Traditional mortgage underwriting relies heavily on tax returns, pay stubs, and employment verification to assess your ability to repay. But what if your financial situation doesn’t fit these standard documentation requirements? No doc loans provide pathways to homeownership and refinancing for borrowers with complex income structures, substantial assets, privacy preferences, or non-traditional employment situations. Understanding how alternative documentation works, what lenders actually verify, and how to position yourself for approval helps you access mortgage financing that aligns with your unique financial profile rather than forcing you into conventional qualification boxes.

Ready to explore your options? Schedule a call with a loan advisor.

A no doc loan is a mortgage that uses alternative verification methods instead of traditional income documentation like tax returns and pay stubs. Despite the name, these programs aren’t truly “no documentation”—they simply verify your financial capacity through different means such as bank statement analysis, asset evaluation, or property cash flow rather than relying on W-2s and tax returns that many borrowers find problematic.

How do modern no doc loans differ from pre-financial crisis stated income loans? Today’s alternative documentation programs maintain responsible lending standards by verifying repayment capacity through bank deposits, asset holdings, or investment property cash flow—unlike pre-2008 stated income loans that literally took borrowers at their word without meaningful verification, creating the loan quality issues that contributed to the housing crisis.

The evolution reflects important regulatory changes. The Dodd-Frank Act and Ability-to-Repay rules established that lenders must verify a borrower’s capacity to repay mortgages. Modern no doc programs comply by using alternative verification that still demonstrates financial capacity, just through different documentation than conventional lending requires.

Several structures provide alternatives to traditional documentation:

Are no doc loans more expensive than traditional mortgages? Alternative documentation programs typically carry pricing premiums and require stronger compensating factors like larger equity contributions, higher credit scores, or substantial reserves—the reduced documentation increases lender risk, reflected in program terms.

Modern no doc programs operate within regulatory frameworks:

The key distinction: responsible alternative documentation versus the truly no-verification stated income programs that disappeared after the financial crisis.

Who should consider no doc loan programs? These programs serve specific borrower profiles where traditional documentation creates barriers despite strong financial capacity—self-employed individuals with tax deductions reducing reported income, business owners with complex structures, investors with property portfolios, retirees living on assets, and high-net-worth individuals prioritizing privacy.

Understanding whether your situation aligns with alternative documentation helps you pursue appropriate programs rather than struggling with conventional lending that doesn’t fit your financial profile.

Traditional underwriting creates challenges for entrepreneurs:

Why do self-employed borrowers struggle with conventional mortgages? Traditional lending calculates income from tax returns after accounting for business deductions—tax strategies that legitimately minimize taxable income also reduce the income lenders use for qualification, creating situations where successful business owners can’t qualify for mortgages despite strong cash flow.

Alternative documentation solves this disconnect:

Self-employed scenarios benefiting from no doc programs:

See how other borrowers have successfully used no-doc financing:

Calculate your no-doc loan scenarios:

Investors with property portfolios face unique documentation challenges:

How do multiple properties complicate traditional mortgage qualification? Each rental property’s mortgage payment counts against your debt-to-income ratio even if properties cash flow positively—lenders may discount rental income significantly or disallow it entirely without extensive documentation, making it progressively harder to acquire additional properties through conventional financing.

No doc solutions for investors:

Investor situations benefiting from alternative documentation:

Explore investor-focused programs:

Wealth doesn’t always translate to qualifying income:

Can retirees with substantial assets struggle to qualify for mortgages? Yes, traditional lending focuses on monthly income streams—retirees living on investment portfolios, drawing minimal distributions to manage taxes, or those between retirement and Social Security eligibility may have limited “qualifying income” despite substantial net worth.

Asset-based solutions address this disconnect:

High-net-worth scenarios benefiting from no doc programs:

Explore asset-focused qualification:

What are bank statement loans and how do they verify income? Bank statement programs analyze deposit patterns in your business or personal bank accounts over recent months—typically 12 or 24 months—calculating average monthly income from consistent deposits and applying expense factors to account for business costs, resulting in qualifying income often exceeding tax return calculations.

