Buying a fixer-upper or renovating your current home doesn’t have to mean juggling multiple loans, contractors, and financial headaches. A HomeStyle Renovation loan combines your purchase or refinance with renovation costs into one convenient mortgage, giving you access to properties with incredible potential that other buyers might overlook.

Ready to explore your options? Schedule a call with a loan advisor.

A HomeStyle Renovation loan is a conventional mortgage product backed by Fannie Mae that allows you to finance both the purchase price (or current value for refinances) and renovation costs into a single mortgage. Instead of taking out a home equity loan or personal loan after closing, you can bundle everything together from the start.

Why consider a HomeStyle Renovation loan instead of traditional financing? This approach offers several distinct advantages that can save you time, money, and considerable hassle during the renovation process.

The loan is based on the “as-completed” value of your home—meaning lenders evaluate what your property will be worth after renovations are finished, not just its current condition. This allows you to borrow more than you could with a traditional mortgage and access properties that might otherwise be out of reach.

Traditional mortgages require you to complete renovations with separate financing, typically through:

HomeStyle Renovation loans eliminate this complexity by providing a comprehensive financing solution that covers:

This streamlined approach means you’ll have one monthly payment, one interest rate, and one closing process instead of coordinating multiple financial products.

Can you really save money buying a home that needs work? Absolutely—and a HomeStyle Renovation loan makes this strategy accessible to more buyers.

Properties requiring significant updates typically sell at a discount compared to move-in ready homes in the same neighborhood. By purchasing below market value and financing renovations through your mortgage, you can:

The key is identifying properties with good bones—solid structure, desirable location, and renovation needs that align with your budget and timeline. Your lender will require a detailed renovation plan and contractor estimates before approval, ensuring your project is feasible and financially sound.

Unlike home equity loans or HELOCs that require substantial existing equity, a HomeStyle Renovation refinance allows you to tap into your home’s future value. This is particularly valuable when:

The refinance pays off your existing mortgage and adds your renovation costs, all based on the projected “as-completed” value. This approach often results in better interest rates than alternative financing options while preserving your cash reserves for other financial goals.

What types of major repairs qualify for HomeStyle Renovation financing? The program covers a comprehensive range of structural improvements that enhance safety, functionality, and value:

Eligible structural projects include:

These aren’t just cosmetic updates—they’re investments that protect and enhance your property for decades. By financing these projects through your mortgage, you spread the cost over the life of the loan at competitive interest rates rather than depleting savings or using expensive short-term financing.

Sustainability and cost savings go hand-in-hand with HomeStyle Renovation loans. You can finance eco-friendly improvements that reduce your environmental footprint while decreasing monthly expenses:

Many of these improvements qualify for federal, state, or local tax incentives and rebates, further enhancing your return on investment. Lower utility bills mean more money available for other expenses or savings goals, making your renovation pay dividends long after completion.

Want to explore if a HomeStyle Renovation loan fits your renovation plans? Submit a purchase inquiry to discuss your specific scenario.

How can you make your home more accessible for long-term living? HomeStyle Renovation loans cover modifications that improve accessibility and support aging in place, allowing you to create a home that adapts to changing mobility needs:

Qualifying accessibility improvements:

These modifications not only enhance quality of life but also increase your home’s marketability to a broader range of buyers when you eventually sell. Planning for accessibility now can prevent the need for costly emergency modifications later.

Rather than tackling improvements piecemeal over several years, a HomeStyle Renovation loan allows you to complete multiple projects simultaneously. This approach offers significant advantages:

Time efficiency: Completing all work at once minimizes disruption to your daily life and reduces the total time contractors need on-site.

Cost savings: Contractors typically offer better pricing for comprehensive projects than for multiple small jobs, and you’ll only pay for mobilization, permits, and dumpsters once.

Design cohesion: Planning all improvements together ensures consistent style, quality, and functionality throughout your home rather than a patchwork of updates completed at different times.

Single financing event: You’ll only go through underwriting, appraisal, and closing once instead of seeking additional financing for each subsequent project.

Common comprehensive renovation packages include:

HomeStyle Renovation loans aren’t limited to basic repairs—you can also finance luxury upgrades that transform your house into your dream home:

While luxury amenities should align with your neighborhood’s value range to ensure good return on investment, they can dramatically improve your enjoyment of your home and make it a true reflection of your lifestyle and priorities.

Explore all loan programs to compare renovation financing options.

Who qualifies for HomeStyle Renovation financing? The program has specific requirements that balance accessibility with responsible lending practices.

