Michael Johnson spent six months scrolling through Zillow and Redfin every evening after work. He was pre-approved, motivated, and ready to become a real estate investor. But every property he found either got snatched up within hours or was priced so high that the rental numbers didn’t work.

Sound familiar?

Michael was making the same mistake most first-time investors make: looking for off-market deals in the same place everyone else looks—online listing sites. The problem isn’t that MLS properties are bad. The problem is that by the time a property hits the MLS, you’re competing with dozens of other buyers, many of whom have more experience, better financing, or faster decision-making processes.

The breakthrough came when Michael’s coworker mentioned attending a local Real Estate Investment Association (REIA) meeting. That single suggestion changed everything. Within four months of committing to consistent networking, Michael secured an off-market deal that was $40,000 below market value—a property he would never have found online.

This case study breaks down exactly how Michael transformed from frustrated online browser to confident off-market deal buyer, including his month-by-month networking strategy, the relationships that led to his purchase, his complete financial analysis, and the lessons learned that you can apply to your own off-market deal search.

If you’re tired of losing bidding wars and watching overpriced properties sit on the MLS, Michael’s story shows there’s a better way. Get pre-approved before you start networking so you’re ready to act when off-market deals appear.

+

Client Profile:

The Six-Month Online Search:

Michael’s journey started like most first-time investors—with enthusiasm and online research. He read every blog post about real estate investing for beginners, watched YouTube videos about finding off-market deals, and set up alerts on every major real estate website.

“I had Zillow notifications going off on my phone multiple times daily,” Michael recalled. “I’d drop what I was doing to check new listings. But by the time I pulled comparable sales and ran the numbers, someone else was already writing an offer.”

Michael’s Online Search Results Over Six Months:

His two offers were both rejected immediately—one property had 14 competing offers, and the other went to a cash buyer willing to waive inspection.

“I realized I was playing a game I couldn’t win,” Michael said. “Online listings favor experienced investors who can analyze deals faster and cash buyers who can close quicker. I needed a different strategy.”

Three Core Problems Michael Faced:

Problem 1: Timing disadvantage

By the time a property appears on Zillow or Realtor.com, experienced local investors have already seen it through their agent networks. First-time investors are always 6-24 hours behind the curve when searching online.

Problem 2: Information overload without focus

Michael was looking at every property type in every Austin neighborhood. His criteria were too broad—”a good deal on a rental property”—which meant he was chasing properties that didn’t really fit his financial situation or investment goals.

Problem 3: No relationships with deal sources

The best off-market deals come from relationships with wholesalers, other investors, agents who specialize in investment properties, and property owners looking to sell without listing. Michael had none of these relationships.

“I realized the investors winning in Austin weren’t smarter than me,” Michael explained. “They just had access to off-market deals through relationships I didn’t have yet.”

Understanding how to find investment property requires shifting from online browsing to relationship-based deal sourcing—exactly what Michael discovered.

The Turning Point:

During a casual lunch conversation, Michael’s coworker David mentioned attending the Austin Real Estate Investment Association monthly meeting. “He said there were about 100 investors there every month, sharing strategies and talking about actual deals,” Michael recalled. “I thought it was worth checking out.”

That decision to attend his first REIA meeting became the catalyst that led to Michael’s first off-market deal.

Ready to start building your off-market deal network while securing financing? Schedule a call to discuss loan options that work for off-market purchases with quick closing timelines.

Michael attended his first REIA meeting in January with lowered expectations. “I thought it would be a bunch of gurus trying to sell $5,000 courses,” he admitted. “I almost didn’t go.”

But within the first 15 minutes, Michael realized this was different. The meeting featured an experienced local investor walking through a recent off-market deal—complete with actual numbers, photos of the property, and lessons learned from renovation challenges.

“Everyone was sharing real information,” Michael said. “People were talking about specific neighborhoods, lender recommendations, contractor horror stories, and properties coming on the market. It wasn’t theory—it was practical, local knowledge.”

What Michael Did Right from Meeting #1:

Strategy 1: Introduced himself honestly

Instead of pretending to have experience he didn’t have, Michael was upfront about being a first-time investor.

“I told people, ‘I’m Michael, I’m a software developer, and I own exactly zero rental properties,'” he recalled. “I expected people to dismiss me, but instead they were encouraging. Several investors told me their first property story and offered advice.”

This honesty made Michael memorable in a positive way. Experienced investors appreciated his authenticity and were more willing to help someone who acknowledged their beginner status rather than someone pretending to know more than they did.

