Your home equity represents potentially hundreds of thousands of dollars in untapped financial power. A Home Equity Line of Credit (HELOC) gives you flexible access to this wealth without disrupting your existing mortgage, providing a financial safety net and opportunity fund that adapts to your changing needs over time.

Ready to explore your options? Schedule a call with a loan advisor.

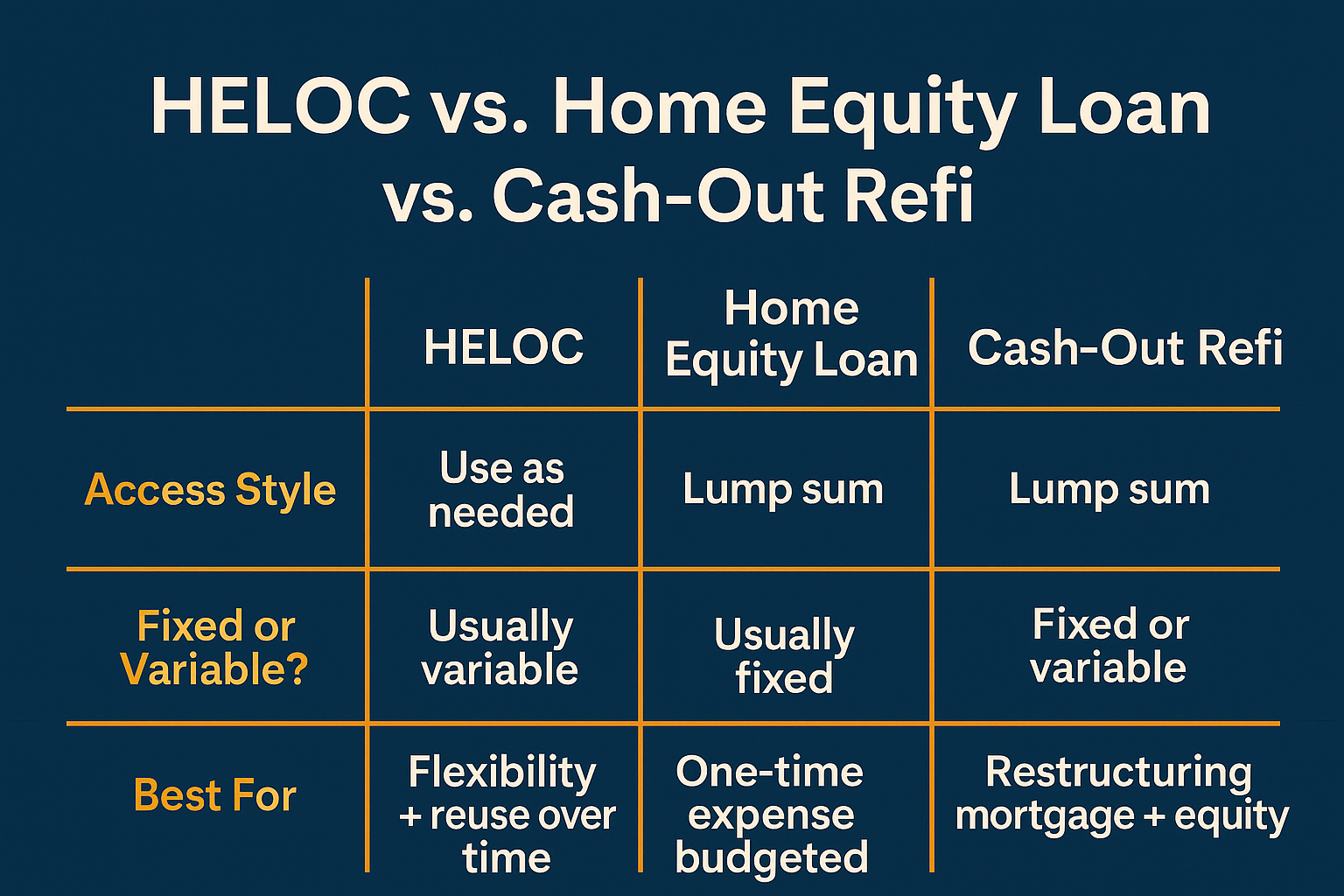

A Home Equity Line of Credit (HELOC) is a revolving credit line secured by your home’s equity—the difference between your property’s current value and what you owe on your mortgage. Unlike traditional loans that provide a lump sum, a HELOC works like a credit card: you can borrow, repay, and borrow again up to your credit limit during the draw period.

How does a HELOC give you financial flexibility that other loan types can’t match? The revolving nature means you only pay interest on what you actually use, not the entire credit limit. You can access funds whenever needed without reapplying, making it ideal for ongoing projects, unpredictable expenses, or multiple financial goals over time.

