Purchasing or refinancing a condominium becomes complicated when the property doesn’t meet standard “warrantable” status required by conventional lenders. Non-warrantable condo loans provide financing solutions for properties rejected by traditional programs due to high investor concentrations, pending litigation, commercial space percentages, inadequate reserves, or other factors that disqualify them from Fannie Mae and Freddie Mac guidelines. Understanding what makes condos non-warrantable, how alternative financing works, and how to position yourself for approval helps you access properties in buildings that most buyers can’t finance, potentially creating value opportunities in desirable locations.

Ready to explore your options? Schedule a call with a loan advisor.

A non-warrantable condo is a condominium property that doesn’t meet the eligibility requirements established by Fannie Mae and Freddie Mac for purchase on the secondary mortgage market. These government-sponsored enterprises set specific standards for condo projects they’ll accept as collateral, and properties failing to meet any of these criteria become “non-warrantable,” requiring alternative financing outside conventional lending channels.

Why do Fannie Mae and Freddie Mac have condo warrantability requirements? These standards manage risk in their mortgage portfolios by ensuring condo projects maintain financial stability, adequate insurance, appropriate owner-occupancy levels, and sound governance—properties meeting these criteria demonstrate lower default risk and more stable collateral values than projects with financial problems, governance issues, or unfavorable unit compositions.

The warrantability distinction creates a two-tier condo financing market. Warrantable condos access conventional financing with competitive terms, broad lender participation, and streamlined approval processes. Non-warrantable condos require specialized lending programs with stricter requirements, fewer participating lenders, and typically higher costs reflecting increased risk.

Multiple factors can render a condo project non-warrantable:

Can a condo project become non-warrantable after you purchase? Yes, projects can lose warrantable status due to changing conditions like declining owner-occupancy, financial deterioration, litigation filing, insurance lapses, or increased commercial activity—this shift affects refinancing options and future buyer pool since fewer people can obtain financing.

Non-warrantable status creates specific challenges:

Understanding these implications helps you evaluate whether a non-warrantable condo purchase makes sense for your situation and how to position yourself for successful financing.

How can you determine if a condo is non-warrantable before committing to purchase? Request the condominium questionnaire or project certification documents from the seller or HOA, review HOA financial statements and meeting minutes, research litigation records, evaluate owner-occupancy ratios, and work with lenders experienced in condo financing who can provide preliminary warrantability assessments before you make binding purchase commitments.

Discovering warrantability issues early prevents surprises during the mortgage approval process when you’ve already invested time and money in a property you may struggle to finance.

Research these critical elements before making offers:

Owner-occupancy ratio:

Commercial space percentage:

HOA financial reserves:

Litigation status:

Insurance coverage:

How do you obtain condo project documentation? Request condominium questionnaires directly from the HOA management company, ask the seller to provide recent HOA documents, review public litigation records through county court systems, and work with your real estate agent to gather comprehensive project information early in your search process.

Watch for warning signs during property research:

Should non-warrantable status automatically disqualify a condo from consideration? Not necessarily—non-warrantable properties may offer value opportunities with lower prices offsetting financing challenges, particularly if you have strong financial profile, substantial equity contribution, and plan long-term ownership, though you should understand the financing implications and ensure you can qualify for available programs.

Do non-warrantable condo loans have stricter requirements than conventional financing? Yes, alternative financing for non-warrantable condos typically requires higher credit scores, larger equity contributions, more substantial reserves, lower maximum debt-to-income ratios, and comprehensive documentation compared to warrantable condo loans—lenders offset the increased project risk through stronger borrower qualification standards.

Understanding these elevated requirements helps you assess whether you can qualify and what financial positioning might improve your approval odds.

Non-warrantable financing demands excellent credit profiles:

How do recent late payments affect non-warrantable condo loan approval? Even single late payments within recent timeframes can create approval challenges or affect pricing—lenders scrutinize payment history intensely since you’re combining higher project risk with mortgage obligations, requiring confidence in your financial discipline.

Larger equity contributions are standard for non-warrantable financing:

Typical equity requirements:

Why do non-warrantable condo loans require more equity? The combination of project-level risk (non-warrantable factors) and individual unit risk creates elevated lender exposure—larger borrower investment through substantial equity reduces potential losses if values decline or borrowers default, while demonstrating financial commitment and capacity.