Strategy 2: Asked specific, thoughtful questions

During the Q&A portion, Michael didn’t ask vague questions like “How do I get started?” Instead, he asked targeted questions based on his research:

“People want to help specific questions, not general confusion,” Michael said. “I did my homework before asking, so people knew I was serious.”

Strategy 3: Stayed for the entire networking hour

While many attendees left immediately after the formal presentation, Michael stayed for the full networking hour. He introduced himself to 8-10 people, collected business cards, and listened more than he talked.

“I made it a rule to introduce myself to at least 5 new people every meeting,” Michael explained. “I focused on listening to their stories and asking about their investing journey rather than immediately asking for deals.”

Strategy 4: Committed to attending every monthly meeting

This was Michael’s most important decision. After meeting #1, he blocked off every third Thursday evening on his calendar for the next six months—before even seeing results from networking.

“Most beginners attend one meeting, don’t find a deal that night, and never come back,” Michael said. “I committed to six months minimum regardless of immediate results. That consistency made all the difference.”

Meeting #1 Takeaways:

Michael left his first REIA meeting with:

“I didn’t find a property at meeting #1,” Michael said. “But I started building relationships that would eventually lead to my first off-market deal.”

By his second REIA meeting in February, Michael had a realization: everyone at these meetings was looking for off-market deals, but very few people were providing value to the community.

“I noticed people constantly asking ‘Does anyone have deals?’ but rarely offering anything helpful themselves,” Michael observed. “I realized if I wanted to stand out, I needed to give value before asking for anything in return.”

Michael’s Value-Creation Strategy:

Contribution 1: Volunteered technical skills

Michael approached the REIA president after the February meeting and offered to help redesign the association’s outdated website. As a software developer, this was easy for Michael but highly valuable to the organization.

“The website was from 2007 and looked terrible,” Michael said. “I offered to rebuild it using a modern template and set up an automated email system for meeting announcements. It took me about 10 hours over a weekend, but it made me memorable.”

The president introduced Michael to several experienced investors as “the guy who fixed our website,” creating instant credibility and goodwill.

Contribution 2: Connected people who could help each other

Michael started playing connector rather than just networker. When a property manager mentioned needing a new website, Michael introduced them to a web developer he’d met at the previous meeting. When a wholesaler asked about property management software, Michael shared research he’d done.

“I realized I could add value even as a beginner,” Michael explained. “I had tech skills, research abilities, and a growing network. Every time I connected two people who could help each other, both remembered me positively.”

This strategy—often called “giving to give” rather than “giving to get”—transformed how other investors perceived Michael. He wasn’t just another beginner asking for help; he was someone who contributed to the community.

Contribution 3: Shared detailed market research

Michael spent time each week researching Austin rental market trends, neighborhood appreciation rates, and property tax changes. At the March meeting, he shared a one-page summary of his findings with several investors.

“I wasn’t providing information they couldn’t find themselves,” Michael said. “But I was saving them time by synthesizing it. Several experienced investors told me they forwarded my research to their partners.”

The Relationship With David Begins:

At the March REIA meeting, Michael had his first substantive conversation with David Martinez, a 58-year-old investor who owned 15 rental properties throughout Austin.

“David asked me what I was looking for,” Michael recalled. “I started to say ‘a good deal on a rental property,’ but then I remembered that advice from meeting #1 about being specific. So I stopped myself and said ‘Actually, I don’t have a specific enough target yet. Could you help me think through my criteria?'”

This honest request for guidance—rather than vague deal-seeking—opened the door to a mentorship relationship that would eventually lead to Michael’s first off-market deal.

David spent 20 minutes asking Michael questions about his financial situation, risk tolerance, property management plans, and long-term investing goals. Then he helped Michael create a specific “buy box” of criteria for his first off-market deal search.

Michael’s Specific Buy Box (Developed With David’s Help):

Property characteristics:

Location parameters:

Financial criteria:

Seller situation:

“Once I had specific criteria written down, David said ‘Now I know what to look for on your behalf,'” Michael explained. “Vague criteria help nobody. Specific criteria make you memorable and make it easy for others to send you potential off-market deals.”

Michael created simple business cards with his buy box criteria, photo, and contact information. He handed these to every investor, agent, and wholesaler he met.

“The business card approach was genius,” Michael said. “People can’t remember everyone they meet, but they can save a card with specific criteria. Several people told me they kept my card and thought of me when properties came up.”

