Introduction

Not every home purchase fits into a standard lending box. Life’s most meaningful real estate transactions often involve unique circumstances that require creative solutions.

Whether you’re navigating clouded titles, buying from family, purchasing in flood zones, or financing as a foreign national, specialized mortgage programs exist. These aren’t exotic products reserved for the wealthy—they’re practical solutions for real-world situations.

The challenge isn’t finding financing for complex situations. The challenge is knowing which program matches your specific circumstances and understanding how to qualify. Many buyers spend months pursuing conventional financing only to discover they needed special financing from the start.

Key Summary

In this comprehensive guide you’ll discover:

- Clouded title strategies and how to secure financing for properties with title defects through specialized underwriting approaches

- Foreign national mortgage solutions for non-U.S. citizens investing in American real estate through passport-based qualification programs

- Co-borrower versus co-signer distinctions that impact your approval odds and long-term liability differently under various lending scenarios

- Arms length transaction requirements ensuring property purchases meet regulatory standards for legitimate financing relationships

- Flood zone financing strategies addressing FEMA requirements while managing elevated insurance obligations successfully

What Is Special Financing and When Do You Need It?

Special financing refers to mortgage programs designed for non-standard situations. These aren’t subprime loans from the 2008 crisis—they’re legitimate products offered by reputable lenders for specific circumstances.

Standard conventional and government loans follow strict eligibility boxes. Property must be in excellent condition. Title must be clear. Transaction must be arms length. Borrower must have traditional employment.

When your situation falls outside these parameters, special financing through portfolio lenders becomes necessary. These lenders hold loans in their own portfolio rather than selling to Fannie Mae or Freddie Mac. This flexibility allows creative underwriting for legitimate situations.

How Do You Know If You Need Special Financing?

Standard financing breaks down when you encounter specific roadblocks. Title issues emerge during the purchase process. Property characteristics don’t meet agency guidelines.

Your income structure doesn’t fit traditional verification methods. The transaction involves family members. The property sits in a challenging insurance market.

Each situation requires different specialized solutions. Understanding which category your challenge falls into determines which financing alternative matches your needs best.

What Makes Special Financing Different From Traditional Mortgages?

The underwriting approach focuses on compensating factors rather than rigid checkboxes. Lenders evaluate the overall strength of your application instead of declining for a single issue.

Higher reserves might compensate for employment gaps. Larger initial investments might offset property condition concerns. Strong credit history might overcome non-standard income documentation.

Portfolio lenders making these decisions keep skin in the game. They’re incentivized to approve sound loans because they’ll service them long-term. This alignment creates opportunities when agency lenders must decline.

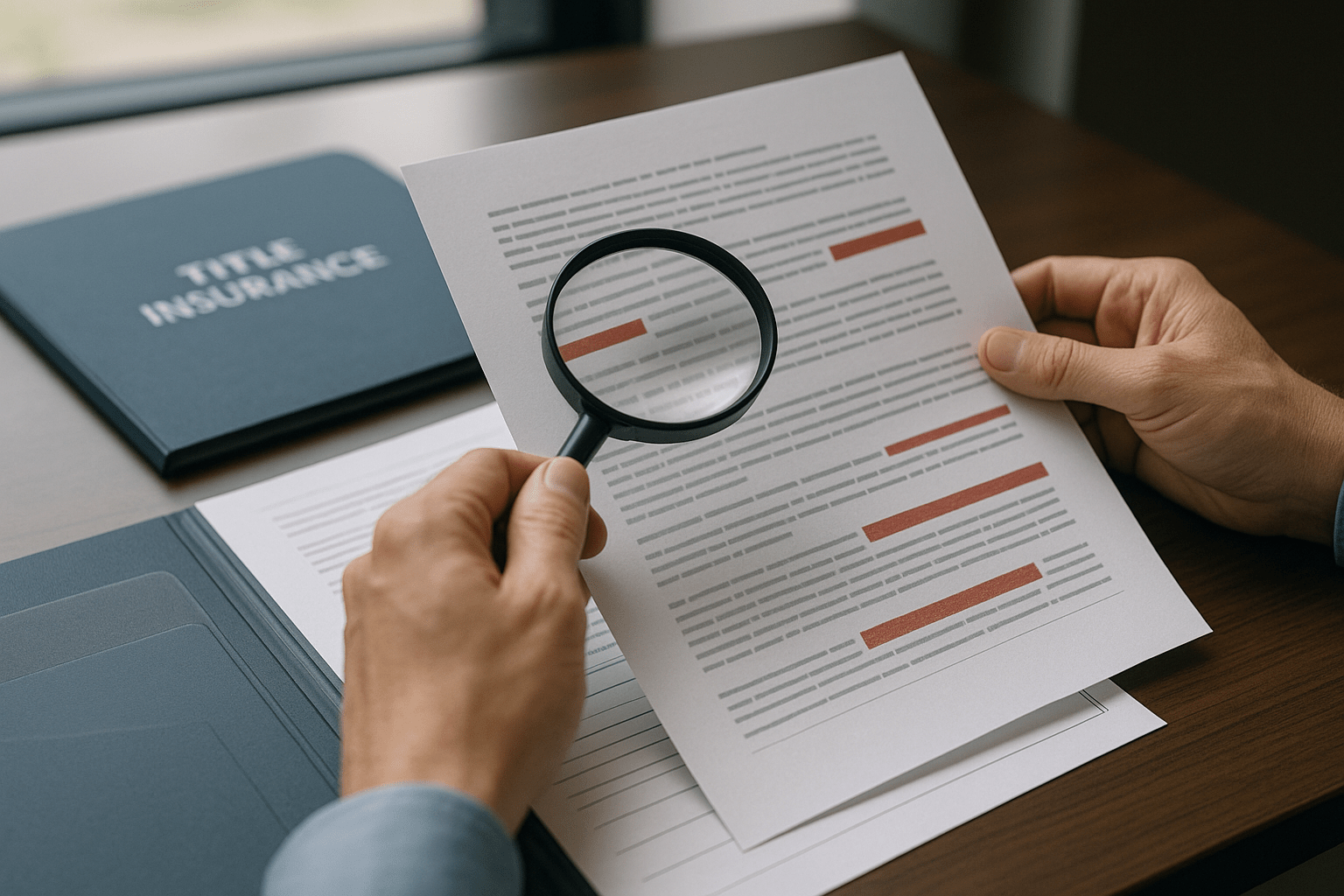

Clouded Title: Buying Property With Title Defects

Title problems represent one of the most common special financing situations. Properties with unresolved liens, boundary disputes, or ownership questions can’t close through standard channels.

The term “clouded title” simply means uncertainty exists about legal ownership. This doesn’t make the property worthless—it means resolving the title issue before or during purchase.

Smart buyers who identify clouded title opportunities early can negotiate substantial discounts. The key is structuring financing that accommodates title clearing as part of the transaction.

What Causes Title Problems That Require Special Financing?

Estate situations create frequent title clouds when heirs haven’t probated properly. Deceased owners’ names remain on the deed. Competing claims emerge among family members. Banks file mechanic’s liens that weren’t properly released after satisfaction.

Boundary disputes arise when surveys don’t match recorded plats. Neighbors claim portions of the property through adverse possession. Easements weren’t properly documented or released.

Divorce situations leave both spouses on title after the decree. Foreclosure processes weren’t completed correctly. Tax liens attach but weren’t discovered until purchase.

How Do You Clear Title Issues To Enable Financing?

The first step involves a comprehensive title search identifying every defect. Title companies won’t issue insurance until all problems resolve. Your real estate attorney develops a clearing strategy.

Simple issues like released liens just need documentation located. Bank contacts confirmed the lien was paid. Recording the release with the county clears the cloud.

Complex situations require quiet title actions through the courts. You file a lawsuit against all potential claimants. The judge declares your ownership rights. Portfolio lenders can close once legal proceedings initiate with proper escrow holdbacks.

