Traditional mortgages require monthly payments that strain budgets, especially for retirees on fixed incomes. Reverse mortgages flip this model, allowing homeowners 62 and older to convert home equity into accessible funds without monthly mortgage payments—the loan balance grows over time and gets repaid when you sell, move, or pass away. Understanding how reverse mortgages work, who benefits most, what protections exist, and how to structure withdrawals helps you make informed decisions about accessing your home’s value while aging in place with greater financial flexibility and security.

Ready to explore your options? Schedule a call with a loan advisor.

A reverse mortgage is a loan that allows homeowners age 62 and older to convert home equity into cash without selling their property or making monthly mortgage payments—instead of paying the lender each month like traditional mortgages, the lender pays you while loan balance and interest accumulate over time, becoming due when you permanently leave the home through sale, relocation, or death.

How does a reverse mortgage differ from a home equity loan? Home equity loans require monthly payments from your income and can result in foreclosure if you can’t pay, while reverse mortgages have no monthly payment requirement and can’t force you out as long as you meet basic obligations like paying property taxes, maintaining insurance, and keeping the home in good condition.

The fundamental shift reverses the traditional mortgage model. With conventional mortgages, you make payments reducing loan balance while building equity over time. With reverse mortgages, you receive payments or access funds while loan balance increases, gradually reducing your equity position until repayment occurs.

Understanding when and how repayment occurs:

Loan becomes due when:

Repayment options for heirs:

What happens if the reverse mortgage balance exceeds the home’s value? HECM reverse mortgages include non-recourse provisions meaning you or your heirs never owe more than the home’s value at repayment time—FHA mortgage insurance covers any shortfall, protecting borrowers and heirs from owing more than the property is worth.

Three main reverse mortgage categories exist:

Home Equity Conversion Mortgage (HECM):

Proprietary (Jumbo) Reverse Mortgages:

Single-Purpose Reverse Mortgages:

Which reverse mortgage type should you choose? Most borrowers use HECM loans due to federal protections, widespread availability, and comprehensive counseling requirements—proprietary reverse mortgages make sense only for high-value homes exceeding HECM limits, while single-purpose options work if available in your area for specific approved expenses.

Who qualifies for a reverse mortgage? Homeowners must be at least 62 years old, own the property outright or have substantial equity, live in the home as their primary residence, meet financial assessment standards showing ability to pay ongoing property charges, and complete HUD-approved counseling for HECM loans—property must also meet FHA standards and be an eligible property type.

Understanding complete eligibility criteria helps you assess whether reverse mortgages fit your situation and what preparation might improve your qualification odds.

Age determines both eligibility and loan amounts:

How much more do older borrowers receive? Payment amounts increase with age—a 62-year-old might access approximately 50-55% of home value, while an 82-year-old might access 65-75% depending on interest rates and property value, though exact percentages vary based on multiple factors and change as program parameters adjust.

Your home equity position determines available proceeds:

Minimum equity standards:

Eligible property types:

Ineligible property types:

Can you get a reverse mortgage on a condo? Yes, if the condominium project meets FHA approval standards—the building must be on HUD’s approved condo list or receive spot approval, have adequate insurance and reserves, meet owner-occupancy requirements, and satisfy other FHA condominium project standards similar to forward mortgages.

HECM programs include financial qualification requirements:

What happens if you don’t meet financial assessment standards? Lenders may require a “Life Expectancy Set Aside” (LESA) where they withhold portion of loan proceeds to pay future property taxes and insurance on your behalf—this reduces your available proceeds but allows approval for borrowers who might otherwise be declined due to income concerns.

The home must serve as your main residence:

What happens if you need to move to assisted living temporarily? Brief stays under 12 consecutive months for medical care typically don’t trigger loan maturity—however, if you’re absent more than 12 months even for legitimate reasons, the loan becomes due and must be repaid.

