Veterans and service members with existing VA loans often miss opportunities to reduce their mortgage costs through the VA’s streamlined refinance program. The Interest Rate Reduction Refinance Loan (IRRRL)—commonly called the VA Streamline Refinance—provides a simplified path to lower interest expenses without the extensive documentation, appraisal requirements, or rigorous qualification processes typical of standard refinancing. This specialized program exists specifically to help military families reduce their VA loan costs quickly and efficiently. This comprehensive guide reveals how eligible VA borrowers can leverage the IRRRL to reduce monthly obligations, switch from adjustable to fixed structures, and navigate the streamlined process while understanding when standard VA refinancing might serve you better.

Key details you’ll discover:

Ready to explore your options? Schedule a call with a loan advisor.

The VA Interest Rate Reduction Refinance Loan (IRRRL) is a streamlined refinancing program designed exclusively for veterans and service members with existing VA loans. Unlike standard refinances requiring extensive documentation, appraisals, and full underwriting reviews, the IRRRL simplifies the process to help military families reduce interest costs quickly and efficiently.

The IRRRL serves one primary purpose: lowering your interest expense on an existing VA loan. Whether you want to reduce your monthly obligations, switch from an adjustable structure to a fixed one, or simply take advantage of improved market conditions, the IRRRL provides the fastest path to accomplish these goals.

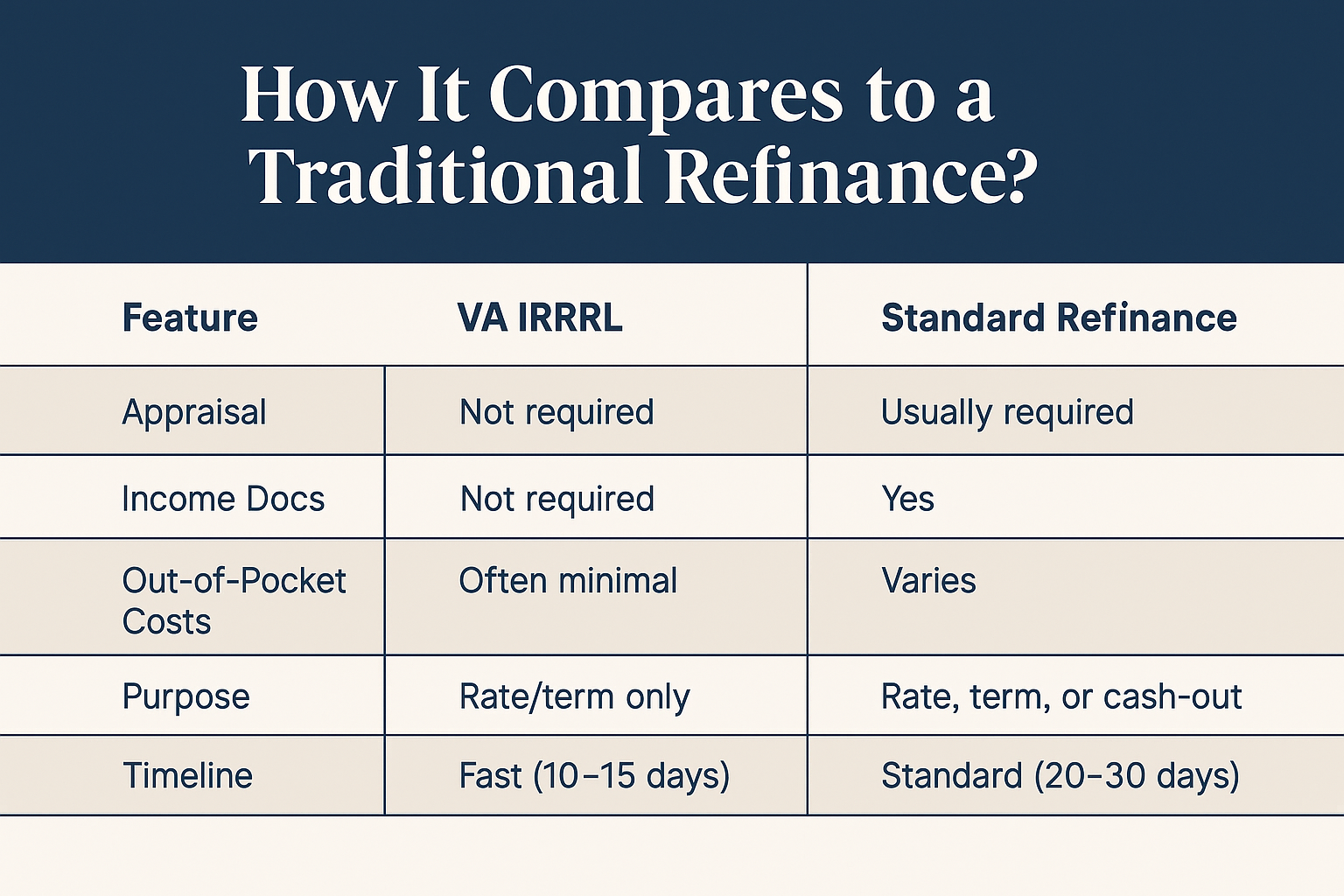

How does the IRRRL differ from standard VA refinancing?

