One of the most important decisions you’ll make when financing a home is choosing between a fixed-rate mortgage and an adjustable-rate mortgage (ARM).

And while one isn’t always “better” than the other, the right choice depends on your goals, timeline, and risk comfort — not just today’s rate.

Let’s break down how each one works, and when it makes sense to choose one over the other.

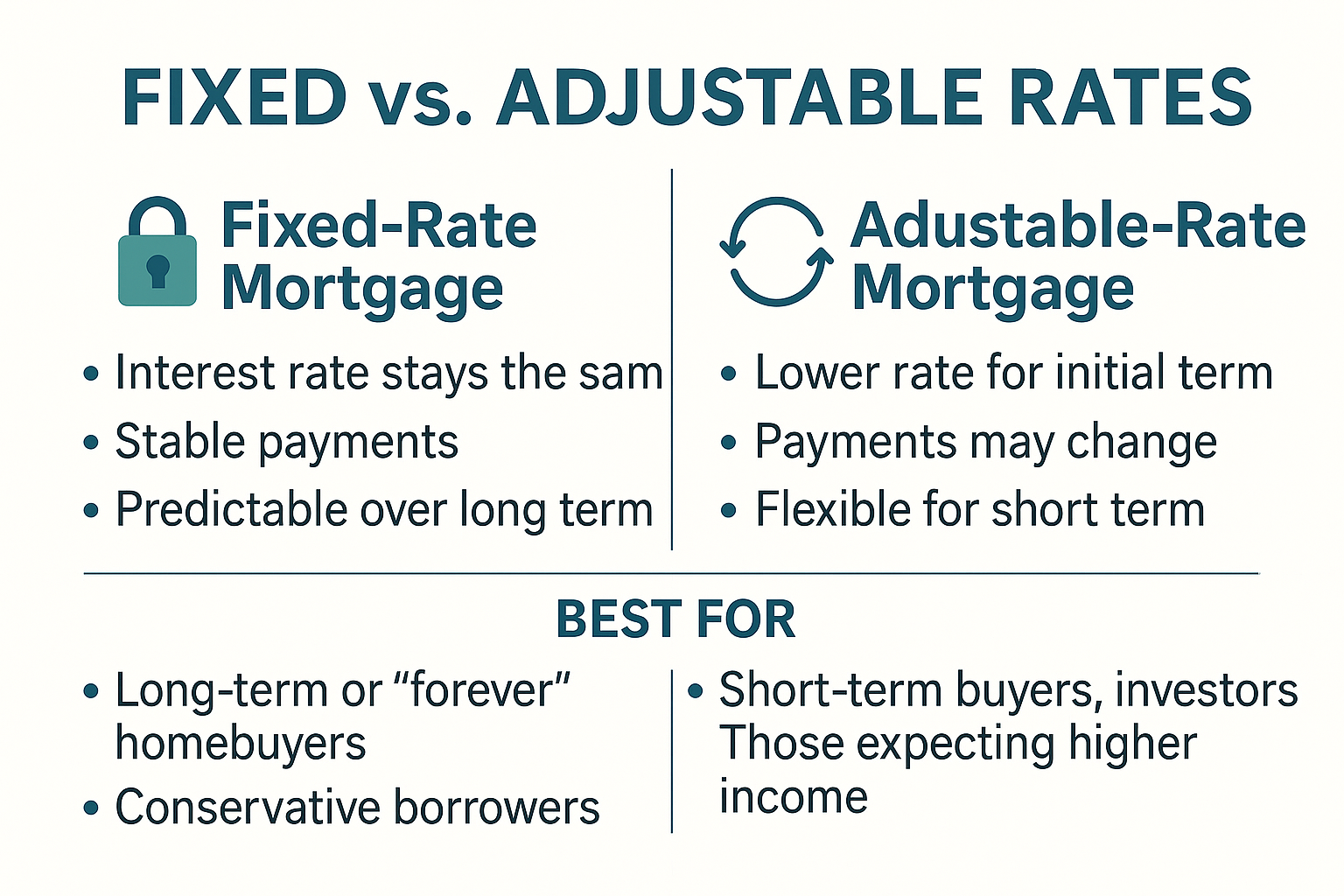

Fixed-Rate Mortgage: Stability First

A fixed-rate mortgage locks in your interest rate for the life of the loan (typically 15, 20, or 30 years). That means your monthly principal and interest payment never changes.

Best for:

Buyers planning to stay in the home 7+ years

People who prefer predictable payments

Times when rates are already low

Pros:

Stability = peace of mind

Easy to budget long-term

No surprises, even if market rates rise

Cons:

Usually a slightly higher rate than ARMs (at first)

Less flexibility if you plan to move or refinance soon

Adjustable-Rate Mortgage (ARM): Flexibility Now, Risk Later

An ARM starts with a lower interest rate for a set time (typically 5, 7, or 10 years), then adjusts annually based on the market.

Best for:

Buyers planning to sell, refinance, or relocate in 5–10 years

Investors looking to maximize cash flow early

People who are comfortable taking some risk for savings

Pros:

Lower rate up front = lower monthly payment

Can save thousands in the short-term

Good for “starter” homes or strategic moves

Cons:

Uncertainty after the fixed period ends

Payment may rise significantly if rates increase

Requires strategy — not set-it-and-forget-it.

Calculate your short-term savings with different loan structures using our loan calculators to see how much ARMs could save you during the initial fixed period.

So… Which One Should You Choose?

Ask yourself:

How long do I plan to stay in this home?

Is this my forever home or a stepping stone?

How much flexibility do I need vs. how much risk can I handle?

If you want security and plan to hold long-term, a fixed-rate loan might be best.

If you’re buying strategically, moving within 5–7 years, or expect income to increase, an ARM could save you money short-term — as long as you have a plan.

Use our Compare 2 Rates calculator to see the total interest difference between fixed and adjustable rate scenarios over your expected ownership timeline.

Bonus: You Can Refinance Either Way

Remember: Your first loan doesn’t have to be your last. Whether you choose fixed or adjustable today, you can always refinance later to lock in new terms.

We help clients run both short- and long-term projections to see which option builds more wealth over time.

Explore refinance options with our Conventional Refinance calculator to see how you could switch strategies later if your goals or the market changes.

Want to Choose the Right Rate Strategy for Your Timeline?

Fixed vs. adjustable isn’t about which is better—it’s about which fits your plan. Here’s how to decide:

📊 Compare total costs with our Compare 2 Rates calculator over your expected ownership period

🔄 Understand refinance flexibility with our Conventional Refinance calculator to see how you can adjust later

💰 Explore all rate structures at our loan calculators page to find what fits your strategy

Ready to Take Your First Step?

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.