This approach recognizes the reality that successful businesses generate cash flow shown through bank deposits regardless of how tax returns report income after deductions optimize tax liability.

Lenders follow systematic processes to derive qualifying income:

Why do bank statement loans apply expense factors? Your bank deposits include gross business revenue, but running your business costs money—the expense factor (25-50% depending on business type and program) accounts for business expenses you must pay from gross deposits, leaving the net amount available for personal obligations like your mortgage.

Programs accept different statement types:

Business bank statements:

Personal bank statements:

Mixed statement approach:

Bank statement loans require specific documentation beyond the statements:

What deposits require explanation in bank statement analysis? Large one-time deposits, transfers between accounts, gifts, loan proceeds, or any irregular deposits not representing business income need documented explanations—lenders want to verify qualifying income comes from sustainable business operations rather than one-time events.

What credit score do you need for no doc loan approval? Alternative documentation programs typically require higher credit scores than conventional mortgages—many programs establish minimums in the excellent range to offset the reduced income verification, though specific thresholds vary by lender, loan amount, and compensating factors like equity and reserves.

The reduced documentation increases lender risk, requiring compensating factors through other underwriting elements to maintain responsible lending standards.

No doc programs demand strong credit positioning:

How do recent credit issues affect no doc loan approval? Alternative documentation programs offer less flexibility for recent credit problems than conventional loans since they’re already accommodating reduced income verification—combining both alternative documentation and challenged credit typically exceeds most lenders’ risk tolerance.

Larger equity contributions offset documentation reduction:

Typical equity requirements:

Why do no doc loans require more equity? Larger borrower investment reduces lender risk exposure—if market conditions decline, greater equity cushion protects against loss, while substantial borrower investment also demonstrates financial commitment and capacity.

Benefits of larger equity contributions:

Substantial liquid reserves are critical for no doc approval:

Minimum reserve expectations:

What assets count toward no doc loan reserves? Checking accounts, savings accounts, money market funds, stocks, bonds, mutual funds in liquid brokerage accounts, and sometimes retirement accounts (potentially discounted) count toward reserves—illiquid assets like real estate equity, business interests, or collectibles typically don’t qualify.

Reserve calculation example:

How do asset-based no doc loans work? These programs qualify you based on liquid asset holdings rather than requiring income documentation—lenders evaluate whether your assets could theoretically service the mortgage over specific timeframes, creating qualification pathways for those with substantial wealth but limited traditional income.

Asset-based lending recognizes that significant liquid wealth demonstrates financial capacity regardless of monthly income streams shown on tax returns or pay stubs.

Lenders use various formulas to derive qualifying capacity from assets:

Asset depletion method:

Debt service coverage:

Percentage of assets:

How much in assets do you need for asset-based qualification? Requirements vary significantly by program and loan amount, but many asset-based programs require liquid assets substantially exceeding the loan amount—ratios of 2-4x the loan amount in qualifying assets occur commonly.

Not all assets receive equal treatment:

Full value assets:

Discounted assets (commonly 60-70% of value):

Typically excluded assets:

While eliminating income documentation, asset-based programs require comprehensive asset verification:

Do asset-based loans require explanation of wealth source? Many programs want to understand how you accumulated assets, particularly with very large holdings—this isn’t to judge but to verify assets come from legitimate sources and truly belong to you rather than being temporarily borrowed for qualification purposes.

Explore asset-based qualification:

What are DSCR no doc loans and how do they work? Debt Service Coverage Ratio loans for investment properties qualify you based on the property’s rental income covering its mortgage payment—your personal income doesn’t factor into qualification, making DSCR loans effectively “no doc” for personal income while focusing entirely on investment property cash flow.

This structure recognizes that well-selected investment properties should be self-sustaining regardless of the owner’s personal income situation.