The IRRRL offers distinct processing advantages:

However, the IRRRL comes with specific restrictions:

These streamlined features make the IRRRL ideal when your sole objective is reducing costs on your existing VA loan without modifying borrowers or accessing equity.

See how other veterans have successfully used IRRRL refinancing:

IRRRL eligibility centers on having an existing VA loan with satisfactory payment history. The streamlined nature means fewer qualification hurdles than standard refinancing, but specific requirements still apply.

Must you currently have a VA loan to use an IRRRL?

Yes. The IRRRL exclusively refinances existing VA loans. You cannot use this program to refinance:

If you currently have a non-VA loan and want VA financing, you need a standard VA refinance instead. The standard VA refinance offers more flexibility including the ability to:

View standard VA refinance case studies to understand when this option makes more sense than an IRRRL.

What payment history must you demonstrate for IRRRL approval?

Lenders require satisfactory payment performance on your existing VA loan:

Minimum seasoning – At least six months of payments on your current VA loan before IRRRL eligibility

Recent payment history – No late payments (typically) in the past six months, though some lenders accept one 30-day late payment with explanation

Current status – Cannot be in default or foreclosure proceedings on your existing VA loan

Occupancy certification – Must certify that you previously occupied the property as your primary residence, even if you no longer live there

This payment requirement ensures the IRRRL program serves veterans managing their mortgages responsibly rather than those already struggling with existing obligations.

Does the IRRRL require full income and credit documentation?

The IRRRL significantly reduces documentation compared to standard refinancing:

Credit verification – Lenders typically pull credit reports but focus primarily on VA loan payment history rather than comprehensive credit analysis

Income documentation – Many IRRRLs process with limited or no income verification, especially when:

Employment verification – Streamlined or waived in many cases when payment history is strong

However, some circumstances trigger additional documentation:

The streamlined approach makes IRRRLs accessible even for veterans whose income or employment situations have changed since obtaining their original VA loan.

Calculate your IRRRL scenario:

What is the net tangible benefit requirement for IRRRLs?

The VA mandates that IRRRLs provide clear financial advantage to borrowers. You cannot refinance simply because you want to—you must demonstrate one of these net tangible benefits:

The most common benefit: lowering your interest percentage to reduce either your monthly payment or your total interest paid over the life of the loan. The new structure must be lower than your current one (with specific exceptions for refinancing adjustable structures).

If you currently have an adjustable structure, you can refinance to a fixed one even if it doesn’t immediately reduce your payment. This provides:

You can refinance to a shorter period to build equity faster and reduce total interest paid, even if your monthly payment increases. This strategy works when:

The VA recognizes that some veterans prefer accelerated equity building even with higher monthly obligations, accepting this as a valid net tangible benefit.

How quickly must you recoup refinancing costs?

Lenders must demonstrate that you’ll recoup closing costs through reduced monthly payments within a reasonable timeframe:

Standard recoupment calculation – Divide total closing costs by monthly payment reduction to determine months until break-even

Acceptable timeframes – The VA doesn’t mandate specific maximum recoupment periods, but most lenders prefer periods under 36 months

Exclusions from calculation – Certain costs don’t count toward recoupment including:

Understanding recoupment helps determine whether refinancing makes financial sense based on how long you plan to keep the property and maintain the new loan.

What funding fees apply to IRRRL refinances?

IRRRLs include funding fees that help sustain the VA loan program for future veterans. However, IRRRL funding fees are lower than fees for purchase loans or cash-out refinances:

IRRRL funding fees vary based on:

First-time vs. subsequent use – Lower fees apply for your first IRRRL, while subsequent IRRRLs carry slightly higher fees

Regular military vs. Reserves/Guard – Reserve and National Guard members typically pay modestly higher fees

Financing method – You can either:

Most veterans choose to finance funding fees into their new loan amounts rather than paying at closing. This approach minimizes upfront cash requirements while marginally increasing the loan balance and monthly payment.