Are reverse mortgage costs higher than traditional mortgages? Yes, reverse mortgages typically involve higher upfront costs including origination fees, FHA mortgage insurance premiums, and third-party charges—additionally, ongoing costs include mortgage insurance premiums, service fees, and accumulating interest that compounds over time, though no monthly payments are required.

Understanding complete cost structure helps you evaluate whether reverse mortgage benefits justify expenses and how costs affect your net proceeds and remaining equity over time.

Several fees apply at closing:

Origination fee:

FHA mortgage insurance premium (MIP):

Third-party costs:

Counseling fee:

Can reverse mortgage closing costs be financed? Yes, most closing costs can be rolled into the loan balance rather than paid out of pocket—this preserves your cash but increases the loan balance from day one, reducing your available credit line or proceeds and increasing total interest accumulation over time.

Continuing charges throughout the loan term:

Annual mortgage insurance premium:

Servicing fees:

Interest accumulation:

Property charges you must pay:

How quickly does a reverse mortgage balance grow? Growth rate depends on interest rates and ongoing costs—with interest around 6-7% annually plus 0.5% mortgage insurance, loan balance increases roughly 6.5-7.5% per year through compound interest, though actual growth varies based on specific loan terms and market conditions.

Evaluate costs relative to alternatives:

Are reverse mortgage costs worth it? For seniors with limited income who need home equity access while aging in place, the no-monthly-payment structure often justifies costs despite premiums over traditional loans—however, younger borrowers or those with adequate income for home equity loans might find traditional borrowing more cost-effective.

Want to explore if a reverse mortgage fits your situation? Submit a reverse mortgage inquiry to learn more.

What payment options do reverse mortgages offer? HECM reverse mortgages provide flexible withdrawal structures including lump sum at closing, monthly payments for fixed terms or life, line of credit you can draw from as needed, or combination approaches using multiple payment methods—your choice affects available amounts, flexibility, and strategic planning opportunities.

Selecting the optimal payment structure requires understanding your cash flow needs, risk tolerance, long-term plans, and strategic goals for the proceeds.

Five main withdrawal methods exist:

Lump sum:

Tenure payments:

Term payments:

Line of credit:

Modified tenure or modified term:

Which payment structure is most popular? Line of credit has become most common due to flexibility—you can withdraw funds as needed while unused portions grow, providing both current access and increasing emergency reserves, with ability to take monthly draws mimicking payment structures if desired while maintaining control over timing.

The credit line growth feature creates unique benefits:

How does reverse mortgage credit line growth work? Your available credit line increases annually at the same rate as interest and mortgage insurance charges accumulate—if you start with $200,000 available credit and leave it unused with 6.5% growth rate, after 10 years you’d have roughly $370,000 available, regardless of home value changes.

Strategic benefits:

Should you take a reverse mortgage just to establish a growing credit line? Some financial planners advocate taking HECM line of credit even without immediate need, allowing it to grow as standby reserve—this strategy works best if you can afford closing costs and the growing credit line serves specific estate planning or emergency reserve purposes in your comprehensive financial plan.

Modified structures blend approaches:

Example combination:

Combinations work well when you need:

Are reverse mortgage proceeds taxable income? No, reverse mortgage funds are loan proceeds, not income, making them non-taxable—you don’t report reverse mortgage distributions on tax returns as income, though interest accumulating on the loan balance isn’t deductible until actually paid (typically at loan repayment), and proceeds may affect eligibility for certain government benefits based on asset testing.

Understanding tax and benefit implications helps you structure reverse mortgages to minimize negative impacts on your overall financial situation.

IRS treatment clarifies taxation questions:

Non-taxable proceeds:

Interest deductibility:

Capital gains considerations:

Can reverse mortgage interest be deducted if you pay it down voluntarily? Potentially yes if you make voluntary interest payments during the loan term and itemize deductions, though most borrowers don’t voluntarily pay interest since the no-payment feature is the primary reverse mortgage benefit—consult tax professionals for guidance on your specific situation.