The debt service coverage ratio measures whether rental income covers the mortgage:

DSCR formula: DSCR = Monthly Rental Income ÷ Monthly Mortgage Payment (PITI)

DSCR interpretation:

Minimum DSCR requirements:

How do lenders determine rental income for DSCR calculations? Most commonly through market rent appraisals where the property appraiser researches comparable rental properties and provides opinion of reasonable market rent for your property—alternatively, existing leases on occupied properties provide actual rental income verification.

Investment property financing without personal income documentation:

Can you use DSCR loans for your first investment property? Yes, DSCR programs don’t typically require previous investment property experience, though lenders may adjust terms or requirements for first-time investors—the focus remains on whether the specific property’s income covers its debt service.

While eliminating personal income documentation, DSCR loans require property-specific verification:

Explore DSCR investment property financing:

Calculate DSCR scenarios:

Can you use no doc loans for any property type? Most alternative documentation programs finance a wide range of property types including single-family homes, condos, townhomes, and 2-4 unit properties, though specific programs have preferences—DSCR loans focus on investment properties while bank statement and asset-based programs typically serve primary residences, second homes, and investment properties.

Understanding program-specific property and purpose preferences helps you pursue appropriate financing for your situation.

Different programs accommodate various property types:

Primary residences:

Second homes:

Investment properties:

Multi-unit properties (2-4 units):

Condos and townhomes:

Can you use no doc loans for unique or luxury properties? Yes, alternative documentation programs often work well for high-value or unique properties that might challenge conventional lending—portfolio lenders providing no doc options frequently have experience with luxury real estate and can accommodate properties exceeding conforming loan limits.

No doc programs serve various financing needs:

Purchase transactions:

Rate-and-term refinances:

Cash-out refinances:

How much equity can you extract with no doc cash-out refinancing? Cash-out refinance loan-to-value limits vary by program but typically range more conservatively than conventional lending—expect maximum LTV ratios that require you to maintain substantial equity positions after extracting cash.

Considering a refinance? Submit a refinance inquiry to see if this makes sense for you.

How can you maximize approval odds for no doc loans? Strong positioning through excellent credit management, substantial equity contributions, significant reserve accumulation, clear bank deposit patterns, and professional documentation presentation dramatically improve approval likelihood—alternative documentation doesn’t mean relaxed standards, but rather different evaluation criteria requiring strategic preparation.

Thoughtful application preparation demonstrates financial sophistication and repayment capacity even without traditional income documentation.

Perfect your credit before applying:

How far in advance should you optimize credit for no doc loan application? Begin credit optimization 6-12 months before your anticipated application—this timeframe allows late payments to age off consideration, gives you time to pay down balances, lets you dispute errors thoroughly, and permits your credit profile to stabilize after any improvements.

If pursuing bank statement loans, prepare your accounts strategically:

Can you improve bank statement loan qualification by changing deposit patterns? While you shouldn’t artificially manipulate finances, legitimately depositing all business revenue through proper business accounts and maintaining consistent patterns does improve how lenders analyze your income—start these practices well before applying rather than making sudden changes right before application.

Build substantial liquid reserves:

How much should you have in reserves for no doc loan approval? Target 12-24 months of total housing payments in liquid reserves after your down payment and closing costs—this substantial cushion demonstrates financial capacity and addresses lender concerns about reduced income documentation.

Organize your application professionally:

Professional presentation signals that you’re serious, organized, and financially sophisticated—these impressions matter significantly when underwriters evaluate applications with alternative documentation.

Are no doc loans legal in today’s mortgage market? Yes, alternative documentation programs operate legally within current regulatory frameworks by verifying repayment capacity through alternative means that comply with Ability-to-Repay requirements—modern no doc loans maintain responsible lending standards while accommodating borrowers whose income doesn’t fit traditional documentation methods.

