Real estate investors evaluating properties based on cash flow potential often find traditional income documentation irrelevant to their investment strategy. DSCR loans qualify you based solely on the property’s rental income potential rather than personal employment or tax returns. This investment-focused approach streamlines qualification for rental properties, vacation homes, and portfolio expansion when the property’s income-generating capacity matters more than your W-2.

Ready to explore your options? Schedule a call with a loan advisor.

A DSCR loan represents an investment property financing approach that evaluates the property’s income-generating capacity rather than the borrower’s personal income. The acronym DSCR stands for Debt Service Coverage Ratio—a calculation comparing the property’s rental income to its total housing expenses.

How does the DSCR calculation work? Lenders divide the property’s monthly rental income by the total monthly housing expense (principal, interest, taxes, insurance, and HOA fees if applicable). A DSCR of 1.0 means the rental income exactly covers the expenses. A DSCR above 1.0 indicates positive cash flow, while below 1.0 shows the property requires subsidizing from other sources.

Most DSCR loan programs require minimum ratios ranging from 0.75 to 1.25 depending on the lender, property type, and borrower profile. A property generating sufficient rental income to achieve the minimum DSCR qualifies for financing without analyzing the investor’s personal income, employment, or tax returns.

This approach revolutionizes real estate investment financing by recognizing that rental property cash flow—not personal income—determines the investor’s ability to manage mortgage obligations. For investors with multiple properties or tax-efficient business structures showing minimal personal income, a DSCR loan provides qualification paths impossible through traditional financing.

Several investor profiles find exceptional value in a DSCR loan structure. These programs serve real estate investors whose portfolio strategies don’t align with traditional income-based qualification methods.

Experienced real estate investors with multiple rental properties represent ideal candidates for a DSCR loan. Traditional mortgages struggle when investors own numerous properties because each mortgage obligation increases debt-to-income ratios, eventually preventing further acquisitions. A DSCR loan eliminates this constraint by ignoring personal debt-to-income calculations entirely.

Self-employed investors and business owners who strategically minimize taxable income through legitimate business deductions find a DSCR loan particularly valuable. Your tax returns might show minimal income despite strong cash flow and substantial assets. Since a DSCR loan doesn’t examine personal income, your tax strategies don’t sabotage your investment property financing.

Foreign national investors purchasing U.S. rental properties often lack the employment documentation, tax returns, and credit history that traditional programs require. A DSCR loan focuses on the property’s rental potential rather than extensive personal documentation, making it accessible for international investors.

Retirees building rental portfolios may have limited W-2 income but substantial assets and investment experience. A DSCR loan allows acquiring rental properties based on rental income potential rather than retirement income that might not meet traditional qualification thresholds.

New investors acquiring first rental properties can use a DSCR loan when the investment property generates sufficient rental income. While some DSCR programs prefer experienced investors, many accommodate first-time rental property owners when the property’s fundamentals support approval.

Explore all loan programs to understand your full range of options.

Understanding the specific qualification criteria helps you assess whether a DSCR loan fits your investment strategy. While requirements vary by lender and program, certain standards commonly apply across most DSCR offerings.

DSCR ratio thresholds – Most programs require minimum debt service coverage ratios between 0.75 and 1.25. Properties with DSCR below 1.0 (where rental income doesn’t fully cover expenses) may still qualify but typically require larger equity contributions, stronger credit, or higher interest rates to compensate for the negative cash flow.

Credit score minimums – DSCR loan programs typically require credit scores of 620-680 minimum, with optimal programs available at 700+. Your credit history demonstrates financial responsibility even though lenders don’t analyze your income or employment.

Equity contribution expectations – Most DSCR loan programs require 20-25% equity contributions for single-family properties, with higher requirements (25-30%) for multi-unit buildings. The equity investment demonstrates commitment and provides lender security.

Reserve requirements – Lenders typically require substantial liquid reserves, often 6-12 months of the property’s total housing expenses. These reserves demonstrate your capacity to manage the property through vacancy periods, repairs, or market fluctuations. Multiple property owners may need reserves calculated across their entire portfolio.

