Condotel and Non-Warrantable Condo Loans Explained

By

Jim Blackburn

on

Tags: Blog Posts for - Emails 1-10

Not all condos are created equal—and not all are eligible for traditional financing.

If you’re looking at a condotel, resort unit, or a condo with too many short-term rentals or investor-owned units, you may be told it’s “non-warrantable.” That’s not a deal-breaker. It just means you need a specialized loan designed for these unique properties.

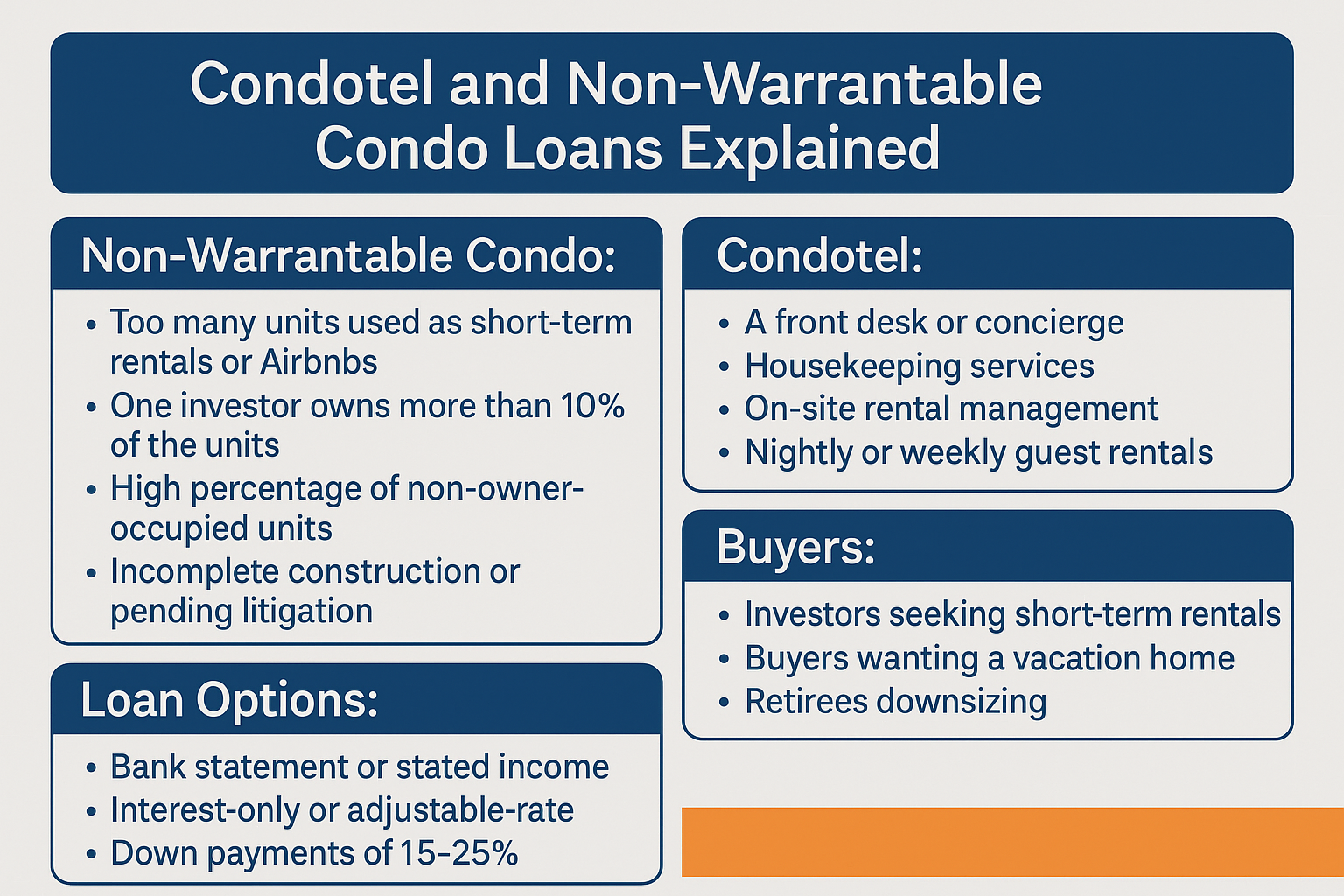

What Is a Non-Warrantable Condo?

A condo is considered non-warrantable if it doesn’t meet conventional lending guidelines from Fannie Mae or Freddie Mac.

Common reasons include:

Too many units used as short-term rentals or Airbnbs

One investor owns more than 10% of the units

High percentage of non-owner-occupied units

Incomplete construction or pending litigation

Low budget reserves or deferred maintenance

What Is a Condotel?

A condotel is a condo located in a building that functions like a hotel. It often includes:

A front desk or concierge

Housekeeping services

On-site rental management

Nightly or weekly guest rentals

Traditional lenders see this as a commercial risk, so they decline financing—even when the unit is individually owned.

Loan Options for Non-Warrantable Condos and Condotels

This is where portfolio and non-QM loans step in.

Available programs may include:

Bank statement or stated income loans

Asset-based qualification options

Interest-only or adjustable-rate terms

Down payment requirements as low as 15–25%

Available for primary, secondary, or investment use

These loans are manually underwritten by lenders that specialize in unique condo projects.

Who Buys These Properties?

Investors looking for cash-flowing short-term rentals

Buyers wanting a vacation home that can also earn income

Retirees downsizing into a low-maintenance lifestyle

Entrepreneurs entering the hospitality or rental business

Strategy: Know Before You Go Under Contract

Many buyers fall in love with a property, make an offer, and only then find out it’s non-warrantable. That’s when deals fall apart.

The smarter approach: work with a lender upfront who can verify the building’s status and offer loan options based on it.

Want to Know If Your Property Qualifies?

We Finance What the Banks Won’t

We work with lenders that go beyond cookie-cutter guidelines to help you close on high-performing, high-potential properties.

Ready to Take Your First Step?

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.