Buying a home in the United States doesn’t require citizenship or a Social Security number. ITIN loans open the door to homeownership for foreign nationals, non-permanent residents, and others who file taxes using an Individual Taxpayer Identification Number—proving that the American Dream is accessible to everyone who works hard and builds financial stability.

Ready to explore your options? Schedule a call with a loan advisor.

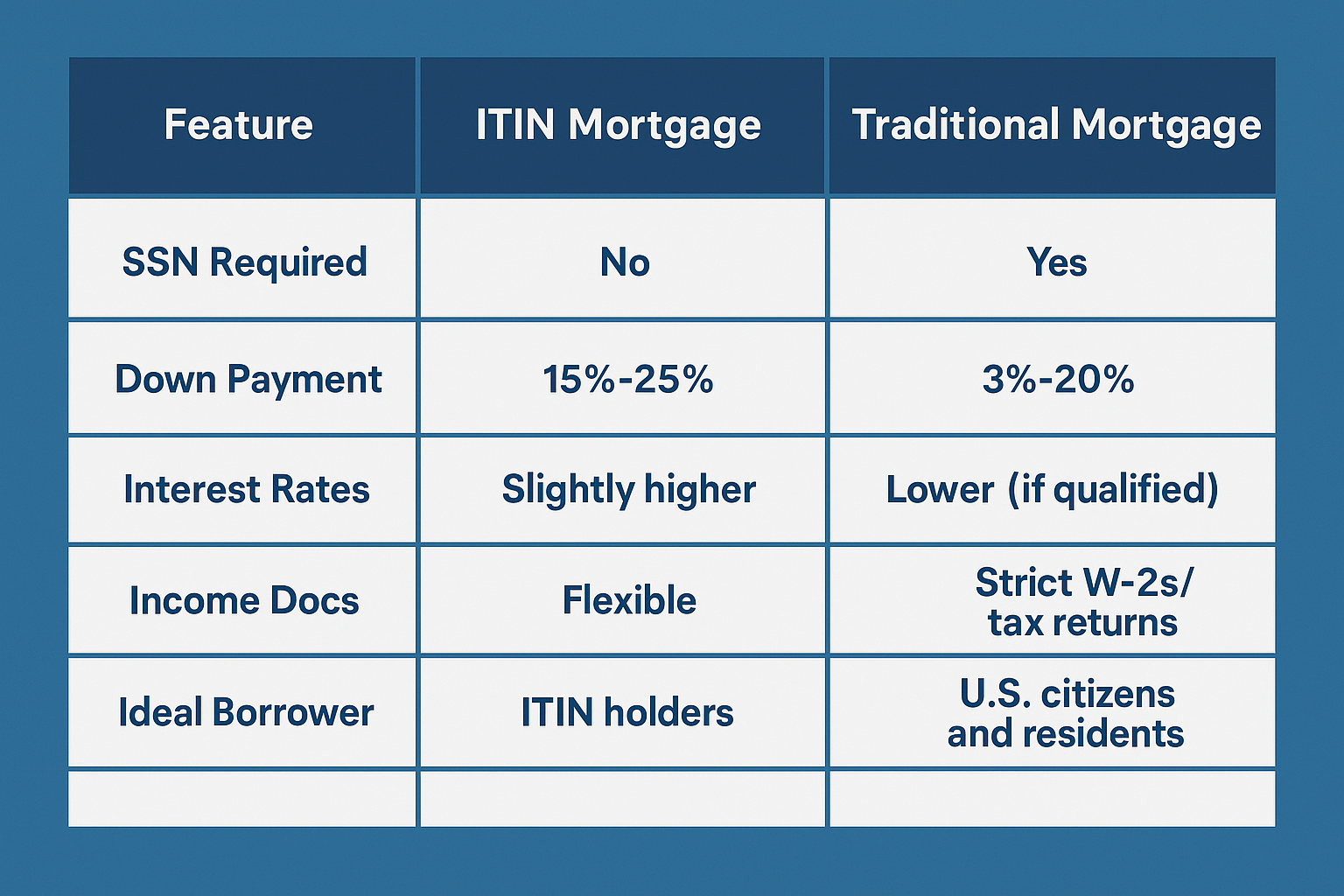

An ITIN loan is a specialized mortgage product designed for borrowers who have an Individual Taxpayer Identification Number instead of a Social Security number. ITINs are issued by the IRS to individuals who need to file U.S. taxes but aren’t eligible for Social Security numbers—including foreign nationals, non-permanent residents, visa holders, and others living and working in America.

Can you really buy a home without a Social Security number? Absolutely. ITIN loans recognize that many people contribute to the U.S. economy, pay taxes faithfully, and deserve the opportunity to build wealth through homeownership even without citizenship or permanent residency.

These loans function similarly to conventional mortgages in many ways—you make monthly payments covering principal and interest, build equity over time, and can eventually refinance or sell. The key difference lies in how lenders verify your identity, income, and creditworthiness without access to traditional Social Security-based systems.

Traditional mortgages rely heavily on Social Security numbers to:

ITIN loans use alternative verification methods that accomplish the same goals through different channels:

This manual approach requires more documentation and typically takes longer to process, but it ensures qualified borrowers can access financing despite lacking traditional identification numbers.

Why rent when you can own? For many ITIN borrowers, years of rent payments represent missed opportunities to build wealth through real estate equity.

Homeownership through ITIN financing allows you to:

Your primary residence becomes both your home and your most powerful wealth-building tool. Each monthly payment increases your ownership stake, and over time, your equity can fund education, business ventures, or future real estate investments.

The key is selecting properties in stable or appreciating neighborhoods where your investment will grow alongside your community ties.