Benefits of larger equity contributions:

Substantial liquid reserves beyond down payment are critical:

Minimum reserve expectations:

What assets count toward non-warrantable condo loan reserves? Checking accounts, savings accounts, money market funds, stocks, bonds, mutual funds in liquid brokerage accounts typically count at full value, while retirement accounts may receive discounted valuation (60-70%), and illiquid assets like real estate equity or business interests generally don’t qualify.

Conservative leverage improves non-warrantable approval odds:

How do high HOA fees affect non-warrantable condo loan qualification? Substantial association fees increase your total housing payment, potentially pushing you over debt-to-income limits even if the mortgage payment alone seems manageable—include the complete PITI+HOA payment when evaluating affordability and qualification capacity.

What specific issues most commonly cause non-warrantable status? Investor concentration exceeding limits, active litigation involving the association, commercial space percentages above thresholds, insufficient HOA reserves, and insurance coverage problems represent the most frequent disqualifiers—understanding which factors affect your target property helps you pursue appropriate financing and set realistic expectations.

Different non-warrantable factors create varying levels of financing difficulty, with some issues having workarounds while others create more substantial barriers.

What owner-occupancy ratio makes a condo non-warrantable? Most conventional programs require at least 50% of units be owner-occupied or sold to owner-occupants, with some programs requiring 51% or higher—projects falling below these thresholds where too many units are investor-owned or operated as rentals lose warrantable status.

Why investor concentration matters:

Can you finance a unit in a project with high investor concentration? Yes, through non-warrantable condo loan programs specifically designed for projects exceeding investor concentration limits—these programs evaluate the specific unit and project fundamentals rather than rejecting properties solely based on owner-occupancy ratios.

Factors lenders consider in high-investor projects:

Lawsuits involving the HOA create significant warrantability challenges:

What types of litigation affect condo warrantability? Construction defect cases, disputes with developers or builders, conflicts with management companies, environmental issues, accessibility claims, or significant disputes between unit owners and the association can all render projects non-warrantable—even meritless lawsuits disqualify projects until resolution or dismissal.

Litigation considerations:

How long does resolved litigation affect condo financing? Timeframes vary by lender and situation, but projects typically need 6-12+ months after litigation settlement before regaining warrantable status—lenders want certainty that issues are truly resolved and no related problems will emerge.

Financial health significantly affects project warrantability:

What HOA reserve percentage is considered adequate? Most guidelines suggest associations maintain reserves equal to at least 10% of the annual budget, though more complex or older projects may need higher percentages—associations with inadequate reserves or reserves declining over time signal financial stress affecting warrantability.

Reserve-related concerns:

Can you get financing if the HOA has low reserves? Non-warrantable condo loans can finance units in projects with reserve deficiencies, though lenders evaluate whether reserve levels create material risk of special assessments that would affect your ability to make mortgage payments—extremely low reserves or projects facing imminent major expenses create greater challenges.

Mixed-use projects frequently exceed commercial space thresholds:

What percentage of commercial space disqualifies a condo project? Conventional guidelines typically allow up to 25-35% commercial space depending on the specific program—projects exceeding these limits where commercial uses represent too much of the building become non-warrantable.

Commercial space includes:

Are condos in mixed-use buildings automatically non-warrantable? Not necessarily—if commercial space stays within the allowable percentage range, the project may maintain warrantable status, though projects marketed primarily as mixed-use developments often exceed these thresholds and require non-warrantable financing.

Ready to discuss your purchase scenario? Submit a purchase inquiry to explore your options.

Are non-warrantable condo loan rates higher than conventional financing? Yes, alternative financing for non-warrantable condos typically carries pricing premiums through higher interest rates, additional fees, or both—the increased project-level risk beyond standard underwriting factors reflects in program costs, though exact pricing varies significantly based on your credit profile, equity contribution, specific project issues, and chosen lender.

Understanding cost implications helps you evaluate whether a non-warrantable condo purchase makes financial sense and what pricing to expect during your search.

Multiple variables influence your specific pricing:

What’s a typical rate premium for non-warrantable condo financing? Premiums vary significantly but commonly range from fractions of a percentage point to multiple percentage points above comparable conventional financing depending on all risk factors—projects with minor warrantability issues and borrowers with excellent profiles see smaller premiums, while complex situations face larger spreads.