HomeStyle Renovation loans follow conventional mortgage guidelines with some additional considerations:

Credit requirements:

Financial stability factors:

Income documentation:

The exact requirements vary based on your overall financial profile, the property type, and the scope of renovations. Working with an experienced loan advisor helps you understand where you stand and what steps might strengthen your application.

HomeStyle Renovation loans can be used for various property types:

What renovation projects are allowed? The program offers remarkable flexibility:

Permitted improvements include:

The renovation budget must be reasonable relative to the property’s after-renovation value, and all work must be completed by licensed contractors (with some exceptions for landscaping and non-structural cosmetic work).

Your HomeStyle Renovation journey begins with identifying the right property and understanding its potential. This involves:

For purchases:

For refinances:

Early consultation with your lender helps you understand budget constraints and ensures you’re evaluating properties or planning renovations that fit within program guidelines.

How do you select the right contractor for a HomeStyle Renovation project? Your contractor choice significantly impacts your project’s success and loan approval.

Contractor requirements and selection criteria:

Your lender will review all contractor bids and renovation plans during underwriting. This typically includes:

Having comprehensive, professional documentation strengthens your application and demonstrates the project’s feasibility.

HomeStyle Renovation loans require specialized appraisals that consider both current condition and planned improvements:

“As-is” appraisal: Determines the property’s current market value in its existing condition.

“As-completed” appraisal: Estimates the property’s value after all renovations are finished, based on contractor plans and comparable sales of similar upgraded properties.

The lender uses the as-completed value to determine your maximum loan amount. This means you can borrow based on your home’s future potential, not just its current state—a powerful advantage for buyers and homeowners with renovation vision.

Underwriters review your:

Once approved, you’ll close on the full loan amount (purchase price or existing mortgage plus renovation costs), but renovation funds are held in escrow and released as work is completed.

How do contractors get paid during a HomeStyle Renovation project? The loan includes a structured draw schedule that protects both you and your lender:

Typical draw process:

This structure ensures work is completed properly before contractors receive payment, providing quality control throughout the project. Most HomeStyle Renovation projects include a contingency reserve (typically around 10-15% of renovation costs) for unexpected issues that arise during construction.

During major renovations that make the property uninhabitable, the loan can include up to six months of mortgage payments, giving you financial breathing room while work is completed.

The total loan amount depends on several factors working together. Your borrowing capacity is based on the lesser of:

Renovation costs typically have no specific dollar cap but must be reasonable relative to the property’s value. Lenders generally expect renovation costs to fall within a certain percentage of the total project value to ensure the improvements make financial sense.

Your loan advisor can help you understand realistic renovation budgets for your specific property and location.

Calculate your HomeStyle renovation loan scenarios:

DIY work faces significant limitations with HomeStyle Renovation loans. Lenders require licensed contractors for most improvements to ensure quality, compliance with building codes, and proper inspections.

Generally prohibited for DIY:

Sometimes allowed with restrictions:

Even when DIY work is permitted, you cannot include sweat equity in your renovation budget—only actual material costs can be financed. The lender’s primary concern is ensuring work is completed safely, properly, and in a way that maintains or increases the property’s value.

What timeline should you expect for completing HomeStyle Renovation projects? Standard renovation periods typically span six months, though extensions may be granted for complex projects or circumstances beyond your control.

Timeline considerations:

Your contractor’s detailed timeline becomes part of your loan documentation, and inspectors verify progress against these milestones. Building realistic buffer time into your schedule helps accommodate unexpected issues without stress or deadline pressure.

Yes, closing costs can typically be included in your total loan amount, subject to the same maximum borrowing limits based on the as-completed value. This is particularly helpful for buyers who want to minimize cash needed at closing or homeowners refinancing who prefer to finance all costs.

Financed closing costs become part of your total mortgage balance and are repaid over the life of the loan. Your loan advisor can provide detailed breakdowns showing scenarios with different combinations of down payment, renovation costs, and closing costs to help you optimize your financial strategy.

How do you handle cost overruns during a HomeStyle Renovation project? Budget surprises can occur despite careful planning, especially when renovating older homes.

Options for managing additional costs:

Setting realistic budgets with experienced contractors and including adequate contingency reserves minimizes the risk of problematic cost overruns. Thorough inspections before creating renovation plans help identify potential issues that might increase costs.