ITIN loans aren’t limited to primary residences—many lenders offer investment property financing that lets you build a real estate portfolio:

Investment property advantages:

Investment properties require larger initial investments and more substantial reserve requirements, but they offer powerful wealth-building potential. Rental income from responsible tenants pays your mortgage while you benefit from appreciation and principal paydown.

Many successful ITIN borrowers start with their primary residence, then transition to investment properties once they’ve built equity and understand the local market.

Already own a home but stuck with unfavorable loan terms? ITIN refinancing can help you optimize your existing mortgage.

Refinancing scenarios that make sense:

Refinancing through ITIN programs sometimes offers better terms than your original loan, especially if you’ve built strong payment history, increased your income, or improved your financial profile since your initial purchase.

The key is calculating whether closing costs justify the long-term savings or benefits you’ll receive from the new loan terms.

Cash-out refinancing allows ITIN borrowers to tap into accumulated equity while maintaining homeownership:

Strategic uses for cash-out refinancing:

This strategy works best when you’ve built significant equity through appreciation, principal paydown, or both. By accessing a portion of your equity at mortgage interest rates rather than higher-cost alternatives, you can leverage your real estate investment to achieve other financial goals.

Remember that cash-out refinancing increases your loan balance, so ensure the purpose justifies the additional debt and that you can comfortably afford the new payment structure.

Considering a refinance? Submit a refinance inquiry to explore if this makes sense for your situation.

Want to minimize your housing costs while building wealth? Multi-family ITIN loans let you live in one unit while renting others to offset your mortgage payment.

House-hacking advantages for ITIN borrowers:

Two- to four-unit properties qualify for owner-occupied financing if you live in one unit, combining the benefits of homeownership with income generation. This strategy is particularly powerful for borrowers in expensive markets where purchasing a single-family home stretches affordability limits.

The rental income doesn’t just help with qualification—it fundamentally changes your housing economics, potentially reducing your net costs below what you’d pay renting a single-family home.