Beyond rate differences, additional costs may apply:

Are non-warrantable condo loan closing costs significantly higher? Total closing costs depend on specific lender fee structures—while some lenders charge premium fees for project review and additional underwriting, others maintain fee structures competitive with standard condo financing, making lender comparison important.

Evaluate the complete financial picture:

When do non-warrantable condo costs justify the expense? If the property offers significant value below comparable warrantable condos, provides unique location or amenity advantages worth the premium, represents excellent investment potential despite financing challenges, or fits your specific needs better than available warrantable alternatives.

Calculate your non-warrantable condo loan scenarios:

See how other condo buyers have successfully used non-warrantable condo financing:

What HOA financial factors should you evaluate beyond standard warrantability requirements? Association budget adequacy, special assessment history and likelihood, reserve study quality and age, delinquency rates among unit owners, insurance coverage limits and premiums, management company reputation, and pending major repairs all affect both financing approval and your long-term ownership costs regardless of technical warrantability status.

Thorough HOA financial analysis protects you from purchasing into projects with serious underlying problems that could create ongoing financial stress even if you successfully obtain financing.

Request and review these essential documents:

HOA budget and financial statements:

Reserve study:

Meeting minutes:

What red flags in HOA financials should concern you? Declining reserves over time, repeated special assessments, high delinquency rates, expenses consistently exceeding budget, minimal reserve contributions, deferred maintenance documented in minutes, insurance premium spikes or coverage reductions, and management company turnover all signal potential problems.

Evaluate likelihood of future assessments:

How do special assessments affect non-warrantable condo loan qualification? Pending or recently imposed special assessments must typically be paid before closing or included in your debt-to-income calculations—large assessments can affect both qualification and appraisal values, while recurring assessments signal chronic financial problems.

Adequate insurance protects your investment:

Master policy review:

Coverage concerns:

Why does HOA insurance matter if you have your own HO-6 policy? Your individual condo insurance (HO-6) provides secondary coverage after the master policy—inadequate master coverage creates gaps leaving you personally liable, while uninsurable buildings prevent you from obtaining financing regardless of other factors.

What condo project documents must you provide for non-warrantable financing? Comprehensive project documentation including complete condo questionnaires, HOA financial statements and budgets, reserve studies, meeting minutes, master insurance policies, declarations and bylaws, litigation details if applicable, and property management information—non-warrantable lending requires more extensive project analysis than warrantable financing due to increased complexity.

Thorough documentation helps underwriters understand project specifics and assess whether issues creating non-warrantable status represent manageable risk or significant concern.

All condo financing requires baseline project documents:

How current must condo documents be for loan approval? Most lenders require documents dated within specific timeframes (commonly 90-180 days), with financial statements ideally from the current or most recent fiscal year—outdated documentation requires updates before underwriting can proceed.

Projects with warrantability issues need supplemental documentation:

For litigation matters:

For investor concentration:

For commercial space:

For reserve deficiencies:

Can you proceed with incomplete condo documentation? No, lenders require complete project documentation before approving non-warrantable loans—missing documents delay underwriting, while HOAs that can’t or won’t provide required documentation may prevent financing entirely, requiring you to consider alternative properties.

Beyond project documents, expect standard mortgage documentation:

Self-employed borrowers may access alternative documentation:

Yes, refinancing non-warrantable condos follows similar underwriting to purchases, requiring evaluation of both current project status and your financial profile—rate-and-term refinances and cash-out refinances are both available through non-warrantable programs, though cash-out refinancing typically faces stricter loan-to-value limitations than rate-and-term transactions.

Does the condo need to remain non-warrantable to refinance? Not necessarily—if the project regains warrantable status by resolving previous issues, you may qualify for conventional refinancing with better terms, while projects remaining non-warrantable require continued alternative financing through specialized programs.

Refinance considerations:

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

What types of lenders offer non-warrantable condo financing? Portfolio lenders holding loans on their balance sheets, non-QM specialists focusing on alternative lending, some credit unions with flexible underwriting, and private lending sources provide most non-warrantable financing—conventional mortgage companies selling loans to Fannie Mae and Freddie Mac generally can’t help with non-warrantable properties.

Finding specialized lenders:

Should you tell your lender early that a condo is non-warrantable? Yes, disclose known warrantability issues immediately—working with lenders experienced in non-warrantable financing from the start prevents wasted time with lenders who can’t help, ensures realistic expectations on requirements and pricing, and allows proper structuring of your purchase contract timeline.