Can You Buy Property Before Title Is Completely Clear?

Yes, through careful escrow structuring and specialized underwriting. The purchase contract includes specific timelines for title clearing. The lender reviews the clearing plan before committing to finance.

Escrow holds back sufficient resources to address remaining issues. The title company provides preliminary commitment showing their clearing path. The lender closes with title insurance exceptions for known defects.

Upon resolution, the escrow releases holdback resources. The title company removes exceptions from the final policy. Bridge financing often structures these transactions while permanent financing follows clearing.

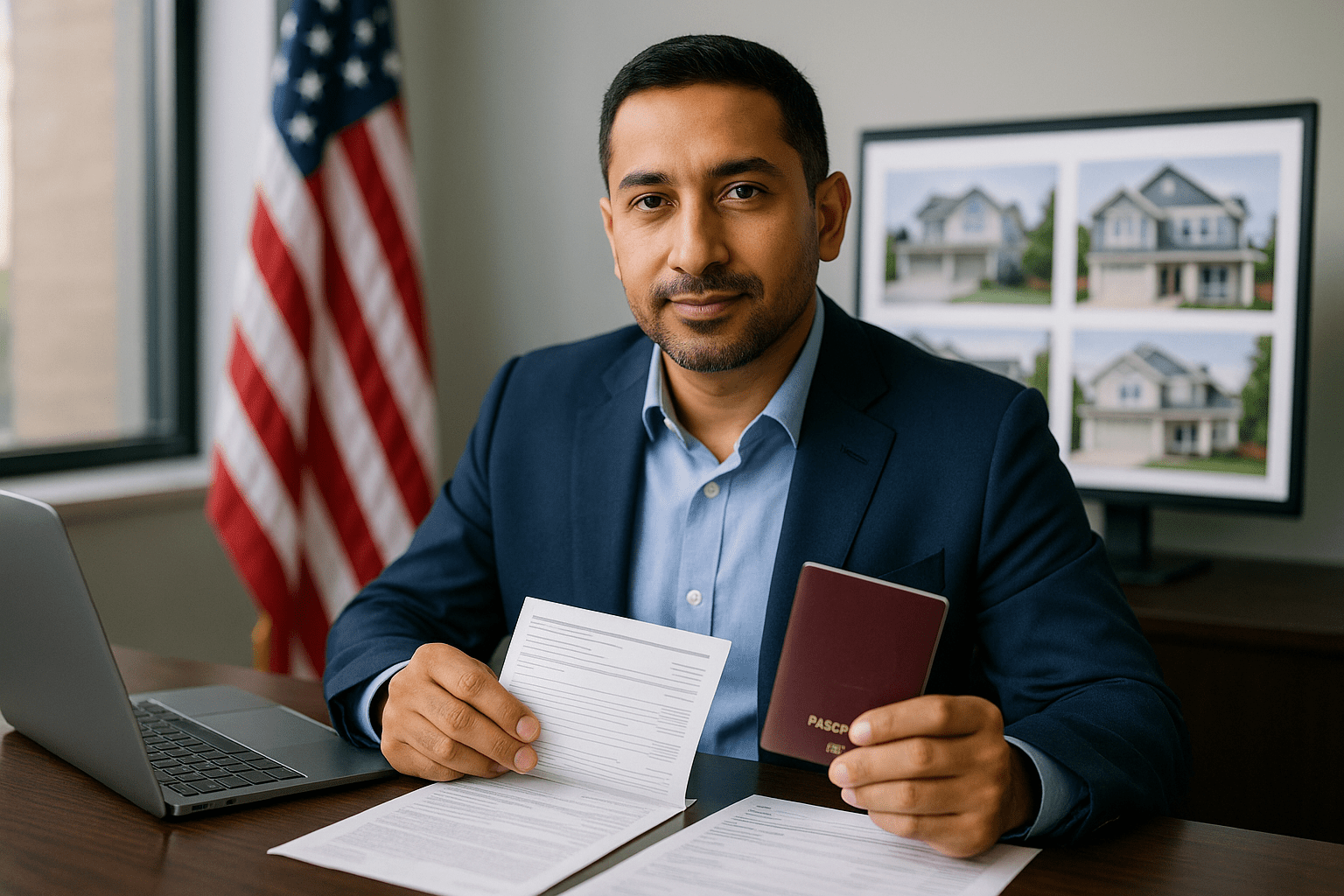

Foreign National Mortgage Solutions for Non-U.S. Citizens

Foreign nationals purchasing American real estate face unique financing challenges. You can’t establish traditional U.S. credit history. Social Security numbers aren’t available for standard credit pulls. Employment verification crosses international borders.

These obstacles don’t make financing impossible—they require specialized programs. Foreign national mortgages focus on the property’s strength and your international credentials rather than U.S.-centric metrics.

Foreign national loan programs have grown substantially as international real estate investment increases. Lenders developed specific underwriting guidelines for non-U.S. citizens with strong financial profiles.

What Documents Do Foreign Nationals Need for U.S. Mortgage Approval?

Your passport serves as primary identification instead of driver’s license or Social Security card. Visa documentation shows your legal right to own U.S. property. Bank statements from your home country demonstrate financial capacity.

Employment verification letters from international employers confirm income. Tax returns from your home country validate earnings. Credit reports from your home nation establish payment history.

Property insurance quotes address the specific property location. Rental projections document expected income if buying investment property. Down payment source documentation proves legitimate funds origin.

How Much Down Payment Do Foreign National Loans Require?

Expect minimum 25-30% initial investment for most foreign national programs. Some lenders require 35-40% for certain property types or locations. Investment properties typically need higher percentages than second homes.

The larger equity requirement protects lenders from cross-border collection challenges. If you default, pursuing legal action internationally adds complexity. The substantial equity cushion reduces default likelihood and improves recovery potential.

Higher initial investments often unlock better interest rates and terms. The 30% tier offers more competitive pricing than 25% programs. Reaching 35-40% can access institutional rates.

Can Foreign Nationals Refinance Their U.S. Property Investment?

Yes, foreign national refinance programs exist for rate improvement and cash-out scenarios. You’ll need updated income documentation and property valuation. Your payment history on the existing mortgage matters significantly.

Cash-out refinancing allows accessing equity for additional investments. Lenders typically limit cash-out to 70-75% of property value. Rate-and-term refinancing can achieve better pricing without extracting equity.

Foreign national refinance programs require similar documentation to purchase loans. Your track record of successful U.S. mortgage payments strengthens your refinance application.

What Interest Rates Should Foreign Nationals Expect?

Foreign national rates typically run 0.50-1.50% above conventional conforming rates. The premium reflects additional servicing complexity and collection risk. Stronger borrower profiles achieve pricing at the lower end.

Properties in prime locations with strong rental demand qualify for better rates. Higher credit scores in your home country improve pricing. Larger initial investments reduce lender risk and lower rates.

Using an experienced foreign national loan specialist helps identify lenders offering competitive terms. Rate shopping across multiple foreign national programs can save thousands annually.

Co-Borrower vs Co-Signer: Adding Someone to Strengthen Your Application

Adding another person to your mortgage application can make or break approval. But the relationship structure—co-borrower versus co-signer—creates dramatically different obligations and outcomes.

Many buyers don’t understand the legal distinction until closing. This confusion causes family conflict and unexpected financial burdens. Choosing the wrong structure for your situation creates problems for years.

Understanding co-borrower and co-signer differences before applying protects all parties involved. Each serves distinct purposes with unique pros and cons.

What Is a Co-Borrower and How Does It Work?

A co-borrower shares full ownership and responsibility for the property and mortgage. Both names appear on the title deed and the mortgage note. Both incomes, assets, and credit profiles factor into qualification.