For many ITIN borrowers, traditional credit history is limited or non-existent. Your mortgage becomes your most powerful credit-building tool:

How mortgage payments build your financial profile:

While ITIN borrowers may not immediately benefit from traditional credit bureau reporting, maintaining perfect payment history creates documented evidence of creditworthiness. This becomes invaluable when you eventually refinance, purchase additional properties, or seek other financing.

Your mortgage payment history can also support alternative credit profiles used by specialized lenders, gradually expanding your access to the broader financial system.

What’s the real value of homeownership beyond financial returns? For many ITIN borrowers, stability and community integration matter as much as wealth building.

Homeownership provides:

These intangible benefits compound over years and decades, creating quality of life improvements that transcend balance sheets. Your home becomes the center of your American experience, regardless of your citizenship status.

Explore all loan programs to compare financing options for non-citizens.

Who qualifies for ITIN mortgage financing? While requirements vary by lender, certain standards apply across most programs.

Your Individual Taxpayer Identification Number forms the foundation of your application:

ITIN requirements:

Supporting identity documents:

Lenders verify these documents carefully since they cannot use traditional Social Security-based verification systems. Ensuring all documentation is current, consistent, and properly translated (when necessary) streamlines the approval process.

How do lenders verify income without W-2s linked to Social Security numbers? ITIN loans use alternative documentation methods:

For employed borrowers:

For self-employed borrowers:

Most lenders require a filing history showing consistent tax compliance. Typically, you’ll need to provide documentation for the most recent tax years, demonstrating stable or increasing income patterns.

Missing tax returns or inconsistent filing creates significant obstacles, as tax compliance serves as the primary income verification method for ITIN borrowers.

Traditional credit scores may be unavailable or limited for ITIN borrowers. Lenders evaluate creditworthiness through alternative means:

Alternative credit documentation:

These alternative credit sources demonstrate your financial responsibility when traditional credit reports offer insufficient information. Providing comprehensive documentation showing 12-24 months of consistent, on-time payments strengthens your application significantly.

If you have traditional credit:

Any traditional credit you’ve established supplements alternative documentation, potentially improving your loan terms and approval odds.

Why do ITIN loans require substantial reserve funds? Reserves demonstrate financial stability and ability to weather unexpected challenges.

Typical reserve requirements:

The exact reserve requirements vary based on:

Higher reserves compensate for the lack of traditional credit data and demonstrate your ability to maintain payments during income disruptions. These funds must typically be seasoned (in your accounts for a documented period) rather than recently deposited.

What documents should you prepare before applying? Thorough preparation significantly speeds the approval process.

Essential documentation checklist:

Identity and ITIN verification:

Income documentation:

Asset verification:

Credit and payment history:

Property documentation (for purchases):

Organizing these documents before starting your application prevents delays and demonstrates your preparedness to lenders.

Not all mortgage lenders offer ITIN loan programs. Finding the right lending partner is crucial:

What to look for in ITIN lenders:

ITIN lending requires specialized knowledge of documentation requirements, alternative verification methods, and the unique challenges non-citizen borrowers face. Lenders experienced in this niche navigate the process more efficiently and advocate effectively on your behalf.

Don’t hesitate to interview multiple lenders about their ITIN program experience, approval rates, and typical timelines before committing to work with one.

How do underwriters evaluate ITIN loan applications? The manual underwriting process examines your entire financial picture:

Underwriting evaluation factors:

Manual underwriting takes longer than automated systems but allows for nuanced evaluation of your circumstances. Underwriters can consider positive factors that automated systems might overlook, such as increasing income trends, strong alternative credit, or substantial reserves.

Be prepared to provide additional documentation or clarification during underwriting. Prompt responses to requests keep your application moving forward efficiently.

ITIN loan processing typically takes longer than traditional mortgages due to manual underwriting and documentation verification:

Typical timeline breakdown:

Total timeline from application to closing often spans 45-75 days, though complex situations may require additional time. Starting early and maintaining organized documentation helps minimize delays.

During purchase transactions, working with experienced real estate agents familiar with ITIN financing ensures purchase contracts include appropriate timelines that accommodate your financing needs.