Understanding the complete investment property analysis framework helped Michael define realistic criteria for his first off-market deal.

With his specific buy box defined and business cards in circulation, Michael’s REIA networking started producing results—though not immediately in the way he expected.

Early Pipeline Activity:

Week 9: A wholesaler sent Michael an off-market deal that met his location criteria but was priced too high. Michael ran the numbers, determined it wouldn’t cash flow, and politely declined. “I explained why the numbers didn’t work at that price,” Michael said. “He appreciated the detailed analysis rather than just ‘not interested.'”

Week 10: An agent Michael met at REIA invited him to preview a property before listing. It was in Michael’s target area but needed $40,000 in renovations Michael wasn’t ready to handle. He passed but stayed in touch with the agent.

Week 11: David sent Michael an off-market deal in the right ZIP code. Property looked good initially, but when Michael drove by, he discovered it backed to a busy commercial street. “David didn’t know that detail,” Michael said. “I thanked him for thinking of me and explained what I learned. That gave him even better criteria for next time.”

Week 12: Another investor mentioned a property owner looking to sell a rental after his tenant moved out. Michael contacted the owner within 2 hours, ran analysis, but the seller’s price expectations were $50,000 above market value. “I shared my comparable sales analysis respectfully,” Michael said. “He thanked me but decided to list with an agent. I stayed friendly and told him to contact me if listing didn’t work out.”

The Pattern Michael Noticed:

“None of these were THE deal,” Michael explained. “But each one was practice. I was getting faster at running numbers, more confident evaluating properties, and better at building relationships even when deals didn’t work out.”

More importantly, Michael was demonstrating to his network that he was serious, responsive, and analytical. Every person who sent him a potential off-market deal received:

“This responsiveness set me apart,” Michael said. “Most beginners ghost after seeing a property that doesn’t work. I treated every opportunity as relationship building for the long term.”

April: The Call That Changed Everything

On April 3rd, Michael’s phone rang during his lunch break. It was David.

“I have a property that might be exactly what you’re looking for,” David said. “The owner contacted me directly about selling, but it’s too small for my portfolio—I only purchase properties above $500,000 now. Your name came to mind immediately because it matches your buy box perfectly.”

The Property Details:

Why This Off-Market Deal Came to David:

The property owner was relocating to California for work. He’d inherited the property from his parents five years earlier and rented it successfully to the same tenant since then. Now he needed to sell quickly without the complexity of MLS listing, agent coordination, showings, and uncertain timeline.

The seller’s brother knew David from a previous transaction two years earlier and suggested contacting him. “David could have easily wholesaled this off-market deal for a $15,000-$20,000 assignment fee,” Michael said. “Instead, he connected me directly with the seller because he remembered my specific criteria and I’d built trust by helping with the REIA website, making introductions, and sharing research.”

Michael’s Immediate Response:

Within 2 hours of David’s call, Michael had:

“I knew I had to move fast on off-market deals,” Michael said. “If I’d waited even a day to ‘think about it,’ another investor would have grabbed it.”

Within 24 hours, Michael had:

The Property Showing:

Michael toured the property the next evening. “It was even better than I expected,” he said. “The property was clean, well-maintained with good bones. Current tenant had taken excellent care of it. Minor cosmetic updates needed—fresh paint, maybe new carpet—but nothing major.”

The property included:

Michael asked the seller thoughtful questions:

“I wanted to understand his real motivations,” Michael said. “The answers told me this wasn’t someone trying to squeeze out maximum value—he needed certainty, speed, and simplicity more than the absolute highest price.”

The seller explained:

“Once I understood his situation, I knew I could structure an off-market deal that solved his problems beyond just offering a price,” Michael said.

[IMAGE 4 PLACEHOLDER]

