Balancing Education Savings and Down Payment Strategy for Young Families

Whether you’re a parent planning for your child’s future or a young adult mapping your own path, one question keeps coming up: Should you prioritize college savings or a home down payment? The answer isn’t either/or—it’s both, with the right strategy.

In this guide, you’ll discover:

- How to use down payment assistance programs to preserve college funds (according to HUD guidelines)

- Why buying a multi-unit property during college can eliminate housing costs (per FHA requirements)

- Strategic ways to balance educational goals with wealth-building through real estate (following CFPB consumer guidance)

- How families can leverage both goals simultaneously without sacrificing either

- Real scenarios where young buyers graduate with equity instead of debt

The key is understanding that these goals can work together—not compete against each other.

Questions about your situation? Schedule a call to speak with a loan advisor who understands family wealth-building strategies.

What’s the Real Cost of Choosing Only One?

Here’s what most families face: You save diligently for college, then realize you have nothing left for a down payment. Or you focus entirely on homeownership and watch your child graduate with substantial student debt.

The traditional approach creates an impossible choice. Families feel forced to pick between their child’s education and their family’s wealth-building foundation. But this false dichotomy has kept generations stuck in cycles of delayed homeownership and mounting debt.

What if there’s a third path? One where education and homeownership work together, where your college-age child can actually build equity while attending school, and where strategic planning lets you achieve both goals without sacrifice.

The families who break through aren’t doing anything magical. They’re simply applying different rules—rules that most people never learn because traditional financial advice keeps them separate.