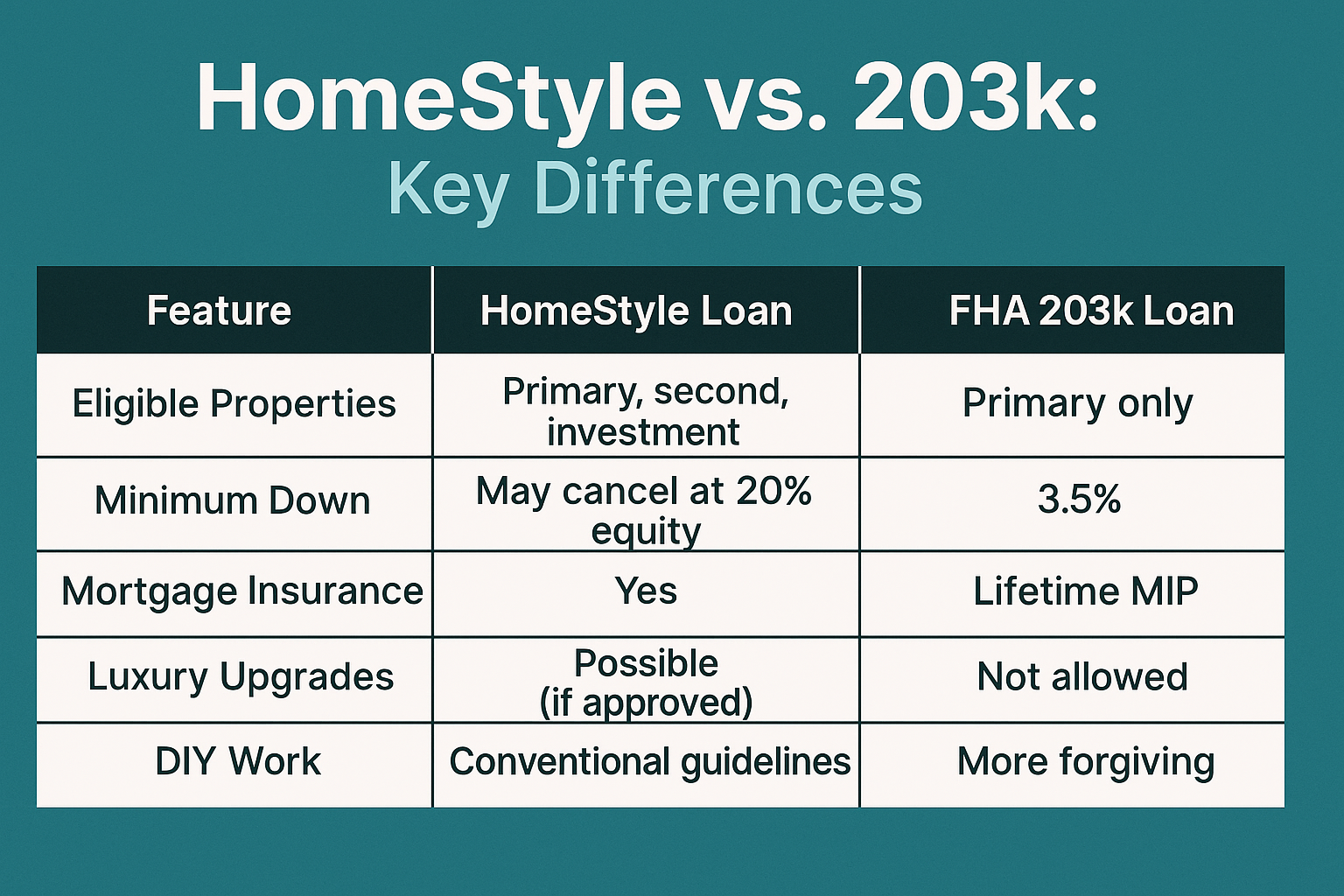

Both HomeStyle Renovation and FHA 203(k) loans serve similar purposes, but they have distinct differences that make each better suited for different situations:

HomeStyle Renovation advantages:

FHA 203(k) considerations:

Your specific financial situation, credit profile, property type, and renovation goals determine which program offers the best fit. Many borrowers find HomeStyle Renovation loans more flexible and cost-effective, particularly when they qualify for conventional financing.

See how other borrowers have successfully used HomeStyle renovation financing:

If a HomeStyle renovation loan isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

Yes, HomeStyle Renovation loans can finance investment properties, though requirements become more stringent. Investment property considerations include:

Different qualification standards:

Expanded opportunities:

The ability to base your loan on after-renovation value makes HomeStyle financing particularly attractive for real estate investors who see potential in undervalued properties. The renovated property can generate rental income while you repay a single mortgage at competitive rates.