Yes, first-time homebuyers can qualify for non-warrantable condo financing, though the combination of first-time buyer and non-warrantable property creates challenges requiring particularly strong financial profiles—expect lenders to emphasize larger equity contributions, substantial reserves, excellent credit scores, and stable income when both factors are present.

What makes first-time buyers more challenging for non-warrantable financing? Lenders prefer borrowers with previous mortgage payment history demonstrating ability to manage housing debt, making first-time buyers inherently higher risk—combining this with non-warrantable project risk requires compensating factors through other underwriting elements.

First-time buyer strategies:

Not necessarily—the nature, severity, and potential impact of litigation determine warrantability more than mere existence of lawsuits—minor disputes with limited financial exposure may not affect warrantable status, while major construction defect cases, significant liability claims, or lawsuits threatening association financial stability typically create non-warrantable status.

What types of litigation are most concerning to lenders? Construction defect cases with potential large remediation costs, environmental hazards like mold or contamination, accessibility compliance lawsuits, structural integrity issues, or any litigation where potential judgments could create special assessments or materially affect property values.

Litigation evaluation factors:

Can you finance a condo if litigation recently settled? Possibly, though many lenders require waiting periods after settlement before approving financing—the wait period allows certainty that issues are resolved, no related problems emerge, and the association’s financial position stabilizes post-settlement.

Can a warrantable condo become non-warrantable after you own it? Yes, changing project conditions like declining owner-occupancy, new litigation, insurance problems, financial deterioration, or increased commercial activity can shift previously warrantable projects to non-warrantable status—this affects your ability to refinance and the future buyer pool when you decide to sell.

Impact on existing owners:

What can unit owners do about declining project status? Actively participate in HOA governance to prevent problems, vote for boards prioritizing financial health and proper management, oppose policies that might create non-warrantable factors, maintain adequate reserves through appropriate assessments, ensure quality property management, and address issues promptly before they become material problems.

Mitigation strategies:

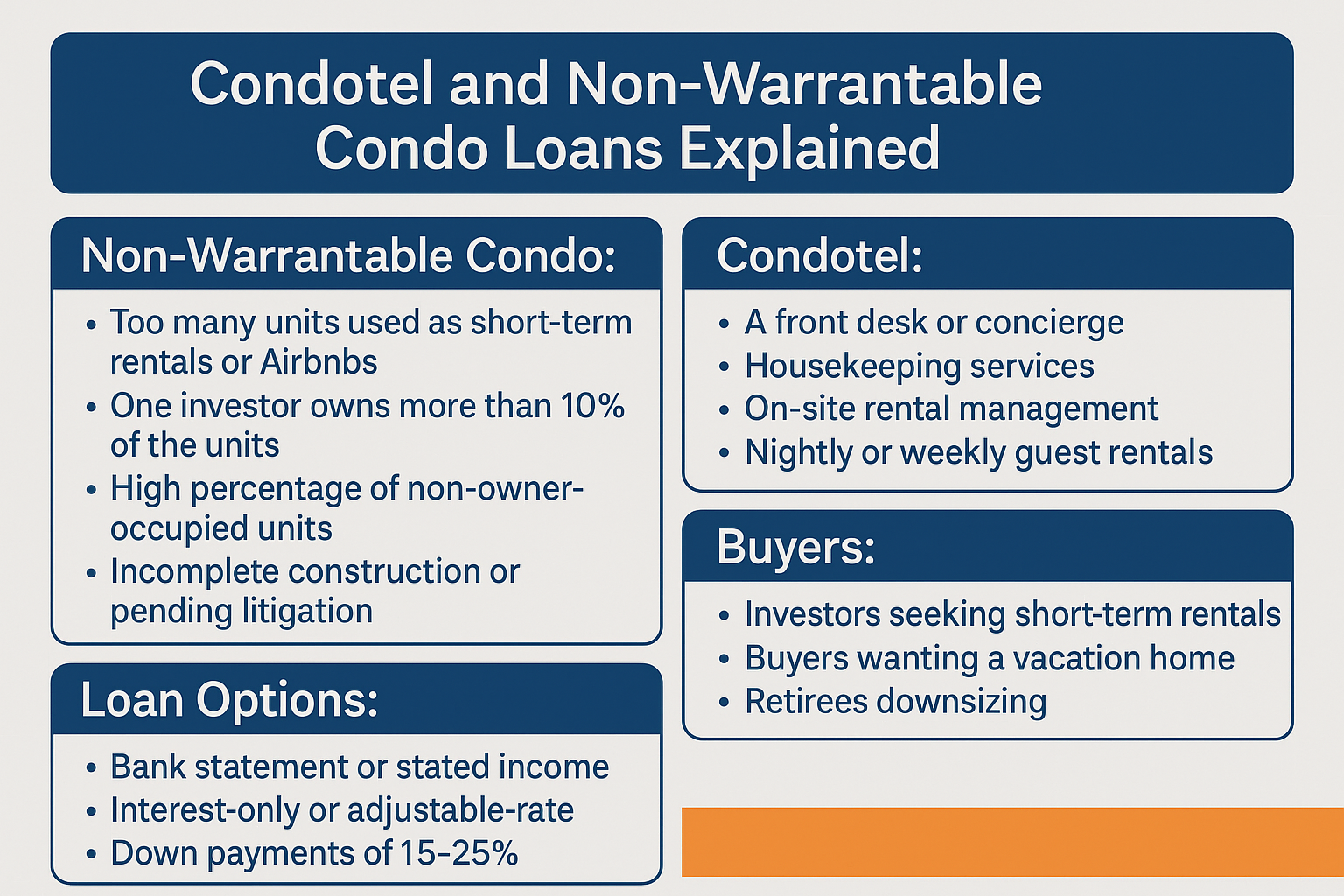

What are condotels and why are they typically non-warrantable? Condotels are condominium properties operated partially or primarily as hotels with units entering rental pools, offered to hotel guests, or managed by hotel operators—these properties almost universally fail warrantability requirements due to commercial operation, lack of owner-occupancy, hotel-style amenities and services, and business structures mixing residential ownership with hospitality operations.

Condotel characteristics:

Can you get financing for condotel units? Yes, through specialized non-warrantable programs designed specifically for these properties—requirements typically include substantial equity contributions (often 30-40%+), excellent credit profiles, significant reserves, and documentation acknowledging the property’s commercial nature and rental program participation.

Vacation condo considerations:

What advantages do portfolio lenders offer for non-warrantable condo financing? Banks and credit unions holding loans on their balance sheets rather than selling them can offer more flexible underwriting for complex projects, individualized risk assessment, accommodation of unique situations not fitting standardized guidelines, relationship-based decision making, and creative solutions for particularly challenging non-warrantable scenarios.

Portfolio lending provides customized approaches where standardized non-QM programs might still struggle with unusually complex situations.

These institutions provide unique advantages:

How do you identify portfolio lenders for non-warrantable condos? Research regional and community banks in your market, explore credit unions with real estate lending programs, ask real estate attorneys and CPAs for referrals to portfolio lenders, contact banks advertising “portfolio lending” or “balance sheet lending,” and work with mortgage brokers who maintain portfolio lender relationships.

Maximize portfolio lender benefits through strategic relationship development:

Can banking relationships actually affect non-warrantable condo approval? Yes, particularly with portfolio lenders who evaluate relationships holistically—substantial deposit relationships, existing loan performance, or multiple service usage can provide flexibility or improved pricing compared to applicants without institutional relationships.

Certain non-warrantable scenarios particularly benefit from portfolio approaches:

Explore portfolio lending options:

Can you use FHA or VA loans for non-warrantable condos? Generally no—FHA and VA have their own condo project approval processes separate from conventional warrantability, and projects failing Fannie/Freddie standards typically also fail FHA or VA requirements, though occasionally projects might qualify for FHA or VA despite being conventionally non-warrantable if specific issues don’t violate government program rules.

Understanding government-backed options helps you explore all potential financing avenues, particularly if you’re a first-time buyer or veteran who might otherwise benefit from these programs.

FHA maintains separate condo project certification:

FHA condo project requirements:

How do FHA condo requirements differ from conventional warrantability? Standards are similar in many respects, though specific thresholds and evaluation criteria differ—FHA maintains an approved condo project list where projects meeting standards receive certification streamlining individual unit financing, while projects not on the approved list face spot approval processes.

FHA spot approval (single-unit approval):

Can veterans use VA loans for non-warrantable condos? VA has its own condo project approval separate from conventional warrantability—occasionally projects might qualify for VA despite Fannie/Freddie non-warrantable status, though most projects failing conventional standards also fail VA requirements due to similar financial, legal, and composition standards.