Why the House Hacking Strategy Changes Everything

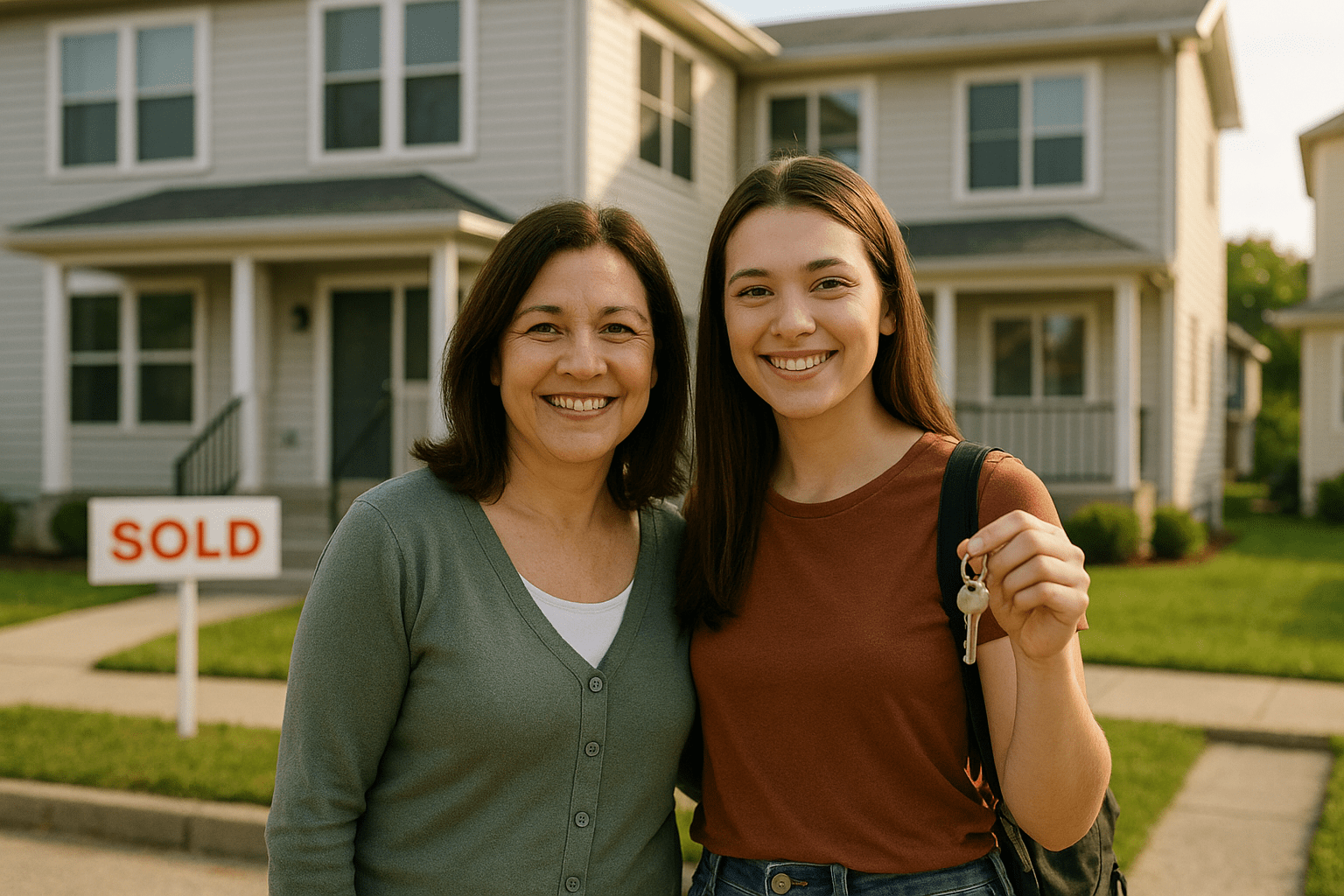

Imagine your child attends college living in a property you helped them purchase. They occupy one unit of a fourplex while renting the other three to fellow students. Their rental income covers most or all of the mortgage payment.

After four years, they graduate with:

- Zero rent payments made to landlords

- Substantial equity from appreciation and principal paydown

- Real-world experience as a property manager

- Tax advantages you used during their college years

- A potential asset to keep or sell

Compare this to the traditional path where they pay rent for four years and walk away with nothing but memories and debt.

This isn’t theoretical. The FHA loan program explicitly allows purchase of properties up to four units with minimal down payment requirements, making this strategy accessible to families at almost every income level.

Use the rental property calculator to run the numbers for your specific area and see how rental income can offset mortgage costs.

How Do You Qualify for Both Goals Simultaneously?

The qualification equation is simpler than most families realize. When you buy a multi-unit property where your child will live while attending college, rental income from the other units counts toward qualification in most programs.

Here’s how it typically works:

Loan Type Selection:

- FHA loans accept minimal down payments and flexible credit guidelines

- Conventional loans offer competitive terms for strong credit profiles

- Both allow multi-unit purchases with owner-occupancy

Income Qualification:

- Parent co-signers can support the application

- Projected rental income counts toward debt-to-income ratios

- Part-time employment and financial aid can contribute

- Gift funds from family are typically accepted

The Down Payment Balance: If you’ve saved for college, using a portion for a property down payment isn’t abandoning education—it’s funding it differently. Your child still attends school, but housing costs transform from expense to investment.

See how a physical therapist used an FHA loan case study to achieve homeownership with minimal funds, similar to what college-age buyers can accomplish with family support.

What About Using 529 Plans for Housing?

529 college savings plans offer surprising flexibility that most families don’t fully utilize. While these accounts are designed for qualified education expenses, housing costs on-campus qualify—but there’s a wealth-building alternative most families miss.

The traditional approach: Withdraw from your 529 to pay rent or dorm fees. The money disappears forever into someone else’s pocket.

The wealth-building approach: Use your 529 for tuition and qualified expenses while purchasing a multi-unit property that generates income to cover housing costs. Your education savings stay intact while real estate provides the housing solution.

If you need funds for a down payment, consider these strategies:

- Use non-529 savings first to preserve tax-advantaged education funds

- Explore down payment assistance programs to minimize cash requirements

- Consider parent co-signers to qualify with less money down

- Use gift funds from extended family for the down payment

The down payment assistance case study shows how a teacher purchased a home with grant funding, similar programs exist for first-time buyers in most markets.

How Do You Choose Which Goal Gets Priority?

The honest answer: It depends on your timeline and starting point. But here’s a framework that helps families make this decision strategically rather than emotionally.

If college is more than five years away:

- Build both savings simultaneously

- Focus slightly more on down payment funds (easier to access when needed)

- Establish credit foundation through authorized user strategies

- Explore markets near potential college locations

If college is two to four years away:

- Accelerate down payment savings for potential college-area purchase

- Research multi-unit availability near target schools

- Begin pre-qualification conversations

- Identify potential co-signer arrangements if needed

If your child is currently in college:

- It’s not too late—many students buy after freshman year

- Use accumulated financial aid refunds and part-time income

- Consider properties that work for remaining college years plus beyond

- Focus on areas with strong rental markets

If college isn’t part of the plan:

- Shift entirely to homeownership savings

- Consider house hacking even without student tenants

- Look at properties near employment centers or trade schools

- Build equity from day one rather than paying rent

Use the FHA loan calculator to model different purchase scenarios and see what fits your family’s financial situation.

What If You Need Down Payment Help from Retirement Accounts?