Do HomeStyle Renovation loans require a consultant? Unlike FHA 203(k) loans, HomeStyle financing doesn’t mandate a renovation consultant, though some borrowers choose to hire one for complex projects.

When you might want a consultant:

Consultants typically charge fees based on project complexity and scope. While not required, their expertise can prevent costly mistakes and ensure smooth project execution, particularly for borrowers undertaking significant renovations for the first time.

Will your property taxes increase after renovations? Almost certainly, but timing and amounts vary by jurisdiction.

Tax assessment considerations:

Your lender factors projected property taxes into your debt-to-income ratio during underwriting, ensuring you can afford the full cost of ownership after improvements. Discussing potential tax implications with your loan advisor and local assessor helps you budget appropriately.

Yes, HomeStyle Renovation loans can finance properties in poor condition, including those deemed uninhabitable—a significant advantage over traditional financing that typically requires properties to meet minimum condition standards.

Uninhabitable property scenarios:

The program can include up to six months of mortgage payments if renovations prevent occupancy, giving you breathing room during construction. This capability opens opportunities to purchase properties at significant discounts that other buyers cannot finance.

Insurance coverage requires careful attention during HomeStyle Renovation projects. You’ll need:

Homeowners insurance:

Builder’s risk insurance:

Contractor liability insurance:

Your lender provides specific insurance requirements during the approval process. Adequate coverage protects your investment and ensures you’re not exposed to financial risk during the renovation period.

Can you use HomeStyle Renovation financing for attached properties? Yes, but additional considerations apply:

Condo and townhome specifics:

Interior renovations typically face fewer restrictions than exterior changes. Kitchen remodels, bathroom upgrades, flooring replacement, and similar improvements usually proceed smoothly. Exterior modifications like deck additions, window replacements, or landscaping may require HOA review and approval.

Working with your HOA early in the planning process prevents delays and ensures your renovation plans align with community standards and regulations.

Can you get extensions if renovations take longer than expected? Most lenders offer extension options for legitimate delays, though requirements vary.

Extension scenarios and solutions:

Extensions typically require:

Most lenders want to see projects completed successfully and work reasonably with borrowers facing legitimate obstacles. However, extensions aren’t guaranteed and shouldn’t be counted on when planning your timeline.

Should you worry about over-improving for your neighborhood? This legitimate concern requires thoughtful consideration during renovation planning.

Appraisers evaluate whether improvements are appropriate for the neighborhood by:

Strategic luxury upgrade approach:

Quality improvements within your neighborhood’s range almost always make sense. Ultra-luxury upgrades that substantially exceed area norms may not appraise for their full cost but can still be worthwhile if you plan to enjoy them for many years.

HomeStyle loans can finance two- to four-unit properties, offering unique opportunities for owner-occupants and investors:

Multi-unit advantages:

Multi-unit considerations:

Multi-unit HomeStyle Renovation financing can be particularly attractive for house-hackers who want to improve their property while building a real estate portfolio.

Why is thorough documentation critical during HomeStyle Renovation projects? Proper records protect your interests and ensure smooth processing.

Essential documentation to maintain:

This documentation serves multiple purposes:

Creating an organized filing system (physical or digital) from day one makes managing documentation much simpler than trying to compile everything at project completion.

Ready to get started? Apply now or schedule a call to discuss your situation.

Fannie Mae HomeStyle Renovation Mortgage Overview – Comprehensive guide covering program guidelines, eligible improvements, property requirements, and underwriting standards for HomeStyle Renovation financing.

Consumer Financial Protection Bureau Mortgage Resources – Federal resources explaining mortgage types, the home buying process, and your rights as a borrower throughout the transaction.

FHFA Conforming Loan Limit Information – Official Federal Housing Finance Agency data on maximum conventional loan amounts by county, updated annually to reflect market conditions.

Freddie Mac CHOICERenovation Program Details – Alternative renovation financing option with similar features to HomeStyle, including eligible properties and improvement types.

National Association of Home Builders Remodeling Resources – Industry insights on renovation trends, best practices, contractor selection, and home improvement ROI analysis.

HUD 203(k) Rehabilitation Mortgage Program – Information about FHA’s renovation loan alternative, useful for comparing program features and determining the best fit for your situation.

EPA Lead-Safe Renovation Requirements – Critical information about lead paint regulations for renovation projects in homes built before 1978, including contractor certification requirements.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, contractors, and home inspectors in your area.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.