Property rental income documentation – For properties with existing tenants, lenders use current lease agreements to establish rental income. For vacant properties or purchases, appraisers provide fair market rent estimates based on comparable rental properties in the area.

No income documentation required – The defining feature of a DSCR loan is the absence of personal income verification. No tax returns, no W-2s, no pay stubs, no employment verification letters. Your personal income remains irrelevant to qualification.

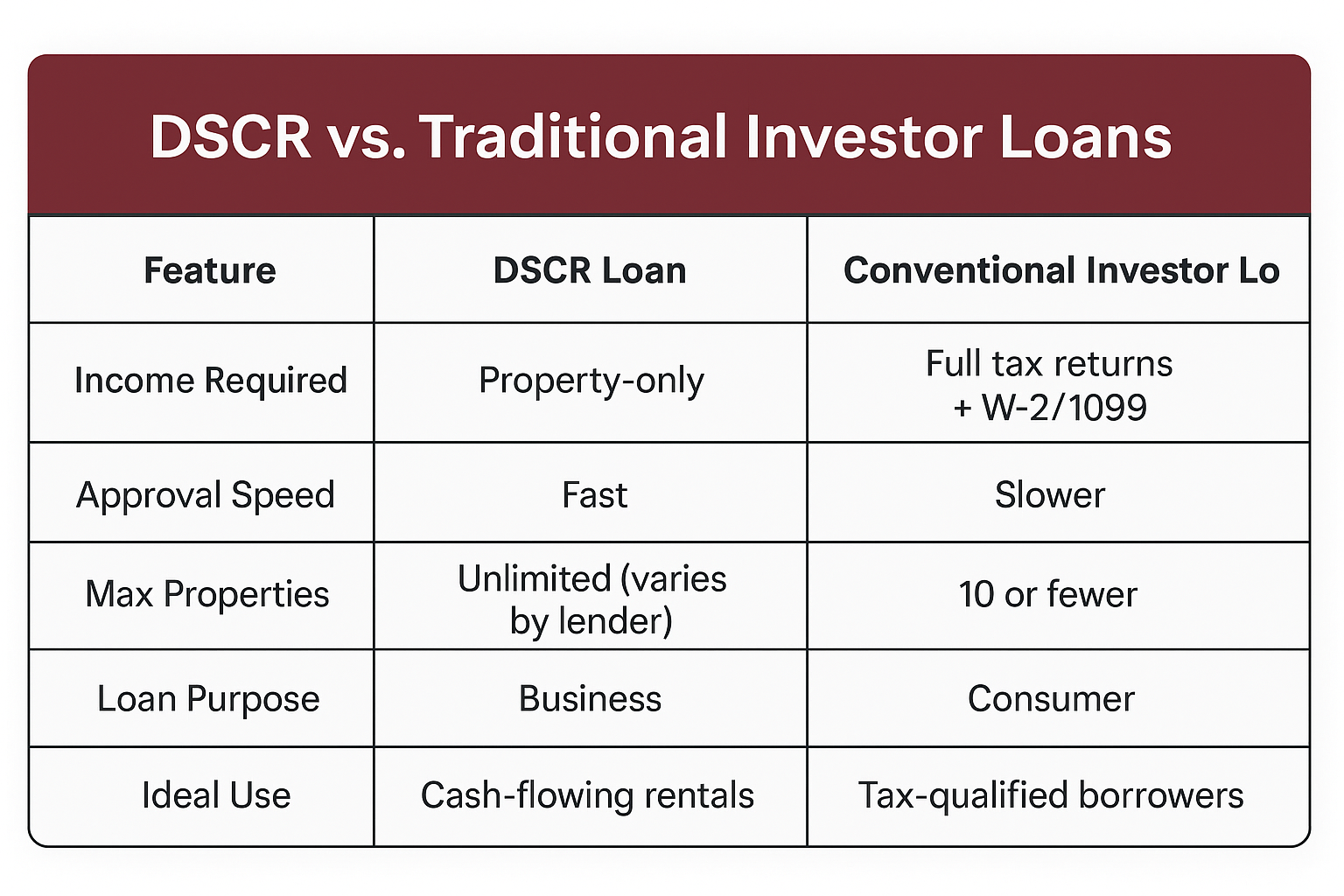

The fundamental distinction lies in the qualification methodology and documentation requirements. Traditional investment property mortgages analyze your personal income and debt obligations while a DSCR loan focuses exclusively on the property’s rental income potential.