The lender considers both applicants’ complete financial pictures. Co-borrowers must sign all mortgage documents. Both parties have equal rights to occupy and control the property.

FHA loans specifically structure co-borrower arrangements for family members assisting with qualification. Married couples nearly always apply as co-borrowers.

What Is a Co-Signer and How Does It Differ?

A co-signer guarantees the mortgage but doesn’t hold ownership rights. Their name appears on the mortgage note but not the property title. Their income and credit strengthen the application.

If the primary borrower defaults, the co-signer becomes legally obligated. They can’t make property decisions or claim any ownership. The mortgage appears on their credit report affecting future borrowing capacity.

Co-signers provide qualification support without ownership interest. Parents often co-sign for children’s first home purchases.

How Do Lenders View Co-Borrowers Versus Co-Signers?

Lenders prefer co-borrowers because ownership aligns interests. Both parties lose their investment if the mortgage defaults. This shared risk typically strengthens long-term payment performance.

Co-signers provide backup support but lack direct ownership incentive. Lenders view them as secondary resources. The primary borrower’s strength matters more than co-signer credentials.

Some loan programs don’t allow co-signers at all. FHA specifically requires non-occupant co-borrowers to have ownership interest. VA loans allow veterans to use non-veteran co-borrowers.

What Are the Tax Implications of Co-Borrower vs Co-Signer Arrangements?

Co-borrowers can typically deduct their portion of mortgage interest paid. The IRS allows deductions proportional to ownership percentage. Both parties can claim the mortgage interest deduction if both pay.

Co-signers generally can’t deduct mortgage interest because they lack ownership. They’re guarantors, not owners. Even if making all payments, the IRS disallows their interest deduction.

FHA non-occupant co-borrower programs create unique tax situations. Your CPA should review the specific structure before committing.

Can You Remove a Co-Borrower or Co-Signer Later?

Removing either requires refinancing the mortgage in the remaining borrower’s name alone. They must qualify independently without the additional income and credit. The original lender won’t simply delete someone from the obligation.

Co-borrowers must also execute quit claim deeds transferring ownership. The remaining owner becomes sole title holder. Removing co-signers only requires refinancing the note.

Refinancing to remove someone works best after building payment history and equity. Most lenders want 12-24 months of on-time payments before considering removal.

Arms Length Transaction Requirements and Why They Matter

An arms length transaction occurs between unrelated parties negotiating at market conditions. Both sides pursue their own interests independently. No family relationship, business partnership, or other connection exists.

Mortgage lenders require arms length transactions for standard financing programs. This prevents inflated appraisals and fraudulent property flipping. The requirement protects both lenders and taxpayers guaranteeing loans.

When transactions don’t meet arms length standards, specialized financing becomes necessary. Understanding these requirements before beginning your home search prevents surprises.

What Relationships Violate Arms Length Transaction Rules?

Parent-child purchases fail arms length requirements regardless of price fairness. Siblings buying from siblings don’t qualify. Transactions between business partners trigger scrutiny.

Purchases from employers to employees raise red flags. Sales between LLC members or corporate shareholders need additional review. Any relationship creating potential conflict of interest requires disclosure.

Even close friends with documented financial ties might face arms length challenges depending on specifics. Lenders examine all connections between parties.

Why Do Lenders Care About Arms Length Transactions?

Fraud prevention drives arms length requirements. Related parties can artificially inflate sales prices to extract maximum financing. The borrower receives cash back at closing they shouldn’t have.

Appraisals between related parties might not reflect true market value. The borrower overpays to benefit the seller. The lender extends more credit than the property secures.

Government-backed programs like FHA and VA strictly enforce arms length rules. Taxpayers ultimately backstop these loans. Preventing fraud protects the insurance funds.

How Can You Buy Property From Family Members?

Portfolio lenders structure non-arms-length purchases when circumstances warrant. They’ll scrutinize the transaction more carefully. You’ll need strong documentation proving legitimate market pricing.

An independent appraisal establishes true property value. The purchase price should match or fall below appraised value. Comparable sales in the neighborhood support the pricing.

Portfolio loan programs for family purchases typically require larger initial investments. Expect 20-25% minimums instead of 3-5% conventional options. Higher equity reduces lender risk.

What Documentation Proves Arm’s Length Intent?

Written purchase contracts with standard terms and contingencies demonstrate legitimacy. Market-rate negotiation processes with inspection periods show typical buyer behavior. Third-party appraisals by licensed professionals establish independent value assessment.

Disclosure of all relationships between parties creates transparency. Documentation of marketing efforts proves the property was available to unrelated buyers. Comparable analysis showing similar neighborhood sales supports pricing.

Bridge financing often structures complex family transactions. The temporary financing allows time for establishing arms length credentials for permanent financing.

Judgment Lien Complications: Buying or Selling With Outstanding Debts

Judgment liens attach to property when someone loses a lawsuit and owes money. The creditor records the judgment with the county. Any property the debtor owns becomes collateral for the debt.

These liens must be addressed before title can transfer cleanly. Buyers won’t accept property with existing liens. Sellers can’t convey clear title with judgments attached.

Specialized financing structures can close transactions while judgment liens undergo resolution. Understanding your options prevents deals from falling apart.

How Do Judgment Liens Affect Property Sales?

Title searches reveal all recorded liens during the purchase process. Any judgment against the current owner creates a title defect. The lien must be satisfied before closing can occur.

Sellers must pay off judgment liens from sales proceeds. The title company handles the payoff at closing. Net proceeds to the seller reduce by the judgment amount.

Sometimes judgment amounts exceed available equity. The seller can’t close because liens exceed property value. Creative financing solutions or short sales become necessary.

Can Buyers Purchase Property With Existing Judgment Liens?

Standard financing requires clear title at closing. The lender won’t fund until all liens release. The title company won’t insure with outstanding judgments.

Buyers can negotiate seller responsibility for clearing liens. The purchase contract specifies lien satisfaction as a closing condition. The seller must resolve before closing occurs.

Portfolio lenders might close with specific lien clearing timelines and escrow holdbacks. The structure protects the buyer while allowing transaction completion.

What If the Judgment Lien Amount Is Disputed?

Disputed judgments require legal resolution before closing. The seller’s attorney negotiates with the creditor. Settlement amounts often reduce from the original judgment.

The title company might issue title insurance with specific exceptions. They exclude the disputed lien from coverage. This allows closing while legal proceedings continue.

Bridge financing can fund the purchase while dispute resolution happens. Permanent financing follows once the title clears completely.

How Long Do Judgment Liens Remain on Property?

Most states allow judgment liens for 10-20 years. Creditors can renew expired judgments for additional terms. The lien remains until satisfied or legally removed.

Chapter 7 bankruptcy might discharge the underlying debt. However, liens recorded before bankruptcy often survive. The property still carries the judgment attachment.

Understanding your state’s specific laws helps develop clearing strategies. Real estate attorneys specializing in title issues provide crucial guidance.

Foreclosure Mortgage Options: Financing After or During Foreclosure

Foreclosure impacts your ability to obtain financing for years. How long depends on the loan program and whether you completed the foreclosure or avoided it through alternatives.

Many people believe foreclosure means permanent disqualification from homeownership. This isn’t true—waiting periods exist, but future mortgage approval remains possible.

Understanding post-foreclosure financing timelines helps you plan your path back to homeownership. Different strategies shorten waiting periods.

How Long After Foreclosure Can You Buy Again?

FHA loans require three years from foreclosure completion. You must demonstrate credit rebuilding and stable housing payments. Extenuating circumstances like medical hardship might shorten the timeline.

Conventional loans typically require seven years from foreclosure. Some lenders consider four years with strong compensating factors. Credit scores must rebound to minimum qualifying levels.

VA loans allow Veterans to qualify two years after foreclosure. USDA loans require three years similar to FHA. Portfolio lenders evaluate individual circumstances more flexibly.