Want to discuss your specific purchase scenario? Submit a purchase inquiry to explore your options.

Employment isn’t strictly required—what matters is demonstrable income sufficient to support mortgage payments. Many ITIN borrowers qualify through:

The key is providing documentation that proves stable, reliable income likely to continue. Self-employment often requires more extensive documentation but is absolutely acceptable when properly verified through tax returns and financial statements.

Some borrowers combine multiple income sources to meet qualification thresholds, which is perfectly acceptable if all income is properly documented and verified.

Yes, gift funds from acceptable sources can supplement or fully cover your required investment:

Gift fund requirements:

Gift funds help borrowers who have sufficient income and creditworthiness but limited savings for the initial investment. Some lenders limit how much of your investment can come from gifts, particularly for investment properties.

Documenting gifts properly from the beginning prevents underwriting delays or complications near closing.

Can you finance any property type with an ITIN loan? Most residential property types qualify, though requirements vary:

Eligible property types:

Occupancy types:

Each property type and occupancy category has different qualification requirements. Primary residences typically offer the most favorable terms, while investment properties require larger investments and more substantial reserves.

Property condition matters significantly—most ITIN lenders require properties to meet standard livability and safety requirements without major defects or necessary repairs.

Your ITIN must be current and valid throughout the application process. ITINs issued before 2013 may have expired and require renewal through the IRS.

ITIN renewal considerations:

If your ITIN expired and you haven’t filed taxes recently, renewing your ITIN and filing current returns before applying for a mortgage saves significant time and prevents approval obstacles.

Working with a tax professional experienced in ITIN matters ensures your tax situation supports mortgage approval rather than creating complications.

ITIN loans often involve higher costs due to additional risk factors and manual processing:

Potential cost differences:

However, these increased costs must be weighed against the alternative—no homeownership at all. For many ITIN borrowers, slightly higher costs represent worthwhile investments in building equity and achieving housing stability.

Shopping among multiple ITIN lenders helps you find competitive pricing, as costs vary significantly between programs. The least expensive option isn’t always best—consider the lender’s expertise, service quality, and likelihood of successfully closing your loan.

What happens if you eventually obtain a Social Security number? Transitioning to traditional financing becomes possible and often advantageous.

When you might refinance to traditional mortgages:

Having established mortgage payment history makes refinancing easier, as you’ve demonstrated creditworthiness through actual performance. Your home becomes a bridge asset, allowing you to build credit and financial history that eventually qualifies you for mainstream financing products.

Even without status changes, refinancing your ITIN loan to better ITIN loan terms becomes possible as markets change, your financial profile strengthens, or you build additional equity.

See how other ITIN holders have successfully used this financing:

Calculate your ITIN loan scenarios:

If an ITIN loan isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

How many years of tax returns do you need? Most ITIN lenders require documentation spanning recent tax years showing:

Tax return essentials:

Self-employed borrowers need complete business returns showing profitable operations and sustainable income. Employed borrowers need returns demonstrating W-2 income matching employment verification.

Gaps in tax filing history create significant obstacles. If you haven’t filed recently, working with a tax professional to catch up on filing before applying for mortgages improves approval odds substantially.

ITIN loan availability varies significantly by state due to different regulatory environments and lender appetites:

State-by-state considerations:

High-population states with substantial immigrant communities typically have more developed ITIN lending markets. Rural areas or states with smaller immigrant populations may have limited lender options.

Working with lenders who operate nationally or specialize in ITIN financing helps overcome geographic limitations. Many experienced ITIN lenders can work with borrowers across multiple states through licensed loan officers.

Yes, ITIN investment property loans are available, though qualification requirements are stricter than primary residence financing:

Investment property considerations:

Investment property ITIN loans work best for borrowers with:

Starting with a primary residence purchase often makes more sense, allowing you to build equity and establish mortgage payment history before transitioning to investment properties.