Traditional investment property financing:

DSCR loan qualification approach:

Why does personal income not matter for a DSCR loan? The underwriting philosophy recognizes that rental properties should support themselves through tenant income. If the property generates sufficient rent to cover its obligations, the investor’s personal income becomes irrelevant. This approach aligns with how sophisticated real estate investors actually manage portfolios—evaluating each property as an independent business entity.

Ready to discuss your purchase scenario? Submit a purchase inquiry to explore your options.

A DSCR loan program accommodates various investment property categories. Understanding eligibility across different property types helps you plan your real estate investment strategy.

Eligible investment property types:

Can you use a DSCR loan for fix-and-flip properties? Traditional DSCR loan programs focus on stabilized rental properties rather than short-term renovation projects. However, some specialized programs accommodate light renovation scenarios when the property will generate rental income after improvements. Extensive rehabs typically require alternative financing approaches.

What about vacation rentals or short-term rentals? Many DSCR loan programs now accommodate short-term rental properties including Airbnb, VRBO, or other vacation rental strategies. These programs use projected short-term rental income based on market analysis, comparable properties, and historical performance data rather than traditional long-term lease documentation.

Are there property location restrictions? DSCR loan programs generally work in all 50 states, though some lenders focus on specific markets or regions. Urban, suburban, and even some rural investment properties qualify when they demonstrate rental income potential. Properties in declining markets or economically challenged areas may face additional scrutiny.

What about property condition requirements? Most DSCR loan programs require properties in good condition suitable for immediate rental. Properties needing major repairs, significant safety issues, or system replacements may need renovation financing or alternative structures before qualifying for standard DSCR programs.

See how other real estate investors have successfully used DSCR financing:

Understanding rental income verification and calculation helps you evaluate whether specific properties meet DSCR requirements. The income determination process varies based on whether the property currently has tenants or sits vacant.

For properties with existing tenants:

For vacant properties or purchases:

What if you’re purchasing a property to convert to rental? Properties currently owner-occupied but destined for rental conversion use appraiser market rent estimates. The current owner’s occupancy doesn’t affect rental income potential. Lenders evaluate what tenants would pay in the current market regardless of current usage.

Do lenders account for vacancy rates? Most DSCR loan calculations use gross rental income without vacancy deductions. However, some conservative programs apply vacancy factors (typically 5-10%) when calculating the debt service coverage ratio. This approach provides additional safety margin for lenders.

Can you use Section 8 or subsidized rental income? Many DSCR loan programs accept government-subsidized rental income including Section 8 housing choice vouchers. These income sources often provide greater stability and consistency than market-rate rentals, potentially strengthening your application.

Calculate your DSCR loan scenarios:

Understanding the specific documentation requirements helps you prepare for a smooth application process. While a DSCR loan eliminates income documentation, specific property and financial verification remains necessary.

Required documentation typically includes:

Do you need to provide any personal financial information? While a DSCR loan doesn’t require income documentation, lenders need reserve verification. You’ll provide bank statements or investment account statements proving you have adequate liquid reserves to manage the property through challenges. The focus remains on assets rather than income.

What about entity ownership structures? Many real estate investors purchase properties through LLCs, corporations, or other legal entities for liability protection and tax purposes. DSCR loan programs accommodate entity ownership when you provide appropriate formation documents, operating agreements, and verification of your ownership stake or authority.

How do lenders verify property rental income? For existing tenants, lease agreements provide documentation. For vacant properties or purchases, the appraisal includes a rent schedule section where the appraiser analyzes comparable rental properties and establishes fair market rent estimates supporting the DSCR calculation.

Are tax returns ever required for a DSCR loan? Traditional DSCR loan programs specifically avoid tax return requirements—that’s the primary advantage. However, some hybrid programs might request tax returns for informational purposes without using them for income calculation. True DSCR programs require zero tax return documentation.