Who qualifies for IRRRL funding fee waivers?

The same exemptions that apply to other VA loans apply to IRRRLs:

Veterans with funding fee exemptions save substantially on each IRRRL refinance, making it easier to take advantage of improved market conditions multiple times without accumulating fees.

Check the VA IRRRL funding fee chart for current fee amounts based on your specific circumstances.

How does the IRRRL application and approval process work?

The streamlined IRRRL process typically completes in 20-30 days from application to closing:

Contact a VA-approved lender and provide:

Unlike standard refinances, you typically don’t need:

Your lender verifies:

This review typically completes within 5-10 business days, much faster than standard refinance underwriting.

Once your IRRRL qualifies, you’ll:

Market conditions affect available structures, so timing your rate lock strategically can maximize your savings.

Your lender coordinates:

What happens to your current loan during IRRRL processing?

Continue making your regular monthly payments on your existing VA loan until your IRRRL closes. Your current lender receives payoff proceeds at closing, and your new loan replaces the old one. Any payments made after your closing are typically refunded or applied to your new loan depending on timing.

At closing, you’ll:

The new loan typically funds within 1-2 business days after closing. Your first payment on the new loan usually isn’t due for 30-45 days after closing, giving you a brief payment holiday between your final payment on the old loan and your first payment on the new one.

Ready to discuss your IRRRL scenario? Submit a refinance inquiry to explore whether this makes sense for you.

Yes. IRRRLs require only that you previously occupied the property as your primary residence when you obtained the original VA loan. You can refinance with an IRRRL even if you:

You must certify at closing that you previously occupied the property, but current occupancy isn’t required. This flexibility helps military families who relocate frequently manage mortgages on properties they’ve converted to rentals.

Is there a limit on how many IRRRLs you can complete?

No maximum limit exists on IRRRL usage. You can refinance your VA loan multiple times using the IRRRL program, provided you:

Veterans commonly use IRRRLs multiple times as market conditions improve or their financial circumstances change. However, consider diminishing returns—each refinance incurs closing costs and funding fees, so ensure the benefits justify these expenses.

No. The IRRRL’s streamlined nature eliminates appraisal requirements in most circumstances. This advantage provides:

Appraisal waivers represent one of the IRRRL’s most valuable features, especially in markets where property values have decreased since your original purchase. You can refinance to reduce costs regardless of current property value, as long as your existing loan balance doesn’t exceed allowable refinancing limits.

Limited cash back is possible, but IRRRLs aren’t designed for substantial equity access. Typical restrictions include:

When you need substantial cash from your equity:

Use a standard VA cash-out refinance instead of an IRRRL. Cash-out refinances allow you to:

View VA cash-out refinance case studies to understand this alternative approach when equity access is your primary goal.

No. IRRRLs require the same borrowers on the new loan as the original. You cannot use an IRRRL to:

When you need to modify borrowers:

Use a standard VA refinance that allows complete flexibility to:

Standard VA refinances require full documentation but provide the flexibility to modify your borrower structure as life circumstances change.

View standard VA refinance case studies showing scenarios where borrower changes made standard refinancing the better choice.

Does refinancing with an IRRRL consume additional VA entitlement?

No. IRRRLs don’t require new entitlement because you’re refinancing an existing VA loan, not taking out a new one. Your entitlement remains the same—the existing loan’s guarantee simply transfers to the new IRRRL.

This means you can:

If you have remaining entitlement beyond what’s securing your current VA loan, that excess remains available for purchasing additional properties or taking out new VA loans.

When should you use an IRRRL versus a standard VA refinance?

Understanding the key differences helps you select the right refinancing approach:

You want the fastest, simplest path to reduce costs on your existing VA loan and:

The IRRRL’s streamlined processing makes it ideal when your only goal is cost reduction without any loan restructuring needs.

You need more flexibility than the IRRRL provides, including situations where you:

Currently have a non-VA loan – FHA, conventional, or USDA mortgages require standard VA refinancing to convert to VA financing

Need to modify borrowers – Marriage, divorce, inheritance, or other life changes requiring addition or removal of borrowers

Want substantial cash out – Need to access equity beyond the minimal amounts IRRRLs allow (typically up to a certain amount)

Need to remove private mortgage insurance – Currently pay PMI on a conventional loan and want to eliminate it through VA refinancing

Want property value considered – Have substantially increased equity that strengthens your qualification

Standard VA refinances require:

However, they provide flexibility worth the additional documentation when your needs extend beyond simple interest reduction.