The key distinction from problematic pre-crisis lending:

Are no doc loans safe for borrowers? Yes, when pursued appropriately for situations where they fit—borrowers should ensure they can truly afford the mortgage payment based on their actual financial situation regardless of what documentation shows, maintain adequate reserves for emergencies, understand the terms and costs, and work with reputable lenders following responsible underwriting practices.

Yes, no doc loans can be refinanced through conventional or other alternative documentation programs when circumstances change or market conditions create opportunities—the existing no doc loan doesn’t prevent future refinancing, though you’ll need to qualify under whatever program you choose for the refinance based on requirements at that time.

Should you plan to refinance your no doc loan to conventional financing later? This strategy works well if you anticipate your documentation situation improving—for example, self-employed borrowers might take no doc loans initially then refinance to conventional terms after establishing two years of tax returns showing adequate income, or retirees might refinance once Social Security creates qualifying income streams.

Refinance planning considerations:

No doc loan timelines vary based on loan complexity and documentation completeness, but typically align with or slightly exceed conventional mortgage timelines—expect 30-45 days for straightforward transactions, though complex situations or unique properties may require longer, while well-prepared applications with complete documentation can sometimes close faster.

What factors affect no doc loan closing speed?

Expedite your closing:

Yes, foreign national programs provide no doc financing for non-U.S. citizens purchasing U.S. real estate without requiring U.S. income, credit history, or employment—these programs focus on property equity, foreign income and assets, and the property itself as collateral, making them effectively alternative documentation for international buyers.

What do foreign nationals need for no doc loan approval? Valid passport and visa documentation, foreign income verification (often simplified compared to U.S. requirements), foreign bank statements showing financial capacity, substantial equity contributions (typically larger than U.S. citizen requirements), U.S. tax identification number (ITIN), proof of funds for down payment, and sometimes U.S. bank account establishment.

Foreign national considerations:

No, alternative documentation programs come primarily from portfolio lenders, non-QM specialists, and private lenders rather than being widely available across all mortgage lenders—many large retail mortgage companies focus exclusively on conforming loans that can be sold to Fannie Mae or Freddie Mac, while smaller portfolio lenders and specialty lenders provide most no doc programs.

How do you find lenders offering no doc loans? Work with mortgage brokers who have access to multiple no doc lenders, research portfolio lenders in your market that hold loans on their balance sheets, explore non-QM lending specialists, connect with lenders serving self-employed borrowers or real estate investors, and ask for referrals from real estate attorneys, CPAs, or other investors.

Types of lenders offering no doc programs:

Are no doc loan costs significantly higher than conventional mortgages? Alternative documentation programs typically carry pricing premiums through higher interest rates, additional fees, or both—the reduced documentation increases lender risk, reflected in program costs, though exact pricing varies significantly based on your overall risk profile, equity contribution, credit score, and chosen program.

Understanding total costs across different no doc programs helps you select the most cost-effective option for your situation while weighing benefits against expenses.

No doc programs generally carry rate premiums:

What factors most affect your no doc loan interest rate? Credit score stands as the primary driver within most programs, with larger equity contributions, substantial reserves, strong bank deposit patterns, and program selection all materially impacting pricing—improving these factors before applying can shift you into better pricing tiers.

Alternative documentation may involve additional costs:

Are no doc loan closing costs substantially higher? Total closing costs depend on specific lender fee structures—while some no doc lenders charge premium fees, others maintain fee structures competitive with conventional lending, making lender comparison important for understanding total transaction costs.

Evaluate the complete cost picture:

When do no doc loan costs justify the expense? If alternative documentation enables purchasing a property that will appreciate significantly, accessing your current home’s equity for high-return investments, avoiding liquidation of well-performing assets, maintaining business operations without disruption, or acquiring cash-flowing investment properties that self-fund the premium costs through rental income.

Do all states allow no doc loans? While most states permit alternative documentation lending, specific program availability varies by state based on state-specific lending regulations, lender licensing, investor guidelines for purchasing these loans, and local market conditions—some states have more restrictive consumer protection laws affecting non-QM lending availability.