Yes, many DSCR loan programs accommodate properties with ratios below 1.0, meaning the rental income doesn’t fully cover the housing expenses. These scenarios require the investor to subsidize the property from other income sources, but qualification doesn’t require documenting those sources.

DSCR below 1.0 considerations:

Properties with strong appreciation potential, tenant quality, or below-market rents that will increase might justify accepting lower initial DSCR if the property’s fundamentals support long-term value.

Unlike traditional financing that caps portfolio growth through debt-to-income limitations, DSCR loan programs theoretically allow unlimited property acquisitions. Each property qualifies independently based on its own rental income rather than aggregating into personal debt ratios.

Practical portfolio growth limitations:

Experienced investors use DSCR loan financing to build extensive portfolios that would be impossible through traditional income-based qualification.

Standard DSCR loan programs focus on existing properties with established rental income or comparable properties proving market rent. New construction rentals face challenges because comparable rent analysis becomes difficult without similar completed properties.

Some specialized programs accommodate new construction investment properties when:

Most investors use construction financing or alternative programs during building phases, then refinance into DSCR loan programs once properties stabilize with tenants.

Multi-unit properties with 2-4 units aggregate total rental income for DSCR calculations. If your triplex has three units renting for different amounts, lenders sum the total monthly income and divide by the total monthly housing expense to determine the DSCR.

Multi-unit DSCR considerations:

Understanding the pricing framework helps you evaluate whether a DSCR loan provides competitive overall costs for your investment strategy. Interest rates represent only one component of the total return calculation.

What factors influence DSCR loan pricing? Several elements affect your specific rate:

Are DSCR loan rates higher than traditional investment property mortgages? DSCR loan pricing typically reflects a modest premium compared to conventional investment property financing due to the reduced documentation and specialized underwriting. However, many investors find the premium worthwhile given the qualification flexibility and portfolio scalability advantages.

Does a higher DSCR improve your rate? Yes, properties demonstrating stronger cash flow through higher debt service coverage ratios typically access more favorable pricing. A property with a 1.5 DSCR showing substantial positive cash flow receives better rates than a property barely meeting minimum 1.0 requirements.

Can you improve pricing through relationship lending? Some DSCR loan lenders offer portfolio pricing programs where rates improve as you finance multiple properties through their institution. Building relationships with specialized investment property lenders may provide pricing advantages over time.

The total investment return calculation should consider both financing costs and the ability to scale your portfolio efficiently. Many investors accept slightly higher rates on DSCR loan financing in exchange for the ability to acquire properties that would be impossible to finance through traditional programs.

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

Understanding the specific benefits helps you evaluate whether this financing approach aligns with your real estate investment strategy. A DSCR loan offers distinct advantages for investors building rental property portfolios.

Key advantages include:

No income documentation required – Eliminate the extensive tax return analysis, W-2 collection, employment verification, and income calculation that complicates traditional investment property financing. Your personal income remains completely irrelevant to qualification regardless of how it appears on tax returns.

Unlimited portfolio growth potential – Traditional mortgages limit portfolio size through debt-to-income ratio constraints. Each additional property increases your debt obligations, eventually preventing further acquisitions. A DSCR loan evaluates each property independently, enabling continuous portfolio expansion limited only by your capital and management capacity.

Accommodates tax-efficient investment strategies – Real estate investors legally minimize taxable income through depreciation, cost segregation, expense deductions, and strategic tax planning. These approaches devastate traditional mortgage qualification but don’t affect DSCR loan approval since personal income isn’t analyzed.

Faster closing timelines – Without complex income documentation, employment verification, and debt-to-income analysis, DSCR loan approvals often proceed more quickly than traditional financing. Many investors experience streamlined underwriting enabling competitive closing timelines for investment acquisitions.

Entity ownership flexibility – Purchase properties through LLCs, corporations, or other legal entities without the complications that traditional mortgages impose on entity lending. DSCR loan structures naturally accommodate entity ownership common in sophisticated real estate investing.

Foreign national accessibility – International investors purchasing U.S. rental properties face significant barriers with traditional financing requiring domestic employment, credit history, and tax documentation. A DSCR loan focuses on the property rather than extensive personal documentation, making it accessible for foreign nationals.