Consider FHA or VA for specific situations:

Research government loan eligibility early in your condo search to understand whether these alternatives might provide better terms than non-warrantable conventional financing.

Should you purchase a non-warrantable condo as an investment property? Investment potential depends on multiple factors including purchase price discount versus warrantable comparables, rental income relative to financing costs, local rental demand, your ability to hold long-term if resale proves challenging, tax implications, and your overall investment strategy—non-warrantable status creates both challenges and potential opportunities.

Understanding investment dynamics helps you assess whether a non-warrantable condo represents a good opportunity or a potential problem.

Non-warrantable status affects pricing:

Typical price dynamics:

How much discount justifies non-warrantable challenges? No universal answer exists, but substantial discounts (10-20%+ below comparable warrantable condos) may offset higher financing costs and limited resale pool—evaluate whether the discount plus rental income or personal use value exceeds the premium you’ll pay through higher financing costs and potential difficulty selling.

For investment properties, cash flow drives decisions:

Do DSCR loans work for non-warrantable condos? Yes, DSCR investment property loans focusing on rental income coverage can finance non-warrantable condos—this combination works particularly well since DSCR loans already use alternative underwriting, and rental income-focused qualification aligns well with investment property analysis.

Explore DSCR financing for non-warrantable investment condos:

Consider your eventual exit:

Resale challenges:

Resale opportunities:

Hold strategy:

Should you expect non-warrantable condos to appreciate normally? Not necessarily—limited buyer pools from financing challenges may constrain appreciation relative to warrantable comparables, though well-located properties with strong fundamentals can still appreciate significantly over time, and projects resolving their non-warrantable issues may see value increases.

Calculate investment scenarios:

Can you improve your financing options by waiting for project status changes? Sometimes yes—if non-warrantable issues appear temporary or in the process of resolution, waiting until problems resolve may provide access to conventional financing with better terms, though you risk missing purchase opportunities or price increases if the property appreciates while you wait.

Strategic timing balances securing a good property against optimizing financing terms.

Evaluate the nature of non-warrantable factors:

Potentially temporary issues:

Likely permanent characteristics:

How long does it typically take for projects to regain warrantable status? Timelines vary dramatically—litigation settlement might clear in months, while owner-occupancy improvements could take years of turnover, developer sell-out depends on market conditions and inventory, and some issues may never fully resolve.

Track progress if you’re waiting:

Should you make offers contingent on warrantable status improvement? This typically doesn’t work well—sellers won’t accept offers contingent on future events outside their control, and warrantability determinations can take time—instead, structure normal contingencies protecting your earnest money while you evaluate financing options during due diligence periods.

Consider the tradeoffs:

Reasons to purchase despite non-warrantable status:

Reasons to wait or look elsewhere:

If a non-warrantable condo loan isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

Fannie Mae Condo Project Standards – Official Fannie Mae resource detailing condominium project eligibility requirements, warrantability standards, and guidelines that determine whether projects qualify for conventional financing purchase on the secondary market.

Consumer Financial Protection Bureau Mortgage Resources – Federal consumer protection agency offering educational resources on mortgages, homebuying, and borrower rights that apply to all mortgage types including non-warrantable condo financing.

FHA Condominium Project Approval Process – Department of Housing and Urban Development resource explaining FHA condo project certification requirements, approval processes, and guidelines for government-backed condo financing.

Community Associations Institute Resources – National organization serving community associations providing educational resources on HOA governance, financial management, legal issues, and best practices for condominium association operations and oversight.

National Association of Realtors Condo and Co-op Resources – Real estate professional organization offering condo market data, buying guidance, legal considerations, and resources for buyers, sellers, and agents working with condominium properties.

Mortgage Bankers Association Non-QM Lending Information – National trade association providing research, market trends, and industry perspective on non-qualified mortgage lending including non-warrantable condo financing and alternative documentation programs.

American Bar Association Real Estate Law Resources – Legal organization providing educational materials on real estate law, condominium governance, HOA legal issues, and property rights relevant to condo ownership and financing.

Federal Reserve Consumer Credit Resources – Central bank educational materials explaining mortgage markets, interest rate factors, and economic conditions influencing lending availability and pricing for all mortgage types.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and contractors in your area.

Ready to get started? Apply now or schedule a call to discuss your situation.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.