Additionally, certain property types or locations may face availability limitations regardless of state regulations.

Alternative documentation availability varies geographically:

What states have the best no doc loan availability? Generally states with strong real estate markets, significant self-employment populations, large investor communities, and active portfolio lending institutions—major markets in California, Florida, Texas, New York, and other populous states typically offer robust alternative documentation options.

Not all property locations receive equal treatment:

Preferred locations:

Challenging locations:

Can you get no doc loans for rural properties? Yes, though availability narrows and requirements may strengthen—rural property no doc financing typically requires larger equity contributions, may involve specialized lenders with rural expertise, could carry different pricing, and benefits from properties with income-generating potential like farms or ranches.

Why does lender selection matter more for no doc loans than conventional mortgages? Alternative documentation requires specialized expertise, different underwriting approaches, portfolio lending relationships, and experience navigating complex financial situations—working with lenders inexperienced in no doc programs leads to declined applications, unnecessary documentation requests, extended timelines, and potentially missing optimal programs for your situation.

Specialist lenders understand how to present and underwrite alternative documentation effectively.

Look for specific experience indicators:

How do mortgage brokers help with no doc loans? Experienced brokers maintain relationships with multiple no doc lenders and programs, can match your situation to optimal programs, understand various lender overlays and preferences, navigate complex underwriting requirements, and advocate on your behalf when issues arise—their multi-lender access proves particularly valuable in specialized lending.

Evaluate lenders through targeted questions:

Lenders with genuine expertise provide clear, confident answers demonstrating deep program knowledge.

Watch for concerning lender behaviors:

Should you get multiple no doc loan quotes? Yes, comparing terms across lenders reveals market pricing and helps identify optimal programs—however, timing applications strategically to minimize credit inquiries and working with experienced lenders who can pre-qualify you before formal applications prevents application denials affecting your credit profile.

If a no-doc loan isn’t the right fit, consider these alternatives:

Explore all 30+ loan programs to find your best option.

Not sure which program is right for you? Take our discovery quiz to find your path.

Consumer Financial Protection Bureau Ability-to-Repay Rule – Federal consumer protection agency explaining mortgage lending standards including Ability-to-Repay requirements that govern responsible alternative documentation lending practices.

Federal Trade Commission Mortgage Discrimination Information – FTC resource covering fair lending laws, discrimination protections, and borrower rights that apply equally to alternative documentation and conventional mortgage programs.

Mortgage Bankers Association Non-QM Lending Resources – National trade association providing research, market data, and industry perspective on non-qualified mortgage lending including alternative documentation programs and market trends.

National Association of Realtors Investment Property Resources – Real estate professional organization offering investment property data, market analysis, and resources relevant to investors using alternative documentation for property acquisition.

IRS Small Business and Self-Employed Tax Center – Official IRS resource for self-employed individuals explaining tax filing, business deductions, and income reporting that affects traditional mortgage qualification and drives need for alternative documentation.

U.S. Small Business Administration Business Resources – Federal agency supporting small businesses with educational resources, business planning tools, and financial management guidance helpful for self-employed borrowers navigating alternative documentation requirements.

Federal Reserve Consumer Credit and Mortgage Resources – Central bank educational materials explaining mortgage markets, interest rate factors, and economic conditions influencing both conventional and alternative documentation lending availability and pricing.

Need local expertise? Get introduced to trusted partners including loan officers, realtors, and contractors in your area.

Ready to get started? Apply now or schedule a call to discuss your situation.