Some families discover their college savings are intact but they lack liquid funds for a down payment. Your retirement accounts might offer a bridge—but only with careful planning.

401(k) loans work differently than withdrawals:

- You borrow from yourself, not a lender

- No credit check affects your mortgage application

- Repayment goes back into your own account

- You avoid early withdrawal penalties

The strategic calculation: If borrowing from retirement helps your child purchase a multi-unit property that generates positive cash flow and builds equity, you’re not sacrificing retirement—you’re diversifying wealth-building across generations.

Alternative approaches include:

- Conventional loan programs with minimal down payment options

- Gift funds from extended family members

- Down payment assistance in your target market

- Delaying purchase until you’ve saved sufficiently

The conventional loan case study demonstrates how a physical therapist purchased with traditional financing, showing this path works for families with different financial situations.

What About Properties That Need Work?

If you’re balancing education costs with home purchase, buying a fixer-upper might seem impossible. But renovation financing programs actually make this strategy more accessible, not less.

Why renovation properties work for this strategy:

- Lower purchase prices free up cash for other goals

- Rental rates based on updated condition, not purchase price

- Equity built through improvements, not just market appreciation

- Students can learn valuable skills through renovation process

The financing approach: The FHA 203k loan combines purchase price and renovation costs into one mortgage. This means your down payment requirement is based on the lower purchase price, not the higher after-repair value.

Strategic renovation timing:

- Purchase before school starts with cosmetic updates only

- Complete major renovations during summer breaks

- Engage student tenants in minor improvements for rent credits

- Build sweat equity while building real equity

Review this FHA 203k case study showing how a medical technician transformed a fixer-upper, similar to what families can accomplish with college properties.

What Happens After College Graduation?

Here’s where the dual-goal strategy proves its worth. When your child graduates, they face a decision point that their rent-paying peers never get.

Option 1: Keep the Property

- Continue renting all units while living elsewhere

- Property becomes long-term investment generating passive income

- Build wealth through rental cash flow and appreciation

- Establish credit history and landlord experience

Option 2: Live in One Unit

- Continue generating rental income from other units

- Reduce personal housing costs below market rates

- Build equity while starting career

- Refinance later with conventional loan refinance options

Option 3: Sell the Property

- Access accumulated equity for next investment or goal

- Use profits tax-efficiently based on ownership duration

- Leverage gains into different property or location

- Demonstrate mortgage payment history for next purchase

The critical difference: Their rent-paying peers have none of these options. They leave college with only debt and diploma, starting from zero on wealth-building.

Use the conventional loan refinance calculator to explore options for optimizing the property after graduation.

How Does This Strategy Affect Future Financial Aid?

This is the question that stops many families from pursuing the college property strategy. Let’s address it directly.

Property ownership impact on FAFSA:

- Investment properties do count as assets on financial aid applications

- Primary residences do not count (student must occupy the property)

- Rental income counts as income (but mortgage payments offset this)

- Net impact varies significantly by individual situation

Strategic considerations:

- Purchase in parent’s name to potentially minimize student asset impact

- Timing of purchase relative to FAFSA filing years matters

- Some families find the wealth-building benefit outweighs aid reduction

- Professional financial aid advisors can model specific scenarios

The bigger picture: If reduced financial aid eligibility means taking slightly less in grants but graduating with substantial equity and no rent expense over four years, many families find this trade-off strongly positive.

Bottom line: Don’t let financial aid fears prevent you from running the numbers on what could be a transformational wealth-building strategy.

What About Cash Flow During College Years?

The monthly cash flow equation determines whether this strategy succeeds or struggles. Here’s how to think about the numbers strategically.

Positive Cash Flow Properties:

- Rental income exceeds all property expenses

- Property pays for itself from day one

- Extra income can fund other education expenses

- Minimal financial stress on family budget

Break-Even Properties:

- Rental income covers mortgage, insurance, taxes

- Family handles maintenance and occasional vacancies

- No additional monthly cost compared to paying rent elsewhere

- Building equity without ongoing expense

Slightly Negative Cash Flow:

- Rental income falls short of all expenses by small amount

- Family covers gap (often less than traditional dorm costs)

- Equity building and tax benefits offset modest monthly cost

- Still far superior to paying full rent with no return

Use the rental property calculator to project cash flow for properties you’re considering and see which category fits your potential purchase.

The key insight: Even properties requiring modest monthly contributions typically cost less than paying full rent while building substantial equity over the college years.