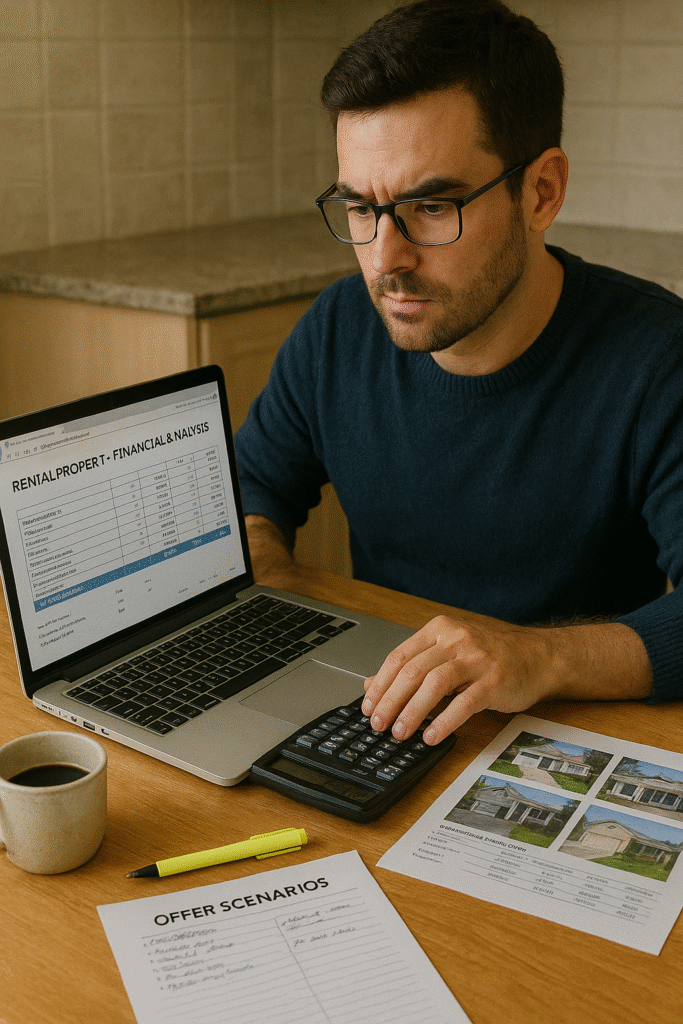

Before making any offer on the off-market deal, Michael spent two full evenings running comprehensive financial analysis. This wasn’t his first time analyzing a potential property—he’d evaluated several properties through REIA networking—but it was his first time analyzing a property he was seriously considering purchasing.

Step 1: Comparative Market Analysis

Michael pulled recent sales of similar properties to establish true market value. The seller had mentioned thinking the property was worth around $370,000 based on Zillow’s Zestimate.

Comparable Sales (Past 3 Months, Same Neighborhood):

1842 Maple Street:

2156 Oak Avenue:

1729 Pine Drive:

Average comparable sale price: $332,667

“The comps clearly showed the property was worth $330,000-$335,000 in current condition,” Michael explained. “Zillow’s $370,000 estimate was inflated—probably based on different property types or neighborhoods. I needed to show the seller real evidence, not just my opinion.”

Michael prepared a one-page comparable sales analysis showing:

“I wanted to have evidence ready when discussing price,” Michael said. “Not to be argumentative, but to have objective data supporting my offer.”

Step 2: Rental Income Analysis

The current tenant was paying $2,100 monthly. Michael needed to confirm whether this was below market, at market, or above market for rental income.

Comparable Rental Properties Currently Listed:

Similar properties in the area:

Average market rent range: $2,150-$2,250/month

“The current tenant was paying $2,100, which was $50-$150 below market,” Michael noted. “This meant I could increase rent to market rate when the lease renewed in 4 months, improving cash flow.”

Michael confirmed these rental rates with a property manager contact from REIA who managed 30 properties in the area. “She said $2,200-$2,250 was realistic for that property in good condition, and that similar properties rarely sat vacant more than 2-3 weeks.”

Step 3: Expense Projections

Michael created conservative expense estimates using information from his property manager contact, insurance quotes, and tax records:

Monthly Operating Expenses (Conservative Projections):

Property-specific expenses:

Management and maintenance reserves:

Capital expenditure reserve:

Total monthly expenses before financing cost: $880/month

“I used conservative assumptions because I’d rather be pleasantly surprised than financially stressed,” Michael explained. “The 6% maintenance reserve was high for a well-maintained newer property, but I wanted buffer as a first-time landlord.”

Step 4: Financing Cost Calculation

Michael’s lender had pre-approved him for a conventional investment property loan requiring 25% initial capital with good credit. His credit score of 742 qualified him for favorable terms.

Financing scenarios Michael modeled:

Scenario A: Purchase at $320,000

Scenario B: Purchase at $300,000

Scenario C: Purchase at $285,000

“I needed to figure out what purchase price would give me my target $300 minimum monthly cash flow,” Michael said.

Step 5: Cash Flow Analysis at Different Purchase Prices

Cash Flow Analysis: Purchase at $320,000

Monthly rental income: $2,100 (current rate)

Monthly expenses:

Monthly cash flow: -$361 (NEGATIVE)

“At $320,000, even with the current tenant paying rent, I’d be losing money every month,” Michael noted. “Not acceptable for my first property.”