What If You Did a Short Sale Instead of Foreclosure?

Short sales create shorter waiting periods than foreclosure. FHA allows borrowing after two years instead of three. Conventional timelines drop from seven to four years.

VA loans might approve immediately after short sale with extenuating circumstances. USDA follows FHA’s two-year timeline. Portfolio lenders often approve sooner than agency guidelines.

Short sale alternatives to foreclosure preserve more of your future borrowing capacity. The credit impact proves less severe than foreclosure completion.

Can You Buy a Foreclosed Property If You Have Good Credit?

Yes, purchasing foreclosed properties doesn’t require special financing. The property’s foreclosure status differs from your foreclosure history. Any qualified buyer can purchase foreclosed real estate.

Banks selling foreclosed properties want quick sales. They’ll accept standard financing from qualified borrowers. Your good credit and stable income make you an attractive buyer.

Foreclosed property purchases often require renovation financing. Many foreclosures need repairs before meeting lending standards.

How Do You Rebuild Credit After Foreclosure?

Secured credit cards rebuild payment history immediately. You deposit money as collateral. The card company reports positive payment history monthly.

Small installment loans from credit unions establish new positive tradelines. Auto loans after foreclosure demonstrate repayment capacity. Each on-time payment improves your profile.

FHA’s Back to Work program shortens waiting periods for documented hardship. You must prove the foreclosure resulted from circumstances beyond your control.

Distressed Property Financing: Buying Fixer-Uppers

Distressed properties offer substantial discounts but present financing challenges. Standard mortgages require properties to meet minimum condition standards. Significant defects disqualify properties from conventional financing.

The property might need a new roof. Electrical systems don’t meet code. Plumbing requires complete replacement. Foundation issues exist.

Renovation loan programs specifically address distressed property purchases. They finance both the purchase and rehabilitation in a single mortgage.

What Property Conditions Disqualify Standard Financing?

Structural issues like foundation cracks or settling problems fail inspections. Roof damage with less than two years remaining life expectancy needs repair. Electrical systems without proper grounding or insufficient capacity need upgrading.

Plumbing problems including polybutylene pipes or galvanized steel require replacement. Heating and cooling systems not functioning properly disqualify properties. Major safety hazards like missing railings or exposed wiring must be corrected.

FHA appraisers specifically identify conditions violating minimum property standards. Properties failing these requirements need renovation financing or all-cash purchases.

How Do FHA 203k Loans Work for Distressed Properties?

FHA 203k loans combine purchase financing and renovation costs into one mortgage. The lender bases the loan on the property’s after-repair value. You can buy distressed properties with just 3.5% of the total project cost as initial investment.

The lender establishes a renovation escrow at closing. Contractors draw from the escrow as work completes. An inspector verifies completion before releasing funds.

Standard 203k allows unlimited improvements including structural changes. Limited 203k covers up to a specific dollar amount for non-structural repairs only.

What About Conventional Renovation Loans?

Fannie Mae’s HomeStyle Renovation loan operates similarly to FHA 203k. You can finance up to 75% of the completed property value. Minimum 5% initial investment for owner-occupied purchases.

Freddie Mac’s CHOICERenovation loan provides another conventional option. These programs offer more flexibility than FHA regarding contractor requirements. You can act as your own general contractor with proper licensing.

Conventional renovation programs don’t require upfront mortgage insurance. Once you reach 20% equity, no monthly mortgage insurance applies.

Can Investors Buy Distressed Properties With Financing?

Yes, but initial investment requirements increase significantly. Expect 20-25% minimums for investment property renovation financing. Some lenders require 30-35% for extensive rehabilitation projects.

DSCR renovation loans qualify based on the property’s projected rental income. Your personal income and employment don’t factor into approval. These programs work well for real estate investors.

Fix and flip loans provide short-term financing for distressed properties. You purchase, renovate, and resell within 12-18 months. Hard money lenders specialize in quick-close distressed property financing.

Buying a House From Parents: Navigating Intrafamily Transfers

Purchasing property from your parents creates unique financing challenges. Standard mortgage programs flag intrafamily transactions. Lenders worry about inflated pricing and undisclosed terms.

This doesn’t make parent-child purchases impossible. It requires specialized structuring and thorough documentation. Understanding the obstacles before starting prevents deal collapse.

Portfolio lenders structure legitimate intrafamily purchases regularly. The key is proving market-rate transactions and legitimate qualification.

Why Do Lenders Restrict Parent-Child Property Purchases?

Fraud prevention drives these restrictions. Related parties could inflate sales prices to generate cash back at closing. Parents might secretly forgive initial investment requirements.

Appraisers might inflate values to help family members. The stated purchase price might not reflect actual consideration. These scenarios create losses when properties default.

Government-backed programs like FHA strictly prohibit non-arms-length purchases. Fannie Mae and Freddie Mac enforce similar guidelines for conventional loans.

How Can You Finance Purchasing Your Parents’ Home?

Portfolio lenders evaluate intrafamily purchases individually. They require independent appraisals establishing market value. The purchase price should match or fall below the appraisal.

You’ll need standard qualification including income verification and credit review. The initial investment typically runs 15-25% instead of conventional 3-5% options. Larger equity reduces lender risk concerns.

Documentation proving legitimate arms-length intent strengthens your application. Written purchase contracts with standard terms help. Disclosure of the family relationship creates transparency.

What If Your Parents Want to Gift You the Equity?

Gift equity structures allow parents to “sell” below market value. The difference between appraised value and sales price becomes your equity. This requires specific gift equity documentation.

Parents must sign gift letters stating no repayment expectation. The transaction still needs qualified appraisal. Conventional gift equity guidelines allow up to the full initial investment from gift equity.

FHA doesn’t permit gift equity on non-arms-length purchases. You’ll need actual cash for the minimum 3.5% investment. Parents can gift cash before closing for this purpose.

Can Parents Carry Financing Instead of Using a Bank?

Yes, seller financing between parents and children works when structured properly. Parents hold a mortgage note secured by the property. You make payments directly to your parents.

This arrangement needs legal documentation including promissory notes and recorded mortgages. An attorney should draft all paperwork. The IRS requires parents to charge minimum interest rates.

Combining seller financing with institutional financing gets more complex. Most lenders won’t allow subordinate liens from family members.

What Tax Implications Affect Parent-Child Property Sales?

Your parents might owe capital gains taxes on the sale. Their primary residence exclusion could eliminate this. They can exclude up to a specific amount of gain if they lived there two of the past five years.

You can’t deduct the interest paid to your parents unless the loan is properly documented. A recorded mortgage and promissory note meeting IRS requirements enable deductions. Proper structure ensures you maximize tax benefits.

Gift tax implications arise if parents sell substantially below market value. The IRS considers the difference a gift subject to gift tax rules. Annual exclusion amounts allow certain gifts without filing requirements.

Buying a House in a Flood Zone: FEMA Requirements and Insurance

Properties in designated flood zones require special insurance and face financing restrictions. FEMA flood maps identify high-risk areas. Properties in these zones must maintain flood insurance as a mortgage condition.

Many buyers don’t research flood zones until after going under contract. Then they discover insurance costs thousands annually. The surprise often kills deals.

Understanding flood zone financing before beginning your search prevents surprises. The right preparation makes flood zone purchases viable.

What Are FEMA Flood Zones and How Do They Work?

FEMA creates flood maps showing areas with different flood risks. High-risk zones designated with “A” or “V” have 1% annual flood chance. Moderate-to-low risk zones use “B,” “C,” or “X” designations.

Properties in high-risk zones require flood insurance for federally backed mortgages. This includes FHA, VA, USDA, and conventional loans sold to Fannie Mae or Freddie Mac. The insurance requirement continues for the loan’s life.

Flood zone determinations occur during the appraisal process. The appraiser orders a flood certification. This identifies the property’s exact flood zone designation.

