This case study is hypothetical and for educational purposes only. Scenarios, borrower profiles, loan terms, interest rates, and outcomes are illustrative examples and do not represent current offers or guaranteed terms.

For specific details including down payment requirements, closing cost estimates, interest rate details, closing cost breakdowns, payment calculations, cash-to-close estimates, or an official Loan Estimate, it is highly recommended you schedule a meeting with one of our licensed mortgage advisors.

Learn more:

Actual loan terms vary by credit profile, property, occupancy, location, market conditions, and lender guidelines. For current options tailored to you, schedule a consultation or apply online.

Ready to explore your options? Schedule a call with a loan advisor.

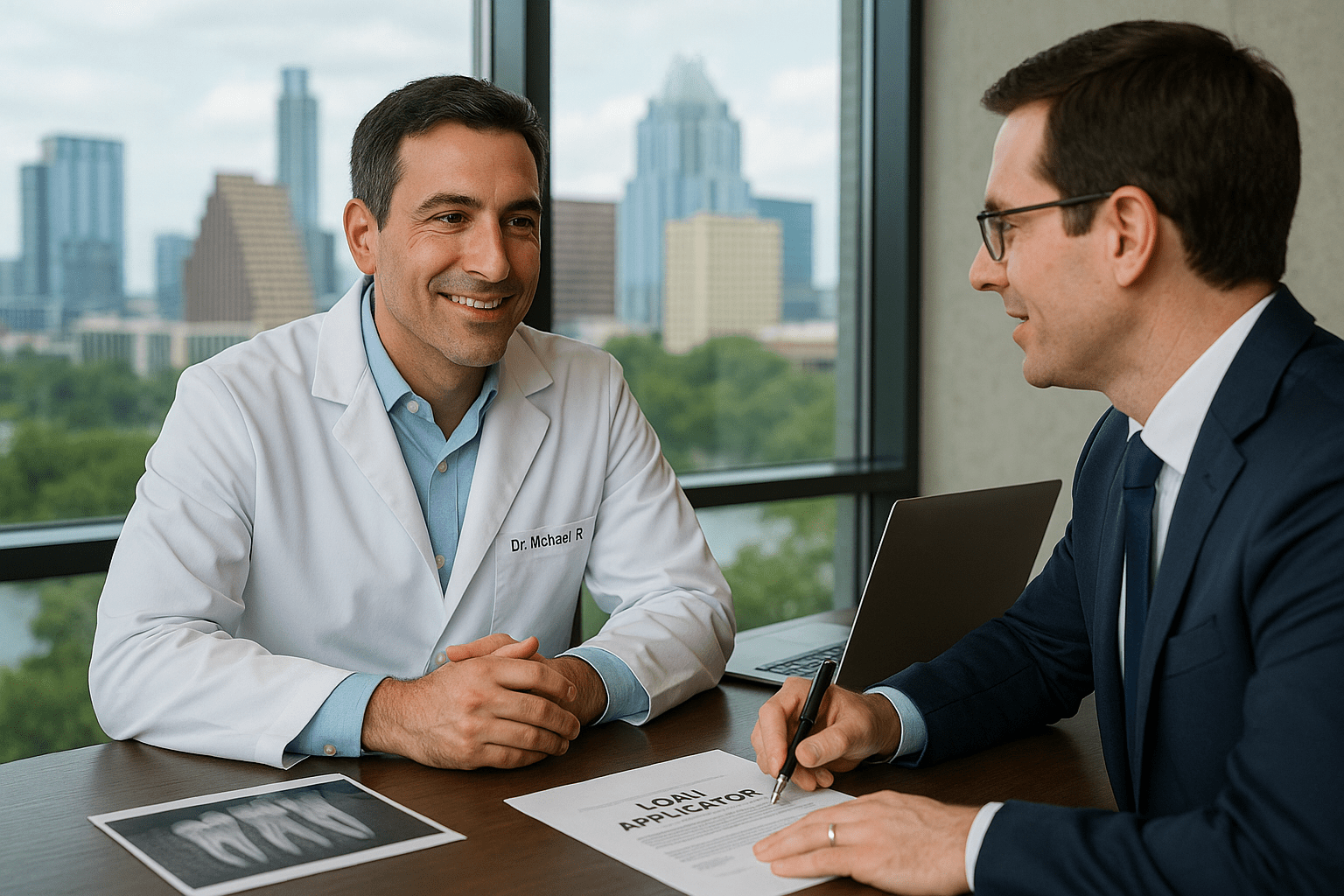

Dr. Michael R., a 44-year-old dentist based in Austin, Texas, had built substantial equity in his primary residence over 12 years of homeownership. His thriving dental practice generated strong income, and he maintained excellent credit. After years of steady growth, Michael identified an opportunity to expand his practice by acquiring state-of-the-art equipment and renovating a larger office space. The expansion would increase patient capacity and position his practice for long-term growth—but he needed substantial capital quickly.

Michael had adequate business savings, but using those funds would deplete his practice’s operating reserves below comfortable levels. He’d built substantial home equity and wanted to tap that wealth to fund the expansion without disrupting his existing favorable mortgage or depleting business liquidity. The challenge was finding a financing solution that provided a predictable lump sum with fixed payments while preserving the low rate on his existing home loan.

Facing similar challenges? Schedule a call to explore your options.

Dr. Michael R., a 44-year-old dentist based in Austin, Texas, had built substantial equity in his primary residence over 12 years of homeownership. His thriving dental practice generated strong income, and he maintained excellent credit. After years of steady growth, Michael identified an opportunity to expand his practice by acquiring state-of-the-art equipment and renovating a larger office space. The expansion would increase patient capacity and position his practice for long-term growth—but he needed substantial capital quickly.