Different programs treat reverse mortgage proceeds differently:

Programs generally not affected:

Programs potentially affected:

How can you protect government benefit eligibility? Spend down reverse mortgage proceeds in the month received to avoid them counting as assets, use proceeds for exempt expenses like home repairs or medical care that don’t increase countable assets, structure distributions strategically to align with benefit rules, or consult with benefits specialists before proceeding if you receive asset-tested assistance.

Strategic approaches minimize impacts:

For detailed tax guidance:

Seeing how other seniors have used reverse mortgages helps you understand practical applications:

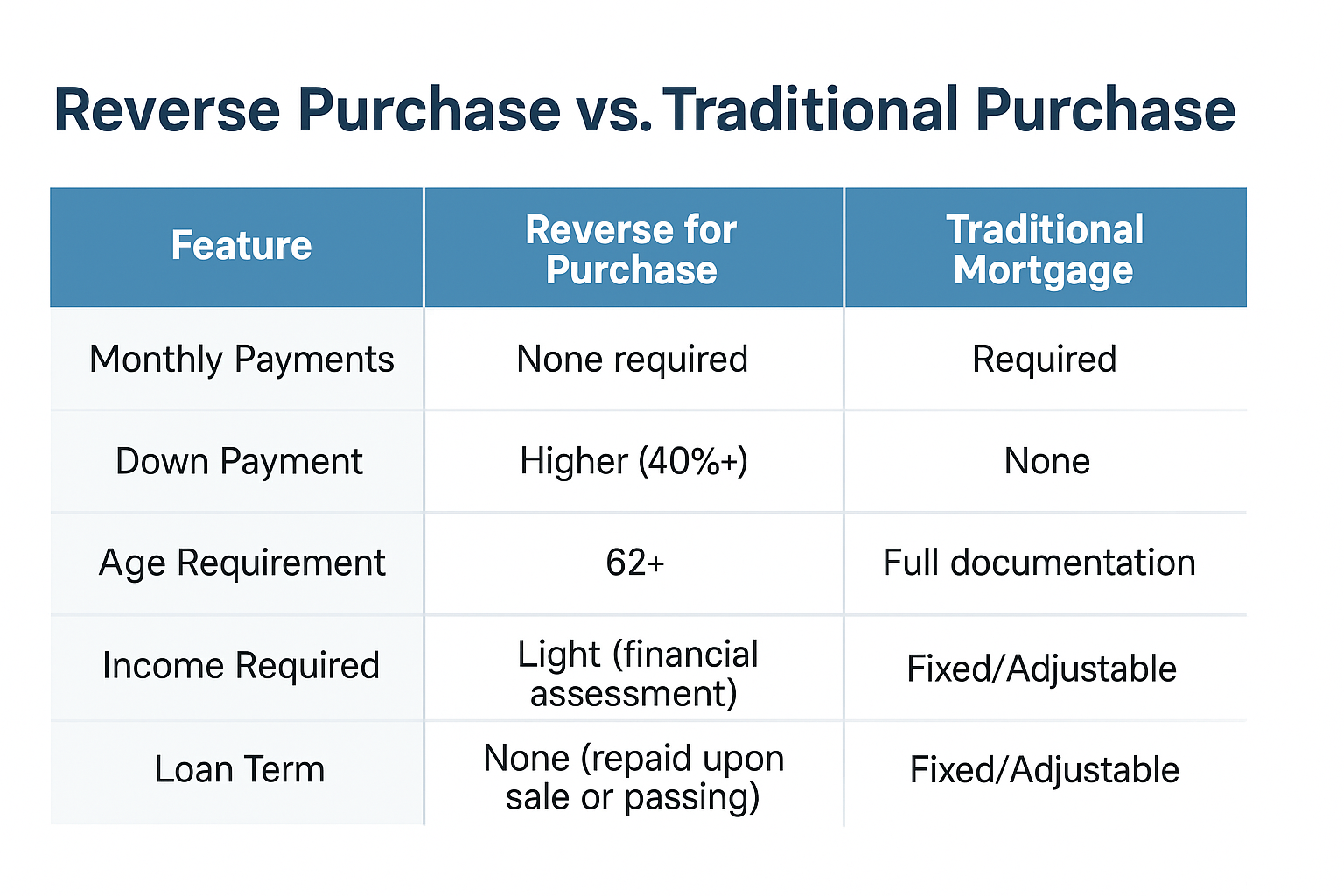

Purchase scenarios:

View reverse mortgage purchase case studies – Real examples of seniors using reverse mortgages to purchase new homes without monthly payments

Cash-out refinance scenarios:

View reverse mortgage cash-out refinance case studies – Examples of homeowners accessing equity for various purposes while eliminating mortgage payments

Payment elimination scenarios:

View reverse mortgage refinance case studies – Cases where existing mortgage payments were eliminated through reverse mortgage refinancing

Income supplement scenarios:

View reverse mortgage income case studies – Examples of seniors creating monthly income streams from home equity

These real examples demonstrate how reverse mortgages solve different financial challenges across various situations and property types.

What happens to a reverse mortgage if one spouse dies? If both spouses are borrowers, the surviving spouse continues living in the home with no changes—however, if only one spouse is on the reverse mortgage and that spouse dies first, historically the non-borrowing spouse faced potential displacement, though current HECM rules provide protections allowing eligible non-borrowing spouses to remain in the home.

Understanding spouse protections and requirements helps couples structure reverse mortgages to protect both parties regardless of who passes away first.

HECM loans originated after August 4, 2014 include non-borrowing spouse protections:

Requirements for protection:

How protection works:

Why would one spouse not be on the reverse mortgage? If one spouse is under age 62, they cannot be a borrower—couples must decide whether to wait until both reach 62 (potentially reducing proceeds due to younger age calculation) or proceed with one borrower while protecting the younger spouse through eligible non-borrowing spouse provisions.