Most HELOCs operate in two distinct phases:

Draw period (typically 5-10 years): You can access funds up to your credit limit and make interest-only payments or pay down principal voluntarily. Many HELOCs provide checks, debit cards, or online transfer capabilities for easy access.

Repayment period (typically 10-20 years): The line closes to new borrowing and converts to a standard amortizing loan where you repay both principal and interest until the balance is eliminated.

Understanding your equity access options helps you choose the right tool:

HELOC advantages:

Home equity loan characteristics:

Cash-out refinance considerations:

For borrowers with excellent first mortgage terms who want flexible access to equity, HELOCs typically offer the most efficient solution.

What’s the smartest way to finance renovations that boost your home’s worth? HELOCs offer several advantages for home improvement projects:

Strategic renovation financing benefits:

High-return improvement projects particularly suited for HELOC financing:

The revolving nature perfectly matches renovation timelines—draw funds for materials as contractors need them, repay during pauses between phases, and access additional funds for subsequent projects.

Why keep tens of thousands in a low-interest savings account when you can access equity instantly? A HELOC serves as an emergency fund that doesn’t sacrifice investment returns:

Emergency HELOC strategy advantages:

Common emergency scenarios where HELOCs provide valuable backup:

Having available credit prevents desperate financial decisions during crises. You’ll maintain better sleep knowing you have substantial backup funds accessible without selling investments at inopportune times or disrupting long-term financial plans.

Consolidating expensive credit card balances, personal loans, or other high-interest debt into a HELOC can dramatically reduce interest costs:

Debt consolidation benefits:

Critical considerations for debt consolidation:

Debt consolidation through HELOCs works brilliantly for financially disciplined borrowers who accumulated debt through specific circumstances (medical bills, business investments, one-time expenses) rather than ongoing overspending patterns.

Calculate potential savings and develop a strategic payoff plan before consolidating to ensure this approach genuinely improves your financial position.

How can real estate investors and entrepreneurs leverage home equity for business growth? HELOCs provide flexible capital for wealth-building opportunities:

Investment and business financing applications:

The revolving structure particularly benefits real estate investors who:

Business owners appreciate the ability to access capital without diluting ownership through investors or navigating complex business loan requirements. The speed and flexibility of HELOCs enable seizing time-sensitive opportunities that traditional financing would miss.

Important note: Investment and business uses typically aren’t tax-deductible. Consult tax and financial advisors to understand the full implications of using home equity for these purposes.

Considering using equity for investments? Submit a refinance inquiry to explore if a HELOC makes sense for your goals.

Education financing through HELOCs can offer advantages over traditional student loans:

Education financing considerations:

When HELOC education financing makes sense:

Important considerations:

HELOC education financing works best for borrowers with stable income, clear repayment capacity, and education investments with strong return-on-investment potential.

How can you buy your next home before selling your current one? HELOCs solve timing challenges in competitive real estate markets:

Bridge financing advantages:

This strategy requires:

Many homeowners find this approach less stressful than coordinating simultaneous closing dates or living in temporary housing while searching for their next home.

Once your current home sells, you can repay the HELOC from sale proceeds, eliminate the overlap, and maintain the line for future needs.

Retirees and pre-retirees can use HELOCs strategically to enhance financial flexibility:

Retirement HELOC applications:

Retirement-specific considerations:

Retirees with substantial home equity but limited liquid assets often benefit from HELOC access, particularly when coordinated with tax-efficient withdrawal strategies from retirement accounts.

Working with financial advisors who understand both investments and home equity strategies ensures HELOC usage aligns with your overall retirement plan.

Explore all loan programs to compare equity access options.

Who qualifies for a Home Equity Line of Credit? Lenders evaluate several key factors when considering HELOC applications.

Your available equity directly determines your maximum HELOC amount:

Equity calculation basics:

Most lenders allow borrowing that keeps your total debt (first mortgage plus HELOC) within certain limits relative to your home’s value. The exact percentage varies by lender, credit profile, and property characteristics.

Factors affecting maximum borrowing capacity:

Higher equity positions and stronger financial profiles typically access more favorable terms and higher credit limits.

What credit profile do you need for HELOC approval? Requirements vary by lender and program type:

Credit evaluation factors:

Lenders consider your complete financial picture, not just credit scores. Strong compensating factors like substantial equity, high income, or significant reserves can sometimes offset credit concerns.

Lenders verify your ability to handle HELOC payments alongside existing obligations:

Income verification methods:

Your total monthly debt obligations relative to your gross income influences approval and credit limit decisions. Lower debt ratios demonstrate greater capacity to handle HELOC payments comfortably.

Debt-to-income considerations:

Stronger income documentation and lower existing debt burdens generally result in larger credit lines and better terms.