How Much Does Flood Insurance Cost in High-Risk Zones?

Flood insurance costs vary dramatically by location and flood zone. Properties in high-risk coastal areas might pay several thousand dollars annually. Inland properties in moderate flood zones might pay several hundred dollars.

The National Flood Insurance Program sets rates through FEMA. Private flood insurance might cost less for some properties. Your insurance agent can compare both options.

Flood insurance costs add significantly to your housing expense. Lenders include flood insurance in debt-to-income calculations. High premiums might affect your qualification amount.

Can You Buy a Flood Zone Property Without Flood Insurance?

Not with standard financing requiring flood coverage. If you pay all cash, you can skip flood insurance. This extremely risky approach leaves you exposed to catastrophic flood damage.

Some portfolio lenders might not require flood insurance for certain low-risk zones. They’re accepting significant risk if flooding occurs. These programs typically require larger initial investments.

Most buyers in flood zones need the insurance for their own protection. A single flood can destroy your investment. The coverage protects your equity.

How Can You Reduce Flood Insurance Costs?

Elevation certificates show your property’s height relative to base flood elevation. If your home sits above the base flood level, insurance costs drop. The certification costs several hundred dollars but might save thousands annually.

Flood mitigation improvements reduce premiums. Elevating utilities and HVAC systems decreases damage potential. Installing flood vents in enclosed areas allows water flow.

Choosing higher deductibles reduces annual premiums. Building new construction above base flood elevation qualifies for preferred rates. Shopping multiple insurance carriers finds the best pricing.

What If FEMA Remaps and Your Property Enters a Flood Zone?

Property owners in newly designated flood zones receive notification. A grace period allows obtaining insurance before requirements begin. Grandfathering provisions might preserve lower rates.

You must add flood insurance even if your original mortgage didn’t require it. The lender will force-place insurance if you don’t obtain coverage. Force-placed insurance costs significantly more than voluntary coverage.

Refinancing after remapping requires compliance with new flood zone designations. You’ll need flood insurance for the new loan even if your old loan predated the mapping change.

FHA Non-Occupant Co-Borrower: Adding Family for Qualification

FHA allows family members to co-borrow even when they won’t live in the property. This unique program helps buyers who fall slightly short of qualification. Your parent or sibling can strengthen your application.

The non-occupant co-borrower must be a family member. Their income and credit factor into qualification. They share full mortgage responsibility despite not living there.

FHA non-occupant co-borrower programs require careful structuring. Understanding the requirements prevents application delays.

Who Qualifies as an FHA Non-Occupant Co-Borrower?

Family members including parents, siblings, children, and grandparents qualify. In-laws and step-relatives also meet the definition. Close friends don’t qualify even with strong relationships.

The non-occupant co-borrower must demonstrate qualifying income and credit. They’ll sign all mortgage documents. The loan appears on their credit report affecting future borrowing capacity.

Both occupying and non-occupying borrowers must meet FHA credit and income standards. Lenders evaluate the complete application package.

How Much Does a Non-Occupant Co-Borrower Help Your Qualification?

Their full income counts toward debt-to-income ratios. If your ratio exceeds FHA limits, their income might bring it into acceptable range. Their good credit might overcome your credit challenges.

The combined profile must meet FHA standards. Adding someone with poor credit might hurt more than help. Adding someone with excellent credit but no income provides limited benefit.

Lenders examine the complete picture when evaluating non-occupant co-borrower applications. Strong compensating factors on both sides create approval likelihood.

What Are the Non-Occupant Co-Borrower’s Obligations?

They’re fully liable for the mortgage if you default. Lenders can pursue them for the full debt. The mortgage impacts their ability to obtain future financing.

They share ownership of the property. Both names appear on the title deed. They have legal rights to the property despite not living there.

Removing non-occupant co-borrowers later requires refinancing. They must be bought out through a new loan in your name alone.

Can Non-Occupant Co-Borrowers Use Gift Equity or Cash Gifts?

Yes, non-occupant co-borrowers can provide all or part of the required initial investment. This gift must be properly documented. Gift letters confirming no repayment expectation are required.

The gift giver must prove their funds came from legitimate sources. Bank statements showing sufficient funds document gift capacity. The funds must be in your account before closing.

FHA gift requirements allow initial investment to come entirely from family gifts. This combination with co-borrowing creates powerful qualification tools.

ITIN Loans: Financing for Borrowers Without Social Security Numbers

Individual Taxpayer Identification Numbers allow non-citizens to file U.S. taxes. ITIN holders contribute billions in taxes annually. However, ITIN numbers don’t provide work authorization or Social Security benefits.

Many ITIN holders believe homeownership remains impossible without Social Security numbers. This isn’t true—specialized mortgage programs exist. Understanding ITIN loan requirements opens homeownership opportunities.

ITIN mortgage programs have grown as lenders recognize this creditworthy market. These borrowers pay their obligations reliably despite lacking traditional documentation.

What Documentation Do ITIN Borrowers Need?

Your ITIN number serves as the primary identification for the application. Two years of tax returns filed with your ITIN establish income history. Pay stubs from your employer verify current earnings.

Bank statements showing savings prove financial capacity. Utility bills in your name demonstrate residential stability. Credit references from alternative sources like rent payments establish payment history.

ITIN loan programs have developed specific underwriting for non-traditional documentation. Experienced loan officers help gather required materials.

How Much Down Payment Do ITIN Loans Require?

Minimum initial investment typically runs 10-15% for owner-occupied purchases. Some lenders require 15-20% depending on credit profile. Investment properties need 20-25% minimums.

The higher equity requirement reflects additional verification challenges. Without Social Security numbers, employment verification becomes more complex. Credit history might be limited or nonexistent.

Larger initial investments reduce lender risk and often improve interest rates. Reaching 20-25% equity creates better pricing opportunities.

What Interest Rates Should ITIN Borrowers Expect?

ITIN loan rates typically run 0.50-2.00% above conventional conforming rates. The premium reflects additional underwriting complexity. Stronger credit profiles achieve pricing at the lower end.

Larger initial investments reduce rates. Two years of tax filing history helps significantly. Stable employment with the same employer for several years improves pricing.

Rate shopping across multiple ITIN lenders finds competitive terms. Not all lenders offer ITIN programs. Working with experienced ITIN specialists matters.

Can ITIN Borrowers Refinance Their Mortgages?

Yes, ITIN refinance programs exist for rate improvement and equity access. Your payment history on the existing mortgage matters significantly. Demonstrating continued income and tax filing strengthens refinance applications.

Cash-out refinancing allows accessing equity for various purposes. Rate-and-term refinancing improves your rate without extracting equity. ITIN refinance requirements mirror purchase loan documentation needs.

Building strong payment history on your initial ITIN mortgage creates better refinance opportunities. Lenders value proven performance over theoretical qualification.

Do ITIN Loans Work in All States?

Most states allow ITIN lending without restrictions. A few states have additional requirements or limitations. Your lender can verify your specific state’s rules.

Property location affects program availability more than borrower location. Lenders prefer properties in metropolitan areas with strong markets. Rural areas might have fewer ITIN program options.

ITIN loan availability continues expanding as demand grows. More lenders enter this market each year recognizing its stability.

Portfolio Loans for Complex Situations: Lender-Held Financing

Portfolio loans solve problems that standard programs can’t address. These lenders keep loans in their own portfolio instead of selling to Fannie Mae or Freddie Mac. This freedom allows creative underwriting.

Complex income documentation becomes manageable. Non-standard property types gain financing eligibility. Unique situations receive individual evaluation instead of automated declines.

Portfolio lending provides solutions when no other options exist. Understanding how they work helps you leverage these programs.

What Situations Require Portfolio Loan Solutions?

Multiple properties with creative financing structures. Self-employment with complicated business entities. Properties that don’t meet agency property standards. Borrowers with non-traditional income sources.