Different timing strategies affect proceeds and protections:

Both spouses as borrowers (both over 62):

One spouse as borrower with non-borrowing spouse protection:

Should you wait until both spouses are 62? Decision depends on your need timeline, age gap, health situations, and financial circumstances—larger age gaps create more significant proceed differences, while immediate financial needs may outweigh waiting several years, and health concerns might make proceeding with available protections more prudent than delaying.

Additional factors affect spouse protection planning:

What happens if non-borrowing spouse can’t afford property charges? If the non-borrowing spouse cannot pay property taxes, insurance, or maintain the home after the borrowing spouse dies, the loan can become due even with protections in place—ensuring adequate income sources or setting aside funds for these obligations is critical.

Do you lose ownership of your home with a reverse mortgage? No, you retain title and ownership throughout the loan—the lender has a lien against the property securing the loan, just like with traditional mortgages, but you maintain ownership, can leave the property to heirs, and retain all homeowner responsibilities and benefits including any appreciation in property value beyond the loan balance.

Understanding common myths helps you evaluate reverse mortgages accurately rather than dismissing them based on misconceptions.

The truth: You retain complete ownership and title to your property. The reverse mortgage is simply a loan secured by your home, identical to how traditional mortgages work—the lender has a lien but no ownership interest. You remain on title, can make decisions about the property, receive any appreciation beyond the loan balance, and can sell whenever you choose.

The truth: You cannot lose your home as long as you meet basic obligations—living in the home as your primary residence, paying property taxes, maintaining homeowner’s insurance, and keeping the property in reasonable condition. Unlike traditional mortgages, you cannot be foreclosed for failure to make monthly mortgage payments because no monthly payments exist. The only ways to lose your home are violating these basic requirements or voluntarily selling or leaving.