Your property must meet lender standards and be accurately valued:

Property eligibility factors:

Professional appraisals determine your property’s current market value, which directly impacts your available credit. Appraisers evaluate:

Strong property values in appreciating markets maximize your available equity and borrowing capacity.

What should you prepare before applying for a HELOC? Gathering documents early streamlines the approval process:

Essential documentation checklist:

Income verification:

Asset verification:

Property documentation:

Identity and credit:

Organized documentation demonstrates your preparedness and professionalism, often resulting in faster processing and fewer follow-up requests.

After application submission, lenders order property appraisals and begin underwriting:

Appraisal process:

Underwriting evaluation:

Underwriters may request additional documentation or clarification during their review. Prompt responses keep your application progressing smoothly toward approval.

Most HELOC applications process within 2-4 weeks from complete application to closing, though timelines vary based on appraisal scheduling, documentation complexity, and lender workload.

Once approved, you’ll attend a closing to sign final documents and establish your credit line:

Closing process:

Methods for accessing HELOC funds:

Most HELOCs activate immediately upon closing, giving you instant access to your approved credit line.

Right of rescission: For HELOCs on primary residences, federal law provides a three-day rescission period after closing during which you can cancel without penalty. The line becomes accessible after this period expires.

What payment obligations do you have while accessing your HELOC? Draw period payment structures vary by lender:

Common draw period payment options:

Interest typically accrues on your outstanding balance and compounds monthly. Your payment amount fluctuates based on your balance and current interest rate (since most HELOCs have variable rates).

Payment example concept: If you’ve drawn funds from your line, you’ll make monthly payments based on that outstanding amount. As you repay principal, your balance and payments decrease. If you draw additional funds, your balance and payments increase.

Many borrowers appreciate interest-only options during draw periods, as they provide maximum flexibility. However, paying down principal during the draw period reduces your balance and creates available credit for future needs.

Calculate your HELOC scenario:

Under what circumstances might HELOC interest be deductible? Tax treatment depends on how you use the funds:

Current IRS guidance indicates HELOC interest may be deductible when funds are used to buy, build, or substantially improve your home—the property securing the loan. Interest on funds used for other purposes typically isn’t deductible under current tax law.

Potentially deductible uses:

Typically non-deductible uses:

Tax laws are complex and change periodically. Consult qualified tax professionals who understand your complete financial situation before making decisions based on tax considerations.

Proper documentation tracking how you use HELOC funds supports your tax position if the IRS questions deductibility.

How does your HELOC change when it converts to repayment? Understanding this transition helps you plan effectively:

End of draw period changes:

Payment increase example concept: During draw period with interest-only payments, your monthly obligation might be relatively modest. When converting to full amortization, payments often increase substantially as you begin repaying principal over the remaining term.

Some lenders offer options to refinance or modify your HELOC as the draw period ends, potentially extending draw periods or adjusting repayment terms. Discussing options with your lender before transition helps you prepare for payment changes.

Most HELOCs don’t charge prepayment penalties, allowing you to repay your balance anytime without additional fees. However, some important considerations apply:

Early payoff considerations:

When early payoff makes sense:

When keeping the line open makes sense:

Many borrowers keep HELOCs open indefinitely even after repaying balances, treating them as permanent emergency reserves and opportunity funds.

What should you understand about HELOC rate structures? Most HELOCs use variable interest rates that adjust based on market indexes:

Variable rate mechanics:

Your actual interest costs fluctuate as the underlying index changes. When the Federal Reserve raises rates, HELOC rates typically increase. When the Fed lowers rates, HELOC rates typically decrease.

Rate risk management strategies:

Some HELOCs offer options to convert all or part of your balance to fixed rates for specific periods, providing predictability while maintaining line flexibility.

Can you transfer a HELOC to your next property? HELOCs are secured by specific properties and typically must be satisfied when selling:

Sale process HELOC considerations:

Calculate your net proceeds by subtracting all liens (first mortgage, HELOC, any other liens) plus selling costs from your sale price. Remaining equity becomes your available funds for your next purchase or other purposes.

After closing on your new home, you can apply for a new HELOC if you have sufficient equity and meet qualification requirements.

See how other homeowners have successfully used HELOC financing:

If a HELOC isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

Can you get a HELOC on rental properties? Yes, though requirements are stricter than primary residence HELOCs:

Investment property HELOC considerations:

Investment property HELOCs work well for real estate investors who:

Qualification typically requires demonstrating both personal income stability and rental property profitability, along with substantial reserves and equity positions.

Yes, borrowers with multiple properties can potentially establish HELOCs on each, subject to overall debt capacity and qualification:

Multiple HELOC management:

Real estate investors and second home owners often maintain multiple HELOCs, creating flexible capital access across their portfolio. This strategy provides liquidity without selling properties or disrupting existing favorable first mortgages.