How does employment loss affect pending ITIN loan applications? This creates significant complications that require immediate communication with your lender:

Options when employment changes occur:

Lenders verify employment shortly before closing, so employment changes discovered late in the process can derail approvals. Immediate notification gives lenders time to explore alternatives rather than discovering issues at the worst possible moment.

Maintaining emergency reserves and stable employment during the application period protects your approval and closing timeline.

Self-employed ITIN borrowers often experience variable income that requires careful documentation:

Underwriter evaluation of variable income:

Providing context for income variations helps underwriters understand your situation:

CPA-prepared financial statements, business bank statements showing consistent deposits, and detailed explanations help underwriters see beyond raw tax return numbers to understand your actual earning capacity.

Who can help you qualify by joining your application? Co-borrowers strengthen applications by combining income and assets:

Co-borrower requirements:

Co-signers (non-occupying co-borrowers) face restrictions:

Most ITIN lenders prefer occupying co-borrowers who will live in and have ownership stakes in the property. This aligns interests and reduces default risk compared to non-occupying guarantors.

ITIN lenders typically require properties to meet minimum condition standards:

Property condition requirements:

Commonly problematic conditions:

Properties requiring extensive repairs before occupancy often don’t qualify for standard ITIN financing. In these cases, renovation loan programs that combine purchase and improvement costs may offer better solutions.

What strategies help ITIN borrowers establish conventional credit profiles? Building credit opens doors to better financing terms and broader opportunities:

Credit-building strategies for ITIN borrowers:

As you build credit history, periodically checking whether traditional mortgages become available to you makes sense. Even modest credit scores can qualify you for conventional financing with better terms than ITIN-specific products.

Your mortgage payment history becomes your most powerful credit reference, even if it doesn’t immediately appear on traditional credit reports.

What should you do if your ITIN loan application is declined? Understanding denial reasons helps you develop an action plan:

Common denial reasons and solutions:

Request specific denial reasons in writing and discuss with your loan officer what changes would result in approval. Some issues can be resolved quickly, while others require months of preparation.

Working with different lenders also makes sense, as program requirements vary. One lender’s denial doesn’t mean all lenders will decline—specialized ITIN lenders may accommodate situations that mainstream lenders cannot.

Can ITIN borrowers deduct mortgage interest on tax returns? Yes—ITIN holders have the same tax benefits as citizens:

Mortgage-related tax considerations:

Working with tax professionals experienced in ITIN filer situations ensures you maximize available deductions and properly report real estate transactions. Your mortgage interest statements provided annually by your lender document deductible interest paid.

These tax benefits improve the after-tax cost of homeownership compared to renting, where no deductions offset your housing expenses.

Ready to get started? Apply now or schedule a call to discuss your situation.

IRS Individual Taxpayer Identification Number Information – Official IRS resource covering ITIN application procedures, renewal requirements, and proper usage for tax filing purposes.

IRS Non-Resident Alien Tax Filing Requirements – Federal guidance on tax obligations for non-residents, including filing requirements, deductions, and treaty benefits.

Consumer Financial Protection Bureau Mortgage Guide for Non-Citizens – Federal consumer protection resource explaining mortgage rights and options for non-citizens pursuing homeownership.

Federal Trade Commission Credit Building Guidance – Government advice on establishing credit history, understanding credit reports, and improving creditworthiness.

Consumer Financial Protection Bureau Guide to Alternative Credit Data – Information about alternative credit evaluation methods including rent payment history and utility accounts.

HUD Fair Housing Information – Federal resources on housing discrimination protections, fair lending laws, and filing complaints if you experience discrimination.

Fannie Mae HomeReady Mortgage Overview – Information about flexible conventional mortgage options that may become available as you build credit and residency history.

Federal Reserve Consumer Credit Resources – Federal Reserve educational materials on credit, mortgages, and personal financial management.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and tax professionals experienced in working with ITIN borrowers in your area.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.