Credit challenges that don’t fit standard guidelines. Debt-to-income ratios slightly exceeding agency limits. Properties in unique locations or with unusual characteristics.

Portfolio lenders evaluate the complete picture. One weakness doesn’t automatically disqualify your application.

How Do Portfolio Loan Interest Rates Compare?

Expect rates 0.50-2.50% above conventional conforming rates. The premium reflects additional risk and servicing complexity. Your specific situation determines where you fall in this range.

Stronger overall profiles achieve lower premiums. Larger initial investments reduce rates. Multiple compensating factors improve pricing. The flexibility costs something, but often provides value.

Portfolio loan costs should be compared to alternative solutions. Sometimes paying slightly higher rates enables transactions that otherwise couldn’t close.

What Property Types Work With Portfolio Loans?

Non-warrantable condominiums gain financing eligibility. Properties needing minor repairs before agency standards. Unique homes that don’t compare well to neighborhood sales. Properties with acreage or unusual lot sizes.

Mixed-use properties combining residential and commercial space. Properties in declining markets. Homes with certain structural characteristics. Properties that appraisers struggle to value using conventional methods.

Can You Refinance Portfolio Loans Later?

Yes, refinancing portfolio loans into conventional programs works after building payment history. You need 12-24 months of on-time payments. Property value must support the refinance.

If your situation that required portfolio financing resolves, conventional refinancing often makes sense. Standard programs offer lower rates. The refinancing strategy should be considered from the start.

Some borrowers keep portfolio loans long-term if the initial situation persists. Others refinance as soon as eligible for conventional terms.

Bankruptcy Mortgage: Financing After Chapter 7 or Chapter 13

Bankruptcy provides fresh financial starts but impacts mortgage eligibility temporarily. How long depends on the bankruptcy chapter and the loan program. Complete understanding helps you plan your path back.

Many people believe bankruptcy means permanent homeownership disqualification. This isn’t true—waiting periods exist, but future approval remains possible. Strategic planning shortens timelines.

Post-bankruptcy mortgage programs have specific rules. Following the guidelines maximizes your chances of timely approval.

How Long After Chapter 7 Bankruptcy Can You Buy?

FHA requires two years from discharge date. You must demonstrate credit rebuilding through new positive tradelines. Extenuating circumstances might shorten this timeline. Housing payment history since discharge matters significantly.

Conventional loans typically require four years from discharge. Some lenders consider two years with strong compensating factors. Credit scores must rebuild to minimum qualifying levels.

VA loans allow Veterans to qualify two years after discharge. USDA follows similar timing to FHA. Portfolio lenders evaluate individual circumstances.

How Do Chapter 13 Bankruptcy Waiting Periods Differ?

FHA allows purchasing during active Chapter 13 repayment plans. You need one year of on-time plan payments. The bankruptcy trustee must approve the purchase. This unique provision helps rebuilders.

Conventional loans require two years from discharge or four years from dismissal. VA might approve during active repayment with trustee consent. Chapter 13 completion demonstrates commitment to debt resolution.

What Credit Score Do You Need After Bankruptcy?

FHA minimums start at 500 for some programs. Most lenders want 580+ for competitive rates. Conventional loans need 620+ minimum. Higher scores improve approval likelihood and pricing.

Rebuilding credit after bankruptcy takes strategic effort. Secured credit cards report positive history monthly. Small installment loans establish new payment patterns.

Credit rebuilding strategies should begin immediately after discharge. The sooner you start, the faster you qualify.

Can You Refinance After Bankruptcy?

Yes, once you meet the minimum waiting period for your loan program. Refinancing follows the same timeline requirements as purchase loans. Strong payment history on your existing mortgage helps significantly.

Refinancing post-bankruptcy can lower rates or access equity. The existing mortgage performance matters more than the past bankruptcy. Two years of on-time mortgage payments creates strong refinance eligibility.

Divorce Mortgage: Buying Out Spouse or Qualifying Alone

Divorce creates complex property ownership issues. The decree might award the house to one spouse. That spouse must refinance to remove the other from the mortgage.

Qualifying alone after divorce proves challenging when the marital income supported the original loan. New debt-to-income calculations might not work. Strategic planning prevents forced home sales.

Divorce mortgage refinancing requires understanding special considerations. Options exist even when initial analysis shows problems.

How Do You Remove Your Ex-Spouse From the Mortgage?

Refinancing in your name alone is the only way to remove them. They won’t be released from the original obligation without refinancing. You must qualify independently using only your income.

The divorce decree doesn’t remove mortgage obligation. Banks didn’t participate in your divorce. They hold both parties responsible until refinancing occurs.

Refinancing to remove ex-spouses should happen quickly after divorce. Delayed refinancing creates ongoing liability for the non-occupying spouse.

What If You Can’t Qualify to Refinance Alone?

Co-borrowers can strengthen your application. FHA allows non-occupant co-borrowers from family members. Their income supplements yours for qualification.

Waiting until income increases might make sense. Taking a second job temporarily boosts qualifying income. Paying down other debts improves debt-to-income ratios.

Portfolio lenders might approve based on compensating factors. Substantial equity helps significantly. Long payment history on the existing mortgage creates strength.

Can Your Ex-Spouse Be Required to Cooperate?

The divorce decree should address refinancing obligations. Courts can order cooperation with refinancing efforts. However, enforcing these provisions takes time and legal expense.

If your ex-spouse won’t cooperate with refinancing, you might need to sell. Court enforcement of refinancing orders proves difficult. Addressing refinancing requirements clearly in divorce negotiations prevents problems.

What About Buying Your First Home After Divorce?

Divorce impacts your debt-to-income calculations if you’re still on the marital mortgage. Lenders count that payment against you even if your ex pays it. Documentation showing your ex makes payments might help.

Court orders requiring your ex to pay the mortgage create some relief. Lenders might exclude the payment with sufficient documentation. Twelve months of your ex making payments from their own account proves the pattern.

New purchase qualification works best after refinancing the marital home. This removes the obligation from your ratios completely.

Self-Employed With Complex Income: Multiple Businesses or Entities

Self-employment creates natural mortgage qualification challenges. Traditional income verification using W-2 forms doesn’t work. Tax returns become the primary income documentation.

Complex business structures with multiple entities, pass-through income, and business deductions complicate analysis. Underwriters must reconstruct your qualifying income from multiple sources.

Self-employed borrowers with complex structures benefit from specialized loan programs. Understanding options prevents unnecessary documentation headaches.

Why Do Multiple Business Entities Complicate Qualification?

Income flows through multiple tax returns requiring individual analysis. S-corporations, partnerships, and sole proprietorships each report differently. Underwriters must combine these sources accurately.

Business expenses reducing taxable income also reduce qualifying income. Legitimate deductions like depreciation don’t represent actual cash outflow. Underwriters add back certain deductions for qualification.

Complex entity structures require experienced underwriters. Standard automated systems can’t handle this analysis. Manual underwriting becomes necessary.

What Are Bank Statement Loan Programs?

Bank statement loans qualify you based on deposits rather than tax returns. Lenders analyze 12-24 months of business bank statements. Deposits demonstrate income without complex tax return analysis.

You avoid the challenge of explaining business deductions. Consistent deposit patterns prove income capacity. These programs work particularly well for businesses with high write-offs.

Bank statement programs require larger initial investments than conventional loans. Expect 10-20% minimums instead of 3-5% options. Rates run higher reflecting additional underwriting complexity.

Can You Use Multiple Years to Average Income?

Standard qualification uses two-year income averaging. If your income trends upward, this works in your favor. If income declined recently, the average hurts.

Lenders might allow using only the most recent year with strong business evidence. Contracts showing future income help. Business expansion documentation supports higher income projections.

Self-employed income analysis varies by lender and program. Some prove more flexible than others regarding income trending.