Michael had adequate business savings, but using those funds would deplete his practice’s operating reserves below comfortable levels. He’d built substantial home equity and wanted to tap that wealth to fund the expansion without disrupting his existing favorable mortgage or depleting business liquidity. The challenge was finding a financing solution that provided a predictable lump sum with fixed payments while preserving the low rate on his existing home loan.

Facing similar challenges? Schedule a call to explore your options.

Michael initially explored traditional business loans for his practice expansion. Lenders offered acceptable terms, but the rates were significantly higher than mortgage-based financing, and they required substantial business assets as collateral. He also considered cash-out refinancing his home but immediately recognized the problem: replacing his existing low-rate mortgage with current market rates would substantially increase his monthly housing payment.

“Business loan rates were substantially higher than mortgage rates, even though I had excellent credit and a profitable practice,” Michael explained. “Using business loans would work, but the carrying costs would be significantly higher than home equity financing. I wanted to leverage my personal real estate equity to fund business growth at better rates.”

Michael’s existing mortgage carried a favorable rate well below current market levels—a rate he secured nearly a decade earlier. Cash-out refinancing would replace that entire loan with a new mortgage at substantially higher current rates, dramatically increasing his monthly housing payment just to access capital for business use.

Unlike revolving credit lines with variable rates, Michael needed predictable fixed monthly payments he could build into his practice’s long-term financial projections. He was making a substantial capital investment in equipment and office improvements that would generate returns over many years—he wanted financing that matched that timeline with stable, budgetable payments.

“I run detailed financial projections for my practice,” Michael said. “Variable-rate financing introduces uncertainty into those projections. I needed a lump sum with fixed monthly payments I could count on—something that wouldn’t fluctuate with interest rate changes over time. And I wanted to access my home equity without losing my favorable existing mortgage rate.”

Experiencing similar challenges? Schedule a call to discuss alternative qualification methods.

Michael discovered home equity loan programs while researching second mortgage options with his financial advisor. His advisor explained the key difference: unlike HELOCs that provide revolving credit access, home equity loans provide a one-time lump sum with fixed interest rates and predictable monthly payments over a set repayment term.