How Stairway Mortgage Helps Families Balance Both Goals

We understand that education and homeownership aren’t competing priorities—they’re complementary paths to family wealth. Our approach helps families achieve both without sacrificing either.

Our process for families balancing these goals:

Discovery Phase:

- Assess your current college savings and down payment funds

- Evaluate qualification potential for multi-unit properties

- Review timeline relative to college start dates

- Discuss family goals for both education and real estate

Strategy Development:

- Model multiple scenarios with different loan programs

- Calculate cash flow projections for specific properties

- Identify optimal timing for purchase relative to school years

- Explore down payment assistance and family gift options

Implementation Support:

- Connect you with realtors experienced in college-area investment properties

- Coordinate qualification including student occupancy and rental income

- Structure financing to maximize both educational and investment goals

- Guide you through closing process with clear timeline

Ongoing Guidance:

- Discuss strategies for property management during college years

- Review options for post-graduation decisions

- Support refinancing or additional purchases as appropriate

- Help you build wealth through education and real estate simultaneously

Ready to explore how your family can achieve both educational and homeownership goals? Schedule a call with our team to discuss your specific situation.

Ready to Stop Choosing Between Your Goals?

You’ve seen how families balance college savings and home down payments successfully. The question isn’t whether it’s possible—it’s whether you’re ready to take action.

Your next steps:

- Run Your Numbers: Use our calculators to see what’s possible in your target college area

- Assess Qualification: Understand how you’d qualify with current income, savings, and credit

- Research Markets: Explore multi-unit availability near target colleges

- Get Pre-Qualified: Know your buying power before your child’s college search

Different paths work for different families:

- Some start with property purchase, then fund remaining education costs from cash flow

- Others prioritize education, then use graduate’s income to qualify for property

- Many find creative combinations that achieve both goals simultaneously

The families who succeed aren’t the ones with the most money. They’re the ones who see possibilities others miss and take action while others wait.

Get pre-approved to understand your options, or take our discovery quiz to see which strategy fits your situation best.

Frequently Asked Questions

Can you really buy a multi-unit property with minimal down payment?

Yes, FHA loans allow purchase of properties up to four units with down payments as low as the program minimum when one unit will be owner-occupied. This makes multi-unit house hacking accessible to families who might assume they can’t afford investment properties. The key is that your college-age child must actually live in one of the units.

Does rental income count toward mortgage qualification?

Absolutely. When purchasing a multi-unit property where you’ll occupy one unit, lenders typically count a percentage of projected rental income from the other units toward your qualification. This is especially helpful for college-age buyers who may have limited personal income but can demonstrate strong rental potential in student housing markets.

What if my child transfers schools or drops out?

This is a legitimate concern. Many families structure these purchases with contingency plans: the property works as a rental investment even if the student isn’t living there, other family members could occupy the property, or the property could be sold. The conventional loan refinance option also exists to restructure the loan if occupancy situations change. The key is buying in markets with strong fundamentals beyond just student demand.

How does this compare to just paying rent and keeping money in investments?

The comparison depends on your specific situation, but most families find that real estate purchased in strong college markets outperforms keeping funds in traditional investments while paying rent. You’re getting housing plus appreciation plus equity building plus tax benefits plus education in property management. The rent-and-invest approach provides only investment returns while housing costs disappear forever. Use the rental property calculator to see the specific comparison for your situation.

What credit score do we need for this strategy?

Credit requirements vary by loan program, but FHA loans work with lower credit scores than conventional loans, making them accessible to more families. If the student is young and has limited credit history, parent co-signers with established credit can typically support the application. The earlier you start building the student’s credit through authorized user status, the more options you’ll have.

Also Helpful for Smart Stewards

Related Resources:

- All Available Loan Programs – Explore financing options for your situation

- FHA 203k Renovation Loans – Buy and improve college properties

- Down Payment Assistance – Preserve college savings with grant programs

What’s Next in Your Journey?

Continue building your smart steward strategy with these guides:

- Building Credit Foundation Early (Post #1)

- Authorized User Strategy Guide (Post #2)

- First Home Purchase Planning (Post #4)

Explore Your Complete Options

Calculate Your Scenarios:

- FHA Loan Calculator – Model college property purchases

- Rental Property Calculator – Project cash flow and returns

- All Calculators – Explore every scenario

See Real Success Stories:

- FHA Loan Success Story – Physical therapist’s first home

- Down Payment Assistance Story – Teacher used grants

- All Case Studies – Browse every journey

Ready to Take Action:

- Schedule a Call – Discuss your family’s goals

- Discovery Quiz – Find your best path

- Get Pre-Approved – Know your buying power