What Documentation Do Complex Self-Employed Borrowers Need?

Personal tax returns for two years including all schedules. Business tax returns for all entities you own 25%+ of. Year-to-date profit and loss statements. Current balance sheets for all businesses.

Business licenses proving legitimate operation. CPA letters explaining complex situations. Documentation of contracts or business relationships showing income stability.

Comprehensive documentation preparation before applying prevents delays. Working with mortgage professionals experienced in self-employment helps tremendously.

Property With Existing Tenant: Buying Occupied Rental Property

Purchasing property with tenants in place creates specific financing considerations. The existing lease affects your occupancy options. Lender requirements vary based on your intended use.

Some buyers want tenant-occupied properties for immediate rental income. Others want to occupy the property themselves. Your intention dramatically affects financing options.

Financing occupied properties requires understanding occupancy-based lending rules. Planning prevents qualification surprises.

Can You Buy Owner-Occupied Property With Existing Tenants?

Owner-occupancy financing requires you to occupy within 60 days of closing. Tenants must vacate before that deadline. The lease terms matter significantly.

Month-to-month tenants can receive notice relatively quickly. Fixed-term leases require respecting the lease period. Standard owner-occupancy programs don’t work if tenants have long-term leases.

Some lenders allow owner-occupancy financing if you’ll occupy one unit of a 2-4 unit property. Other units can remain tenant-occupied.

How Does Investment Property Financing Work for Occupied Properties?

Investment property financing specifically allows tenant occupancy. The rental income can count toward qualification. Lenders verify the existing lease terms and rental amount.

You’ll need a copy of the current lease agreement. Rental history showing consistent tenant payment strengthens the application. The rental income offsets the mortgage payment in debt-to-income calculations.

DSCR loans work particularly well for occupied investment properties. The property’s rental income qualifies you without personal income verification.

What If You Want to Terminate the Existing Lease?

State laws govern lease termination rights. You typically must honor existing lease terms after purchasing. Breaking valid leases requires tenant agreement or specific legal grounds.

Negotiating lease termination as part of the purchase works sometimes. The seller pays tenants to vacate before closing. This allows you to use owner-occupancy financing.

Understanding your specific state’s landlord-tenant laws prevents legal problems. Real estate attorneys provide crucial guidance on lease matters.

How Do Lenders Verify Rental Income From Existing Tenants?

Current lease agreements document rental amounts. Bank statements showing rent deposits verify payment history. Tax returns showing rental income on Schedule E provide historical context.

If you’re purchasing the property, the seller provides these documents. Your lender wants to see 12-24 months of rental history. Consistent payment patterns increase confidence.

Rental income analysis varies by loan program. Some lenders use the full rent amount. Others discount the rent to account for vacancy and maintenance.

Mixed-Use Property Financing: Residential Plus Commercial Space

Mixed-use properties combine residential and commercial purposes. The ground floor might house a business while upper floors contain apartments. These properties require specialized financing approaches.

Standard residential mortgages work when commercial space represents a small percentage. Primarily commercial properties need commercial financing. Understanding the threshold prevents pursuing wrong loan programs.

Mixed-use financing depends heavily on the specific property characteristics. Proper classification from the start prevents problems.

What Percentage of Commercial Space Triggers Commercial Financing?

Most residential programs allow commercial space up to 25% of total square footage. Properties exceeding this threshold need commercial financing. The calculation uses actual square footage, not income.

You can own-occupy the residential portion and lease the commercial space. Or you can treat the entire property as investment real estate. Your intended use affects program selection.

Portfolio lenders often provide the most flexibility for mixed-use properties. They evaluate the complete situation rather than rigid percentage rules.

Can You Use FHA or VA Loans for Mixed-Use Properties?

FHA allows mixed-use properties with specific restrictions. The commercial space must be 25% or less. You must occupy the residential portion as your primary residence. The commercial use can’t create safety hazards.

VA has similar 25% commercial space limitation. The residential portion must be your primary home. Income from the commercial space can help with qualification.

These programs provide attractive financing for qualifying mixed-use properties. Low initial investment requirements make them accessible.

How Do Appraisers Value Mixed-Use Properties?

Appraisers struggle with mixed-use valuations due to limited comparables. Finding similar mixed-use sales in the area proves challenging. The residential and commercial components need separate consideration.

The income approach values commercial space based on lease rates. The sales comparison approach values residential space using housing comparables. Combining these valuations requires judgment.

Complex appraisal situations can delay closings significantly. Building extra time into your timeline prevents problems.

What Are the Tax Benefits of Mixed-Use Properties?

Commercial portions offer more depreciation benefits than pure residential property. You can write off business expenses related to the commercial space. Home office deductions might apply if you use commercial space personally.

Separating residential and commercial expenses requires careful recordkeeping. Your CPA should review your specific situation. Tax strategies for mixed-use properties maximize benefits while maintaining IRS compliance.

Frequently Asked Questions About Special Financing

What is clouded title and can I get a mortgage with it?

Clouded title means legal uncertainty exists about property ownership. Unresolved liens, boundary disputes, or inheritance issues create clouds. Standard mortgages require clear title at closing.

However, specialized lenders can close while title issues undergo resolution. They structure escrow holdbacks to cover resolution costs. Portfolio lenders examine the specific situation and clearing timeline before committing.

Bridge financing often structures these transactions. Permanent financing follows once title clears completely.

How do foreign nationals qualify for U.S. mortgages without Social Security numbers?

Foreign national mortgage programs use passport-based qualification instead of Social Security numbers. Lenders verify international employment and income. Bank statements from your home country prove financial capacity.

Credit reports from your home nation establish payment history. Expect 25-35% initial investment requirements. Foreign national programs focus on property strength and international credentials.

Rates typically run 0.50-1.50% above conventional conforming rates.

What’s the difference between a co-borrower and co-signer?

Co-borrowers share full ownership and responsibility for the property. Both names appear on the title deed and mortgage note. Both incomes and credit profiles factor into qualification.

Co-signers guarantee the mortgage but don’t hold ownership rights. Their name appears on the mortgage note only. FHA requires non-occupant co-borrowers to have ownership interest.

Removing either later requires refinancing in the remaining party’s name alone.

Why do lenders care about arms length transactions?

Arms length transactions occur between unrelated parties negotiating independently. This prevents inflated pricing and fraudulent cash-back schemes. Lenders protect themselves from coordinated fraud between related parties.

Government-backed programs strictly prohibit non-arms-length purchases. Portfolio lenders evaluate intrafamily purchases individually. They require independent appraisals and larger initial investments.

Can you buy a house from your parents with a mortgage?

Yes, through portfolio lenders willing to structure non-arms-length purchases. You’ll need independent appraisal establishing market value. The purchase price should match or fall below appraised value.

Expect 15-25% initial investment instead of 3-5% conventional options. Portfolio programs for family purchases require extensive documentation proving legitimate transaction intent.

Gift equity structures allow parents to “sell” below market value in some situations.

How do judgment liens affect property sales?

Judgment liens must be satisfied before title can transfer cleanly. Sellers must pay off liens from sales proceeds. Sometimes lien amounts exceed available equity.

Portfolio lenders might close with specific lien-clearing timelines and escrow holdbacks. The buyer’s title insurance excludes the judgment until resolution occurs.

Bridge financing can fund purchases while dispute resolution happens.

How long after foreclosure can you buy another home?

FHA requires three years from foreclosure completion. Conventional loans typically require seven years. VA loans allow Veterans to qualify after two years.

Short sales create shorter waiting periods. Post-foreclosure timelines vary by program and circumstances. Extenuating circumstances might shorten requirements.

Credit rebuilding should begin immediately after discharge.

Can you get a mortgage for a fixer-upper that needs major repairs?

Yes, through renovation loan programs combining purchase and repair financing. FHA 203k loans finance both components with just 3.5% initial investment. Conventional HomeStyle Renovation loans offer similar structure.