The truth: Reverse mortgages include non-recourse protection meaning neither you nor your heirs will ever owe more than the home’s value—if the loan balance exceeds property value when it becomes due, FHA insurance covers the difference and heirs can walk away without obligation. Your heirs have options to repay the loan and keep the home, sell the property and keep any remaining equity, or let the lender sell the home with no deficiency judgment possible.

The truth: While scams targeting seniors exist, legitimate reverse mortgages are heavily regulated financial products—HECM loans require HUD-approved counseling to educate borrowers, have federal oversight and consumer protections, and are offered by FHA-approved lenders. Scams typically involve third parties trying to sell you unnecessary products or services, not the reverse mortgages themselves. Working with reputable lenders and completing mandatory counseling protects against fraud.

How can you avoid reverse mortgage scams? Work only with HUD-approved lenders, complete mandatory counseling with independent HUD-approved counselors, never pay large upfront fees to third parties promising to “help” with applications, avoid anyone encouraging you to deed your home to them, don’t let contractors or financial advisors pressure you into reverse mortgages to buy their services, and report suspicious activity to authorities.

The truth: While reverse mortgages help seniors with limited income access home equity, they’re also used by affluent retirees as strategic financial planning tools—financial planners increasingly recommend reverse mortgage credit lines as emergency reserves, portfolio diversification, or methods to delay Social Security while drawing on home equity, making them potentially valuable tools across various economic circumstances.

The truth: You can have existing mortgages or liens when obtaining a reverse mortgage, but they must be paid off at closing using reverse mortgage proceeds—many borrowers use reverse mortgages specifically to eliminate monthly mortgage payments by paying off their existing loans, freeing up monthly income by removing that payment obligation.

What happens to your existing mortgage? The reverse mortgage proceeds first pay off any existing mortgage balance at closing, and you receive access to the remaining equity after satisfying existing liens—this eliminates your previous monthly mortgage payment while giving you access to additional equity beyond what was needed for the payoff.

Should you take a reverse mortgage at 62 or wait until older? This strategic decision depends on immediate financial needs, the value of credit line growth, expected longevity, home appreciation projections, and alternative income sources—waiting allows larger proceeds from age-based calculations and potentially higher home values, while starting early maximizes credit line growth years and addresses immediate financial needs.

Understanding the tradeoffs helps you time reverse mortgage decisions optimally for your situation.

Taking a reverse mortgage earlier provides advantages:

Credit line growth potential:

Eliminate mortgage payments sooner:

Lock in current terms:

What’s the risk of waiting too long? Future health issues might prevent qualification, program changes could reduce benefits or availability, home value declines would reduce available proceeds, or life changes might make you ineligible (moving to care facility, extended medical absence)—establishing the loan while healthy and eligible protects against these scenarios.

Waiting until older can provide advantages:

Higher proceeds from age:

Home appreciation potential:

Lower total interest accumulation:

Alternative income sources:

Should you establish a line of credit even without immediate need? Some financial planners advocate this strategy—establish a HECM line of credit in your 60s, leave it unused while it grows, and draw from it later if needed—this approach works best if you can afford closing costs, plan to stay in the home long-term, and want the growing reserve as financial planning tool.

Factors to evaluate when deciding timing:

What happens to your home after you die with a reverse mortgage? Your heirs have several options—they can sell the home using proceeds to repay the loan and keep any remaining equity, refinance the reverse mortgage with traditional financing to keep the property, pay off the balance with other funds, or walk away if the loan exceeds the home’s value (non-recourse protection prevents deficiency claims).

Understanding estate implications helps you plan appropriately and communicate with heirs about expectations and options.

When the reverse mortgage becomes due, your heirs can choose:

Sell the property:

Refinance and keep the home:

Pay off with other funds:

Walk away from the property:

How long do heirs have to decide? Initially 30 days to inform lender of intentions, then typically 6 months to complete sale or refinancing with possible extensions to 12 months if actively working toward resolution—timelines vary somewhat by lender and circumstances, but acting promptly protects heirs’ interests and options.