Cash Flow Analysis: Purchase at $300,000

Monthly rental income: $2,225 (projected market rate after lease renewal)

Monthly expenses:

Monthly cash flow: -$137 (STILL NEGATIVE)

“Getting closer but still negative,” Michael said. “I needed the purchase price lower.”

Cash Flow Analysis: Purchase at $285,000

Monthly rental income: $2,225 (projected market rate)

Monthly expenses:

Monthly cash flow: -$63 (Nearly break-even)

“At $285,000 with market rent, I was almost cash flow positive using conservative assumptions,” Michael explained. “If actual maintenance came in lower than my 6% reserve—which was likely for a well-maintained newer property—I’d be positive. And I had room to increase rent modestly over time.”

Revised cash flow with 4.5% maintenance reserve (more realistic for newer property):

Monthly expenses:

Monthly cash flow: +$30 (POSITIVE)

“With more realistic maintenance assumptions, I had positive cash flow of $30 monthly at $285,000 purchase price,” Michael said. “Not spectacular, but it worked, and I knew I could improve it over time through rent increases and lower actual expenses.”

Step 6: Return on Investment Calculations

Michael calculated his target returns at different purchase prices to determine his maximum offer:

At $285,000 Purchase Price:

Initial capital required:

Annual cash flow: $360 (12 months × $30)

Cash-on-cash return: 0.48% (not including equity buildup, appreciation, or tax benefits)

“The cash-on-cash return looked low on paper,” Michael acknowledged. “But this analysis didn’t include three other profit centers: mortgage principal reduction, property appreciation, and tax benefits. Plus I valued the education from owning my first property.”

Complete return projection (5-year hold):

Year 1 returns:

“When I looked at all five profit centers—cash flow, equity buildup, appreciation, tax benefits, and leverage—the returns were excellent for a conservative, well-located property,” Michael said.

Step 7: Risk Assessment

Michael identified potential risks before making his offer on the off-market deal:

Risk 1: Tenant turnover – Current tenant could move out, requiring new tenant placement and potential vacancy.

Mitigation: Property in high-demand area, market rent competitive, property manager confirmed 2-3 week typical vacancy.

Risk 2: Major maintenance unexpected – Older properties can have surprise expensive repairs.

Mitigation: Thorough inspection, property well-maintained, major systems recently replaced, keeping healthy reserve fund.

Risk 3: Market downturn – Property values could decline, affecting refinance or sale options.

Mitigation: Buying below market value creates equity buffer, planning long-term hold regardless of short-term market fluctuations.

Risk 4: Rent decreases – Market rents could drop, affecting cash flow. Mitigation: Buying in strong school district with good employment drivers, conservative rent assumptions, positive cash flow even at current below-market rent eventually.

“I wasn’t looking for perfect,” Michael said. “I was looking for acceptable risk with good long-term potential. This off-market deal met that criteria.”

Use the rental property calculator to run similar scenarios when evaluating off-market deals.

Armed with comprehensive financial analysis and comparable sales data, Michael was ready to make his offer. But instead of leading with price, he first had an honest conversation with the seller about his situation and constraints.

Michael’s Pre-Offer Conversation:

Michael called the seller and said: “Before I present a formal offer, I want to make sure I understand your situation fully so I can structure something that works for both of us. Can you walk me through your ideal timeline and any concerns you have about selling?”

This question opened a 30-minute conversation where the seller revealed:

Seller’s Priorities (in order):

Seller’s Concerns:

“Once I understood his true priorities, I realized price wasn’t his primary concern,” Michael said. “He needed certainty and convenience more than maximum sale price. That’s when I knew I could structure an off-market deal that solved his problems.”

Michael’s Initial Offer Strategy:

Instead of starting at his target price of $285,000, Michael came in at $280,000 with several non-price terms designed to address the seller’s concerns:

Initial Offer Terms:

Purchase price: $280,000

Favorable non-price terms:

Estimated value to seller of non-price terms:

“I explained that my $280,000 offer was below his $370,000 expectation, but showed him the comparable sales data and emphasized the non-price benefits,” Michael said. “I wanted him to see the total package value, not just the number.”

Michael included his comparable sales analysis one-pager with the offer, showing the recent $328,000, $332,000, and $338,000 sales of similar properties.