The lender bases the loan on after-repair value. Renovation loans establish repair escrow at closing. Contractors draw funds as work completes.

Standard 203k allows unlimited improvements including structural changes.

What documents do you need to buy a house in a flood zone?

Flood zone purchases require standard mortgage documents plus flood insurance. FEMA flood zone determination occurs during appraisal. Properties in high-risk zones need National Flood Insurance Program coverage.

The insurance requirement continues for the loan’s life. Flood insurance costs vary dramatically by location and flood zone designation.

Elevation certificates might reduce insurance costs if your home sits above base flood elevation.

Can you buy investment property with tenants already in place?

Yes, investment property financing specifically allows tenant occupancy. The existing rental income can count toward qualification. Lenders verify lease terms and rental payment history.

DSCR loans work particularly well for occupied investment properties. The property’s rental income qualifies you without personal income verification.

You must honor existing lease terms after purchasing in most states.

How does an FHA non-occupant co-borrower work?

FHA allows family members to co-borrow even when not living in the property. Parents, siblings, or adult children can strengthen your application. Their income and credit factor into qualification.

Both parties share full mortgage responsibility. The non-occupant co-borrower must be a family member. They share ownership despite not occupying.

Removing them later requires refinancing in the occupying borrower’s name alone.

Can you get a mortgage with an ITIN instead of Social Security number?

Yes, ITIN mortgage programs serve borrowers without Social Security numbers. Two years of tax returns filed with your ITIN establish income. Pay stubs and bank statements prove financial capacity.

Expect 10-20% initial investment requirements. ITIN loan rates run 0.50-2.00% above conventional conforming rates.

Lenders experienced in ITIN programs help gather required alternative documentation.

What are portfolio loans and when do you need them?

Portfolio loans are held by lenders in their own portfolios. This provides flexibility for non-standard situations. Complex income documentation becomes manageable. Non-standard property types gain eligibility.

Portfolio lenders evaluate complete pictures rather than rigid checklists. One weakness doesn’t automatically disqualify your application.

Rates typically run 0.50-2.50% above conventional conforming rates.

How long after bankruptcy can you buy a home?

FHA allows purchasing two years after Chapter 7 discharge. Conventional loans typically require four years. Chapter 13 allows purchasing during active repayment with trustee approval.

Credit rebuilding strategies should begin immediately after discharge. Secured credit cards and small installment loans establish new positive history.

VA loans allow Veterans to qualify two years after discharge.

How do you refinance to remove an ex-spouse from the mortgage?

Refinancing in your name alone is the only removal method. The divorce decree doesn’t release mortgage obligation. You must qualify independently using only your income.

Co-borrowers can strengthen applications when solo qualification proves difficult. FHA allows non-occupant co-borrowers from family.

Refinancing should happen quickly after divorce to release the non-occupying spouse.

What are bank statement loan programs for self-employed borrowers?

Bank statement loans qualify you based on deposits rather than tax returns. Lenders analyze 12-24 months of business bank statements. This avoids explaining complex business deductions.

Bank statement programs require larger initial investments than conventional loans. Expect 10-20% minimums.

Rates run higher reflecting additional underwriting complexity and verification challenges.

Can you use FHA or VA loans for mixed-use properties?

Yes, if commercial space represents 25% or less of total square footage. You must occupy the residential portion as your primary residence. The commercial use can’t create safety hazards.

FHA and VA programs provide attractive financing for qualifying mixed-use properties. Low initial investment requirements make them accessible.

Income from commercial space can help with qualification calculations.

How much does flood insurance cost in high-risk zones?

Costs vary dramatically by location and flood zone designation. High-risk coastal areas might pay several thousand dollars annually. Inland moderate flood zones might pay several hundred.

Elevation certificates reduce costs if your home sits above base flood elevation. Flood mitigation improvements decrease premiums.

Shopping multiple insurance carriers finds the best pricing for your situation.

What if FEMA remaps and your property enters a flood zone?

You must add flood insurance even if your original mortgage didn’t require it. The lender will force-place expensive insurance if you don’t obtain coverage voluntarily.

Refinancing after remapping requires compliance with new flood zone designations. Grandfathering provisions might preserve lower rates.

Property owners receive notification before requirements begin.

Can foreign nationals refinance their U.S. property investments?

Yes, foreign national refinance programs exist for rate improvement and cash-out scenarios. Your payment history on the existing mortgage matters significantly. Updated income documentation and property valuation are required.

Foreign national refinance programs require similar documentation to purchase loans. Cash-out refinancing typically limits to 70-75% of property value.

Your track record of successful U.S. mortgage payments strengthens refinance applications.

Conclusion: Navigating Special Financing Successfully

Complex home buying situations require specialized knowledge and experienced guidance. The programs exist to solve these challenges. The key is identifying which solution matches your specific circumstances.

Don’t assume your situation disqualifies you from homeownership. Portfolio lenders evaluate complete pictures rather than rigid checklists. Compensating factors often overcome initial obstacles.

Working with mortgage professionals experienced in special financing makes the difference between approval and decline. They know which programs match which situations. They structure applications to maximize approval likelihood.

Start by clearly understanding your specific challenge. Is it title-related? Documentation-based? Property condition? Relationship-driven? Each category has targeted solutions.

Gathering documentation early in the process prevents delays. Special financing takes longer than standard programs. Building extra time into your timeline reduces stress.

Be prepared for higher initial investment requirements. Most special financing programs require 10-35% minimums. The equity cushion protects lenders accepting additional risk.

Expect interest rates 0.50-2.50% above conventional conforming rates. The premium reflects additional underwriting complexity. Strong compensating factors achieve pricing at the lower end.

Consider the long-term strategy beyond the initial purchase. Will you refinance into conventional programs later? Or will you keep specialized financing long-term? Planning your exit strategy from the beginning makes sense.

Your path to homeownership exists despite complex circumstances. Special financing programs provide legitimate solutions for real-world situations. Understanding these options empowers you to move forward confidently.

Ready to explore special financing solutions for your unique situation? Schedule a consultation with our experienced team. We’ll evaluate your specific circumstances and identify the optimal program structure.

Get pre-qualified today to understand your options. Our specialized underwriting team handles complex situations daily. Your unique challenge has a solution—let’s find it together.

Related Resources

Special Financing Loan Programs

- Portfolio Loan Programs – Flexible financing for complex situations

- Foreign National Loans – U.S. property financing without SSN

- ITIN Loan Programs – Mortgage approval without Social Security

- Bridge Loan Solutions – Temporary financing during transitions

- Hard Money Loans – Quick-close asset-based financing

- FHA Loan Programs – Government-backed flexible qualification

- FHA 203k Renovation Loans – Purchase plus rehabilitation financing

- Bank Statement Loans – Self-employed alternative documentation

- Non-Warrantable Condo Loans – Financing for non-standard condominiums

- DSCR Loan Programs – Investment property cash flow qualification

- VA Loan Programs – Veterans benefits for special situations

- Conventional Loan Options – Standard programs for comparison

Specialized Calculators

- Foreign National Loan Calculator – International buyer payment estimates

- ITIN Loan Calculator – Non-SSN borrower calculations

- Bridge Loan Calculator – Temporary financing costs

- Bank Statement Loan Calculator – Self-employed payment projections

- DSCR Loan Calculator – Investment property qualification

- FHA Loan Calculator – Government program estimates

- Non-Warrantable Condo Calculator – Special condo financing

Relevant Case Studies

- Foreign National Purchase Success – International buyer closing

- Foreign National Refinance Story – Overseas investor equity access

- ITIN Loan Approval – Non-SSN homeownership achieved

- DSCR Investment Purchase – Complex income qualification

- FHA 203k Renovation Success – Fixer-upper transformation

- Portfolio Loan Solution – Non-standard approval