Reverse mortgages affect what you leave behind:

Equity reduction:

Appreciation still benefits estate:

Example scenarios:

Can you protect inheritance while using a reverse mortgage? Life insurance represents one strategy—purchase or maintain life insurance with death benefit covering projected reverse mortgage balance, allowing heirs to pay off loan and keep home, or providing liquidity replacing equity consumed by the reverse mortgage.

Integrate reverse mortgages with comprehensive estate planning:

Should you avoid reverse mortgages to preserve inheritance? Not necessarily—if the reverse mortgage significantly improves your quality of life, provides needed funds for aging in place, or eliminates financial stress, these benefits may outweigh inheritance preservation, particularly if you discuss the decision with heirs and they understand the tradeoffs.

Yes, you can refinance an existing reverse mortgage to potentially increase your available credit (if home value increased or you’re now older), obtain better terms if rates have improved, change payment structures, or add a spouse who previously wasn’t eligible—however, refinancing involves new closing costs and fees, so benefits must justify these expenses.

When does reverse mortgage refinancing make sense? If your home has appreciated significantly providing access to substantially more equity, if you’re now considerably older increasing available proceeds meaningfully, if interest rates have dropped significantly, or if you need to add a spouse to the loan who has now reached 62—refinancing for marginal improvements often isn’t worth the costs.

Refinance considerations:

No, you must occupy the home as your primary residence to maintain reverse mortgage compliance—temporarily renting a room to a tenant might be acceptable depending on circumstances and lender policies, but converting the home to a rental property or moving out while renting to others violates occupancy requirements and triggers loan maturity.

What happens if you need to move to assisted living or with family? Temporary absences under 12 consecutive months for medical reasons are generally acceptable—however, if you’re absent more than 12 consecutive months even with legitimate reasons, the reverse mortgage becomes due and must be repaid regardless of intent to eventually return.

Occupancy considerations:

Yes, reverse mortgages are available for condominium units if the project meets FHA approval requirements—the condo building must be on HUD’s approved condo list or receive spot approval, maintain adequate insurance and reserves, meet owner-occupancy ratios, and satisfy other FHA condominium standards similar to forward mortgage requirements.

What makes a condo ineligible for reverse mortgages? High investor concentration exceeding limits, pending or active litigation, insufficient reserves, excessive commercial space, inadequate insurance coverage, or structural issues can disqualify projects—additionally, co-ops typically don’t qualify for HECM reverse mortgages though some proprietary products might be available.

Condo-specific considerations:

Credit history is less important for reverse mortgages than traditional mortgages, but financial assessment still reviews your credit to evaluate willingness to meet financial obligations—seriously delinquent taxes or federal debts, recent mortgage foreclosure, or patterns indicating unwillingness to pay obligations can create challenges, though many credit issues that would prevent traditional mortgage approval don’t automatically disqualify reverse mortgage applicants.

What credit issues cause reverse mortgage denial? Recent foreclosure, outstanding federal tax liens, delinquent property taxes on the subject property, or patterns showing unwillingness to meet financial obligations—additionally, if financial assessment determines you lack ability to pay property taxes and insurance going forward, you may be declined or face mandatory set-aside requirements reducing proceeds.

Credit and financial assessment considerations:

Filing bankruptcy doesn’t automatically trigger reverse mortgage maturity, but bankruptcy trustees may require selling the home to satisfy creditors if sufficient equity exists beyond the reverse mortgage balance and bankruptcy exemptions—reverse mortgage borrowers can file bankruptcy and potentially remain in their homes if they have little equity beyond the loan balance and their situation qualifies for bankruptcy protection.

