders Remodeling – Industry trade association offering market research, contractor resources, and consumer guidance on renovation planning, contractor selection, and project management.

Database of State Incentives for Renewables & Efficiency (DSIRE) – Comprehensive database of federal, state, and local incentives for energy efficiency and renewable energy improvements, including tax credits, rebates, and financing programs.

Energy Star Home Improvement Guide – EPA resource providing guidance on energy-efficient home improvements, qualified products, potential savings estimates, and available tax credits for energy upgrades.

Appraisal Institute Home Valuation Resources – Professional appraisal organization offering consumer resources on property valuation, understanding appraisals, and how improvements affect home value.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and contractors in your area.

Ready to get started? Apply now or schedule a call to discuss your situation.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.