Managing multiple HELOCs requires disciplined financial oversight, ensuring you maintain available capacity without overextending your debt obligations.

How does bankruptcy affect HELOC obligations? HELOCs are secured debts treated differently than unsecured obligations:

Bankruptcy and HELOC considerations:

If facing financial distress, communicating with your HELOC lender early often produces better outcomes than ignoring the situation. Many lenders offer hardship programs, temporary payment modifications, or workout arrangements preventing foreclosure.

Consulting bankruptcy attorneys and financial advisors helps you understand options and consequences before making decisions affecting your home equity and credit.

Many lenders offer fixed-rate conversion options providing payment predictability:

Fixed-rate conversion features:

When fixed-rate conversion makes sense:

Fixed-rate conversions provide middle ground between full HELOC flexibility and predictable home equity loan structures, allowing you to stabilize payments while maintaining access to remaining available credit.

Do HELOC draws increase your property’s tax basis? Generally no—borrowing against equity doesn’t change your cost basis:

Tax basis considerations:

Maintaining detailed records of how you use HELOC funds becomes important for:

Working with tax professionals ensures you properly handle HELOC-related tax implications and maximize available benefits under current tax law.

How does a HELOC affect your credit profile? Opening and managing a HELOC influences multiple credit factors:

Credit score impacts:

Ongoing credit management:

For most borrowers with good credit, opening a HELOC causes only minor, temporary score reductions, followed by score improvements from lower overall credit utilization and positive payment history.

Maintaining low HELOC balances relative to the credit limit optimizes credit score benefits while preserving access to funds.

Do reverse mortgages and HELOCs work together? Generally no—combining these products faces significant obstacles:

Reverse mortgage and HELOC conflicts:

Borrowers typically choose one product or the other based on their circumstances:

Choose reverse mortgage when:

Choose HELOC when:

Each product serves different financial goals and life stages, rarely working effectively together.

Can lenders freeze or reduce your HELOC during economic stress? Yes—lenders maintain certain rights to protect against declining property values:

Economic crisis HELOC impacts:

The 2008 financial crisis taught lenders that home values can decline dramatically, leaving them over-secured. Federal regulations allow lenders to freeze or reduce credit lines when property values drop or economic conditions create risk.

Protecting against HELOC disruptions:

Understanding these risks helps you incorporate HELOCs into financial plans appropriately without over-reliance on credit that could become restricted during the times you need it most.

How are HELOC debts handled after the borrower’s death? HELOCs become part of estate settlement:

Estate and HELOC considerations:

Estate planning with HELOCs:

Heirs who want to keep inherited properties must either pay off HELOCs from estate assets, refinance into new loans, or sell properties and satisfy liens from proceeds.

Planning for these scenarios ensures your estate can handle HELOC obligations efficiently without forcing rushed property sales or creating hardship for heirs.

Are HELOC terms fixed or negotiable? Many aspects of HELOC agreements involve some negotiation potential:

Potentially negotiable HELOC terms:

Strengthening your negotiating position:

Shopping among multiple lenders remains your most powerful negotiating tool—competitive pressure naturally produces better terms than simply accepting initial offers.

Consider the total cost and structure rather than focusing exclusively on interest rates. Low rates offset by high fees may cost more than slightly higher rates with minimal costs.

Ready to get started? Apply now or schedule a call to discuss your situation.

Consumer Financial Protection Bureau Home Equity Line of Credit Guide – Federal consumer protection agency resource explaining HELOC features, risks, costs, and borrower rights throughout the lending process.

Federal Reserve Consumer Guide to Home Equity Credit Lines – Comprehensive Federal Reserve publication covering HELOC mechanics, cost comparisons with alternatives, and smart borrowing strategies.

Federal Trade Commission Home Equity Lending Information – Federal guidance on shopping for home equity products, understanding terms, and avoiding predatory lending practices.

IRS Publication 936 Home Mortgage Interest Deduction – Official IRS guidance on mortgage interest deductibility rules including limitations and qualified residence definitions affecting HELOC interest.

IRS Home Improvement Tax Basis Guidelines – Federal tax information explaining how home improvements affect your property’s cost basis and capital gains calculations.

CFPB Mortgage Assistance Resources – Tools and information for mortgage shopping, understanding loan estimates, and resolving disputes with lenders.

Federal Reserve Truth in Lending Act Disclosures – Information about required HELOC disclosures protecting borrowers through transparent cost and term information.

Freddie Mac Home Equity Borrowing Guidance – Educational content comparing home equity access methods including HELOCs, home equity loans, and cash-out refinancing.

Need local expertise? Get introduced to trusted partners including loan officers, financial advisors, and real estate professionals experienced in home equity strategies in your area.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.