Should you consider reverse mortgages to avoid bankruptcy? Using reverse mortgage proceeds to pay debts and avoid bankruptcy is a significant decision requiring professional legal and financial advice—while reverse mortgages can provide funds to manage debt, the proceeds are limited and the decision should consider all alternatives, long-term implications, and whether bankruptcy might actually serve your interests better.

Bankruptcy considerations:

You can have a HELOC or other lien before getting a reverse mortgage, but all existing liens must be paid off with reverse mortgage proceeds at closing—after obtaining a reverse mortgage, you generally cannot take out additional liens against the property as this would violate reverse mortgage terms requiring the lender to maintain first lien position.

Why can’t you add a HELOC after getting a reverse mortgage? Reverse mortgage lenders require first lien position on the property as primary protection for their loan—allowing additional liens would reduce their security and create complications, so reverse mortgage agreements prohibit additional borrowing against the home without lender permission (rarely granted).

Lien considerations:

Should you consider alternatives before getting a reverse mortgage? Yes, reverse mortgages serve specific purposes well but aren’t optimal for every situation—evaluating alternatives like home equity loans or HELOCs, downsizing and relocating, spending down other assets first, or seeking family assistance helps you determine whether reverse mortgages genuinely represent your best option or if simpler solutions might work better.

Comprehensive evaluation ensures you’re not choosing reverse mortgages simply because you haven’t fully explored other approaches.

Traditional equity borrowing offers alternatives:

Home equity loan advantages:

Home equity loan disadvantages:

When home equity loans work better:

When reverse mortgages work better:

Relocating to smaller or less expensive homes provides equity access:

Downsizing advantages:

Downsizing disadvantages:

When downsizing makes more sense than reverse mortgages:

Using retirement accounts or investments before tapping home equity:

Asset drawdown advantages:

Asset drawdown disadvantages:

When using other assets first makes sense:

Borrowing from or receiving support from family members:

Family assistance advantages:

Family assistance disadvantages:

When is family assistance appropriate? Only when family members genuinely have capacity to help without jeopardizing their own financial security, clear written agreements exist documenting terms, all parties understand and accept the arrangement, and relationships can withstand potential complications—family money often creates complex dynamics requiring careful navigation.

See how other seniors have successfully used reverse mortgages:

Calculate your reverse mortgage scenarios:

If a reverse mortgage isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

HUD HECM Reverse Mortgage Information – Department of Housing and Urban Development’s official resource center for Home Equity Conversion Mortgages providing program details, borrower protections, counseling requirements, and lender approval lists.

Consumer Financial Protection Bureau Reverse Mortgage Guide – Federal consumer protection agency offering educational resources on reverse mortgages, borrower rights, costs, risks, and alternatives to help seniors make informed decisions.

IRS Publication 936: Home Mortgage Interest Deduction – Official IRS guidance on mortgage interest deductibility including treatment of reverse mortgage interest, limitations on deductions, and reporting requirements for itemized returns.

National Council on Aging Reverse Mortgage Resources – Nonprofit organization serving older Americans providing objective reverse mortgage education, benefits checkup tools, financial planning resources, and counseling referrals for seniors considering home equity conversion.

AARP Reverse Mortgage Information – Membership organization for Americans 50+ offering comprehensive reverse mortgage guidance, scam warnings, calculator tools, and educational materials helping seniors evaluate whether reverse mortgages fit their situations.

National Reverse Mortgage Lenders Association – Trade association representing reverse mortgage industry providing consumer education, lender directories, market data, and resources on responsible reverse mortgage origination and servicing.

Financial Industry Regulatory Authority Reverse Mortgage Guide – Financial industry regulatory organization offering investor protection resources including reverse mortgage education, cost comparisons, risk analysis, and guidance on evaluating products.

Social Security Administration Benefit Programs – Official information on Social Security retirement benefits, Medicare, Supplemental Security Income, and other programs that may interact with reverse mortgage proceeds in planning your retirement income strategy.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and contractors in your area.

Ready to get started? Apply now or schedule a call to discuss your situation.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.