If a DSCR loan isn’t the right fit, consider these alternatives for investment property financing:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

Most DSCR loan programs use current market rent rather than projected future increases. Lenders focus on existing rental income or current market rents to ensure conservative, realistic calculations. Speculative rent growth doesn’t factor into approval decisions.

However, if you can demonstrate below-market rents that will increase upon lease renewal or tenant turnover, some lenders may consider using market rent rather than actual current rent. This requires clear documentation showing comparable properties commanding higher rents.

Standard DSCR loan programs focus on stabilized rental properties ready for immediate tenant occupancy. Properties requiring significant renovations before renting typically need alternative financing approaches.

Transitional property considerations:

DSCR loan assumption possibilities vary by lender and loan structure. Some portfolio lenders offering DSCR loan programs allow qualified buyers to assume existing financing with lender approval, potentially providing favorable terms for property acquisitions.

Seller financing combined with DSCR loan refinancing offers creative acquisition strategies. Purchase properties with seller financing, stabilize operations with tenants, then refinance into DSCR loan programs to return capital to the seller or fund additional investments.

Properties in areas lacking rental comparables face appraisal challenges for DSCR loan qualification. Appraisers need similar rental properties to establish credible market rent estimates supporting the debt service coverage ratio.

Limited comparable solutions:

Seasonal vacation rental properties or markets with significant seasonal rental variations require specialized DSCR analysis. Lenders typically annualize rental income to calculate monthly averages for debt service coverage ratio purposes.

Seasonal rental considerations:

DSCR loan programs focus exclusively on investment properties without owner occupancy. If you plan to occupy one unit of a multi-unit property, traditional financing programs better accommodate owner-occupied scenarios with rental income from non-occupied units.

However, if you purchase as an investment property using a DSCR loan and later decide to occupy a unit, that transition typically doesn’t violate loan terms since the original purpose was investment—though specific loan documents should be reviewed.

Rising interest rates increase the property’s monthly housing expense, reducing the debt service coverage ratio. Properties that previously qualified with comfortable DSCR margins may struggle to meet minimum requirements when rates increase significantly.

Rate environment strategies:

DSCR loan programs generally accommodate purchases from family members or related parties with appropriate documentation and legitimate transaction structures. Lenders want to ensure the transaction represents a true arm’s length sale rather than a disguised gift or inflated value.

Related party transaction requirements:

Yes, many real estate investors refinance conventional investment property mortgages into DSCR loan programs. This strategy makes sense when:

Refinancing into DSCR loan structures positions your portfolio for continued growth without personal income qualification constraints.

Properties where landlords pay utilities or other operating expenses require careful DSCR analysis. The rental income appears higher because it includes utility reimbursement, but actual net income is lower after deducting utility costs.

Utilities-included considerations:

Ready to get started? Apply now or schedule a call to discuss your situation.

Official Government Guidance:

CFPB Investment Property Mortgage Information – Consumer Financial Protection Bureau resource explaining investment property financing options, qualification differences from primary residence mortgages, and borrower protections for rental property lending.

IRS Rental Property Income Reporting Guidelines – Internal Revenue Service official guidance on rental real estate income reporting, expense deductions, depreciation rules, and tax obligations for investment property owners.

HUD Fair Housing Requirements for Landlords – Department of Housing and Urban Development resource on fair housing laws, tenant rights, landlord obligations, and legal compliance for rental property owners.

Industry Organizations:

Fannie Mae Investment Property Guidelines – Official Fannie Mae underwriting standards for investment property mortgages explaining traditional qualification methods that DSCR loans provide alternatives to for real estate investors.

National Association of Residential Property Managers – Industry organization providing education, resources, and standards for residential property management, supporting real estate investors in professional rental property operations.

Educational Resources:

IRS Passive Activity Loss Rules – Internal Revenue Service guidance on passive activity loss limitations, rental real estate exceptions, and tax treatment of rental property income and expenses affecting investor tax planning.

Federal Reserve Real Estate Investment Information – Federal Reserve reports and data on real estate investment trends, market conditions, and economic factors affecting rental property investment strategies.

Need local expertise? Get introduced to trusted partners including loan officers, property managers, and real estate investors in your area.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.