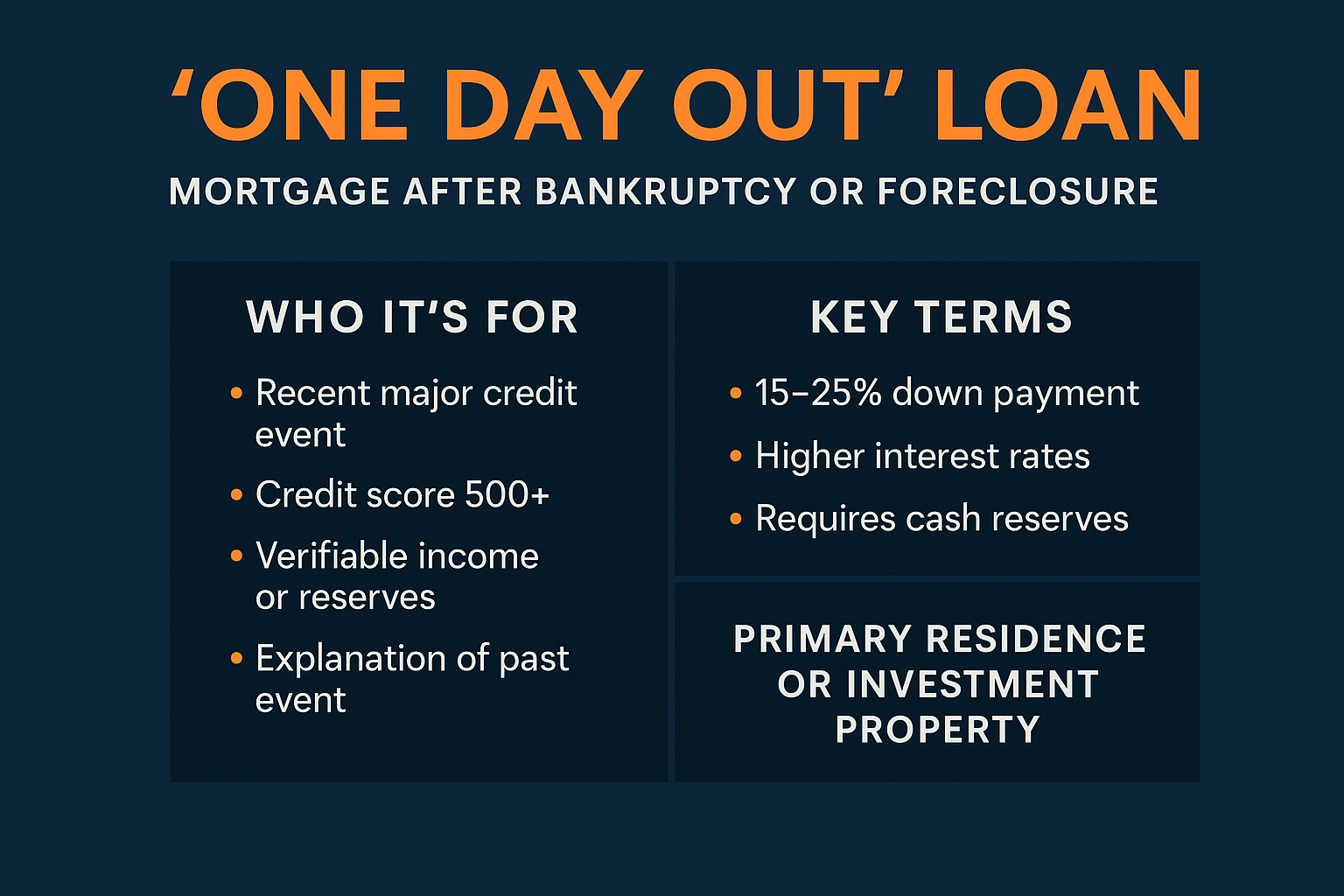

These loans come with stricter terms:

But the benefits are clear: you can stop renting, re-enter the market, and rebuild wealth while others are still waiting for their credit to recover.

Many buyers use this loan to purchase now, then refinance into a lower-rate, full-doc mortgage once they’ve met the conventional waiting periods and improved their credit.

This creates a bridge back into homeownership—without losing years to rent.

You’re not alone, and you’re not disqualified. We help buyers every day who’ve gone through what you have.

Let’s figure out what you qualify for and build a path forward.

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

Get program updates and rate insights in your inbox.