During his consultation with a home equity loan specialist, Michael learned how these loans function as second mortgages providing lump-sum funding—similar to a traditional mortgage but in second lien position behind his existing first mortgage. Unlike revolving HELOCs with variable rates, home equity loans provide fixed-rate financing with consistent monthly payments.

The loan advisor explained that home equity loans work well when borrowers need a specific amount for a defined purpose—whether business expansion, major home improvements, debt consolidation, or large one-time expenses. The fixed-rate structure provides payment certainty, and the second lien position preserves the existing first mortgage.

“That conversation clarified the perfect solution,” Michael explained. “The home equity loan gave me access to substantial capital as a lump sum with fixed payments I could budget precisely. My existing mortgage stayed in place at its favorable rate, and I could fund my practice expansion at mortgage rates rather than higher business loan rates. It checked every box.”

The home equity loan lender evaluated Michael’s combined loan-to-value ratio—his first mortgage balance plus the requested home equity loan amount against his home’s current appraised value. With substantial equity, excellent credit, strong income, and minimal existing debt, Michael qualified easily. This wasn’t just solving a capital access problem—it was enabling smart financial strategy by using his lowest-cost capital source to fund his highest-return investment opportunity.

Michael worked with his loan advisor to assemble documentation for his home equity loan application. The process resembled his original mortgage experience but moved efficiently since the lender was taking a second lien position rather than replacing existing financing.

Documentation provided:

The approval process:

The home equity loan lender approved a substantial lump-sum loan based on Michael’s available equity, credit profile, and income capacity. The structure included a fixed interest rate and predictable monthly payments over an extended repayment term. Michael received the full loan proceeds at closing, immediately available for his practice expansion project.

Exploring refinance options? Submit a refinance inquiry to compare your options.

Michael closed on his home equity loan in less than four weeks after submitting his application. He immediately deployed the capital for his practice expansion, purchasing advanced dental equipment and completing office renovations that doubled his operatory capacity.

Final home equity loan outcome:

Cash-out refinance vs. home equity loan financing:

Michael’s practice expansion generated substantial return on investment through increased patient capacity and the ability to offer advanced procedures previously unavailable with his old equipment. The fixed monthly home equity loan payment fit comfortably within his practice budget, and the favorable rate made the financing cost-effective compared to alternative capital sources.

“Without the home equity loan, I would have either accepted substantially higher business loan rates or depleted my practice operating reserves—neither option was ideal,” Michael explained. “The home equity loan gave me the perfect solution: low-rate fixed financing that preserved my favorable existing mortgage and kept my practice liquidity intact. Now my expanded capacity is generating excellent returns, and the loan payment is easily covered by the incremental revenue.”

Michael views this expansion as a strategic investment in his practice’s long-term value and his family’s financial security. The increased capacity and advanced equipment position his practice for continued growth over the coming decade. Beyond this expansion, Michael is considering future investment opportunities including purchasing the building that houses his practice or acquiring additional practice locations.

“This isn’t just about expanding one office,” Michael added. “It’s about building substantial wealth through strategic investments in my business. The home equity loan unlocked growth capital at favorable rates without disrupting my personal finances. As I evaluate future opportunities—whether real estate, additional locations, or other investments—I know I can leverage my equity strategically while maintaining the favorable financing I’ve already secured.”

When Michael is ready for his next strategic investment, he might tap additional equity through another Home Equity Loan for lump-sum funding or explore a HELOC for more flexible access if he prefers revolving credit. He’s also considering commercial real estate investment, using home equity strategically to fund down payments while building long-term wealth through property ownership.

Ready to get started? Get approved or schedule a call to discuss your situation.

While Dr. Michael used a home equity loan to fund practice expansion, home equity loan financing works for multiple scenarios:

Have questions about qualifying with home equity loan programs? Schedule a call with a loan advisor today.

If a home equity loan isn’t the perfect fit, consider these alternatives:

Explore all loan programs to find your best option.

Learn more about this loan program:

Similar success stories:

External authoritative resources:

Ready to get started?

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and contractors in your area.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get the latest insights and mortgage case studies in your inbox.