Scenario 1: Pure cost reduction

Scenario 2: Divorce situation

Scenario 3: Converting from FHA

Scenario 4: Need cash for improvements

Use these comparison tools to evaluate your options:

What costs should you expect when completing an IRRRL?

IRRRLs typically involve lower closing costs than standard refinances due to streamlined requirements:

Lender fees – Origination charges for processing and underwriting your refinance

Title fees – Title search and insurance protecting the lender’s interest (though typically lower than purchase title work)

Recording fees – Government charges for recording your new mortgage

Credit report – Cost of pulling your credit history

Flood certification – Verification of flood zone status for the property

VA funding fee – One-time charge supporting the VA loan program (can be financed)

Items you typically DON’T pay with IRRRLs:

Most IRRRL borrowers finance closing costs and funding fees into their new loan amount rather than paying them at closing. This approach:

Calculate whether the marginally higher monthly payment from financing costs still provides net benefit compared to your current loan.

Can you complete an IRRRL without paying closing costs?

Some lenders offer structures where closing costs are covered through slightly higher interest structures rather than upfront fees. This approach works when:

Evaluate total costs over your expected holding period to determine whether no-closing-cost structures provide better value than traditional approaches with upfront costs but lower structures.

Yes, provided you previously occupied the property as your primary residence when you obtained the original VA loan. The IRRRL’s occupancy requirement focuses on previous occupancy, not current use.

This flexibility particularly benefits military families who:

You must certify at closing that you previously occupied the property, but current rental use doesn’t disqualify you from IRRRL refinancing.

How do escrow accounts transfer when refinancing?

Your existing escrow account typically refunds to you within 20-30 days after your IRRRL closes. Simultaneously, your new lender establishes a new escrow account for property taxes and insurance on the refinanced loan.

This transition creates temporary overlap where:

Plan for this timing when budgeting your refinance. The refund from your old escrow eventually reimburses the new escrow deposits, but there’s typically a delay between collecting new escrow and receiving the old refund.

Is it possible to modify your remaining period when refinancing?

Yes. IRRRLs allow you to select different durations than your original loan, enabling you to:

Extend your period to:

Shorten your period to:

When changing durations, ensure you still meet the net tangible benefit requirement. Extending your period while lowering your structure easily demonstrates benefit through reduced monthly obligations. Shortening your period requires showing benefit through total interest savings or other valid advantages.

Can you include energy improvements in your IRRRL?

The VA allows energy-efficient improvements in IRRRLs through the Energy Efficient Mortgage (EEM) program. This option lets you:

Energy improvements must:

This combination approach helps veterans reduce both mortgage costs and ongoing utility expenses simultaneously.

What paperwork do you need for IRRRL applications?

The streamlined IRRRL requires minimal documentation compared to standard refinances:

Always required:

Sometimes required depending on circumstances:

Rarely or never required:

This minimal documentation makes IRRRLs accessible even for veterans whose income or employment circumstances have changed since obtaining their original loans.

Refinancing during active Chapter 13 bankruptcy presents challenges but isn’t impossible. Requirements typically include:

Most veterans wait until bankruptcy discharge before refinancing, as this eliminates complications and expands lender options. However, if refinancing during bankruptcy provides substantial benefits, work with both your bankruptcy attorney and lender to navigate the approval process.

Why do IRRRL applications get rejected?

Despite streamlined processing, IRRRLs can still be denied for specific reasons:

Insufficient seasoning – Haven’t made six months of payments on current VA loan

Poor payment history – Recent late payments on existing VA loan without acceptable explanations

No net tangible benefit – Cannot demonstrate that refinancing reduces costs or improves loan structure

Unacceptable recoupment period – Takes too long to recover closing costs through savings

Current loan isn’t VA-backed – The IRRRL exclusively refinances existing VA loans

Property title issues – Liens, judgments, or ownership problems discovered during title review

Inadequate credit standing – Even with streamlined review, seriously compromised credit may prevent approval

Occupancy certification problems – Cannot verify previous primary residence occupancy

Excessive existing debt – When combined with housing expenses, monthly obligations exceed acceptable thresholds

Address these potential issues before applying to increase approval probability and reduce processing delays.

Explore all loan programs to understand your complete range of options.

What happens to your mortgage payments during IRRRL processing?

You don’t actually “skip” payments, but you often experience a payment gap due to refinancing timing:

If you made your regular payment shortly before closing, you might go 6-8 weeks without making a mortgage payment. This happens because:

This break provides brief cash flow relief but doesn’t represent forgiven obligations—you’re simply experiencing normal payment timing associated with refinancing.

What credit impact should you expect from IRRRL refinancing?

IRRRLs typically have minimal credit impact:

Short-term effects:

Long-term effects:

Most veterans see negligible lasting credit effects from IRRRLs. Any temporary score reduction typically recovers within a few months as you establish positive payment history on the new loan.

No. IRRRLs require satisfactory payment history on your existing VA loan. If you’re currently behind on payments or in default:

First priority: Bring your loan current through:

Then explore refinancing once you’ve:

If you’re struggling with your current VA loan payments, contact your lender immediately to discuss options like:

Address payment difficulties promptly rather than letting them escalate to foreclosure.

How does refinancing affect your mortgage timeline?

Yes, an IRRRL creates a new loan with a new start date. This affects your mortgage in several ways:

Amortization restarts – If you refinance to the same duration as your original loan, you’ll be paying for a longer total period:

Equity building pace changes – Early loan years allocate more toward interest than principal. Restarting resets this amortization curve, potentially slowing equity accumulation temporarily.

Total interest considerations – Extending your timeline increases total interest paid even if your structure decreases. Calculate total costs over your entire holding period, not just monthly savings.

To avoid extending your overall mortgage timeline, choose a new period matching your remaining time on the original loan.

IRRRLs require certification that you previously occupied the property as your primary residence. Second homes or vacation properties that never served as your primary residence don’t qualify for IRRRL refinancing.

However, former primary residences converted to second homes or vacation properties after establishing occupancy may qualify, provided you:

The distinction matters: second homes you never occupied as primary residences don’t qualify, while former primary residences now used seasonally may qualify based on previous occupancy.

Does refinancing affect mortgage insurance requirements?

VA loans don’t require private mortgage insurance regardless of your equity level—this benefit applies to both your original VA loan and any IRRRL refinances.

If you previously refinanced from a conventional or FHA loan to VA financing, you already eliminated mortgage insurance when you first obtained your VA loan. The IRRRL simply refinances your existing VA loan without any mortgage insurance considerations.

This represents one of the VA loan program’s most valuable features: no mortgage insurance regardless of your equity position, saving hundreds monthly compared to conventional financing with limited equity.

What is the minimum waiting period for IRRRL eligibility?

You must wait at least 210 days from the first payment due date on your current VA loan AND make at least six monthly payments before IRRRL eligibility. Both requirements must be satisfied:

Minimum 210 days – Calculated from your first payment due date, not your closing date

Minimum 6 payments – Actual monthly payments made, not just time elapsed

Example timeline:

This seasoning requirement ensures the IRRRL program serves veterans managing their loans responsibly rather than those constantly churning refinances.

Does the IRRRL allow conversion from adjustable structures to fixed ones?

Yes. Converting from an adjustable structure to a fixed one represents a valid net tangible benefit even if it doesn’t immediately reduce your payment. The VA recognizes that predictability and protection from future increases provide valuable benefits justifying IRRRL refinancing.

This option particularly benefits veterans who:

When converting from adjustable to fixed structures, demonstrate net tangible benefit by showing:

This conversion strategy provides peace of mind and financial stability even if your immediate payment doesn’t decrease.

Ready to get started? Apply now or schedule a call to discuss your situation.

If a VA IRRRL isn’t the right fit, consider these refinancing alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which refinancing approach is right for you? Take our discovery quiz to find your path.

VA IRRRL Program Overview and Requirements – Comprehensive Department of Veterans Affairs resource explaining IRRRL program benefits, eligibility requirements, and streamlined processing features for existing VA loan holders.

VA Net Tangible Benefit Standards for IRRRLs – Official VA guidance on net tangible benefit requirements ensuring refinancing provides clear financial advantages to veteran borrowers.

VA IRRRL Funding Fee Chart – Current funding fee schedules for IRRRL refinances showing amounts based on service type and whether this is your first or subsequent IRRRL.

VA Home Loans Main Page – Central hub for all VA loan programs including purchase loans, refinances, and specialized programs serving military families.

VA Loan Entitlement Information – Detailed guidance on VA loan entitlement including how refinancing affects your available benefits and restoration processes.

Consumer Financial Protection Bureau Refinancing Guide – Federal consumer protection agency providing unbiased information about refinancing considerations, cost comparisons, and borrower rights.

HUD Housing Counseling Services – Directory of HUD-approved housing counselors offering free or low-cost assistance with refinancing questions, financial planning, and decision-making support.

Military OneSource Financial Counseling – Department of Defense program offering free financial counseling and education specifically for military families evaluating refinancing options and managing mortgages.

Defense Finance and Accounting Service – Official military pay and benefits information helping service members understand income documentation requirements for refinancing applications.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.