The Seller’s Counter:

The seller took two days to consider (during which Michael nervously checked his phone every hour). Then he called with a counter-offer:

Seller Counter-Offer:

Purchase price: $305,000 (up from $280,000)

Counter-explanation:

“The seller said he appreciated the comparable sales analysis and understood $370,000 was too high,” Michael recalled. “But he felt $280,000 was below fair market value even accounting for the convenience. He countered at $305,000, which was still well below the $330,000-$338,000 comparable sales.”

Michael had two options:

Michael’s Second Offer Strategy:

Instead of meeting in the middle at $292,500, Michael made a strategic decision based on advice from David and his agent. He came back at $285,000 but enhanced the non-price terms:

Second Offer Terms:

Purchase price: $285,000 (up from $280,000 but below $305,000 counter)

Enhanced non-price terms:

“I realized the seller valued certainty and flexibility more than price,” Michael explained. “By giving him 45 days post-close occupancy instead of 30, I solved his housing transition problem completely. That was worth more to him than $20,000 in price.”

Why This Strategy Worked:

The extended occupancy gave the seller:

Michael’s total effective cost: $285,000 + $3,500 transaction costs + $2,000 repair cap = $290,500

Seller’s effective received value: $285,000 + $3,500 + $3,500 (avoided temporary housing) = $292,000 equivalent value

The Seller Accepted:

After one more day of consideration, the seller called Michael and accepted the $285,000 offer with enhanced terms.

“He told me three other investors had contacted him about the property but everyone just negotiated on price,” the seller explained. “You were the only one who asked about my situation and structured an offer that solved my actual problems. The extra 15 days of occupancy was the deciding factor.”

Final Agreement Terms:

Total effective cost to Michael: $290,500

Market value based on comps: $330,000-$338,000

Instant equity: $39,500-$47,500 (12-14% below market)

“This off-market deal worked because I understood the seller’s true priorities,” Michael said. “Win-win negotiation beats pure price haggling every time.”

Understanding buying first rental property with LLC considerations helped Michael structure the purchase correctly from the start.

Michael’s financing process was smooth because he’d done three critical things before finding his off-market deal:

Michael’s Financial Profile:

Credit and income:

Savings and reserves:

“I spent a year building my financial profile before ever searching for properties,” Michael explained. “Paid down credit cards, increased my credit score from 690 to 742, and saved aggressively. When this off-market deal appeared, I was ready.”

Conventional Investment Property Loan Details:

Michael qualified for a conventional investment property loan with favorable terms:

Financing structure:

Why the lender counted rental income:

Because the property had an existing tenant with a current lease agreement, the lender could include the rental income in Michael’s debt-to-income calculation. This made qualification easier.

“The lender used 75% of the monthly rent ($2,100 × 0.75 = $1,575) in my income calculation,” Michael explained. “This offset the new financing cost and made my debt-to-income ratio stay favorable even with the new property.”

Cash Required at Closing:

Breakdown of upfront capital needed:

Property-related:

Lender fees and reserves:

Total cash to close: $84,575

Michael used $75,000 from his saved investment capital plus $9,575 from his $20,000 reserves, leaving him with $10,425 in emergency reserves after closing.

“I wanted at least $10,000 remaining in reserves after closing as first-time landlord,” Michael said. “Keeping buffer was important for peace of mind.”

The Appraisal Process:

Michael’s biggest concern was the appraisal coming in below his $285,000 purchase price, which would require him to bring additional cash to close or renegotiate.

“I had comparable sales supporting $330,000+ value, but appraisers can be unpredictable,” Michael said. “I didn’t relax until I got the appraisal report.”

Appraisal Results:

The property appraised at $325,000 – significantly above Michael’s $285,000 purchase price.

The appraiser used the same three comparable sales Michael had researched ($328,000, $332,000, $338,000) and noted the subject property’s well-maintained condition and desirable location.

“That $325,000 appraisal created instant equity of $40,000,” Michael said. “I bought at $285,000, and it immediately appraised for $325,000. That’s equity I didn’t have to wait for through appreciation—it existed from day one because I negotiated an off-market deal below market value.”

Closing Timeline:

Day 1 (April 15): Offer accepted, both parties sign purchase agreement

Day 2-3: Michael orders inspection, submits financing application

Day 4: Appraisal ordered by lender Day 7: Inspection completed (minor items noted: worn weatherstripping on doors, slow-draining bathroom sink, loose handrail) Day 8: Michael and seller agree seller will fix inspection items before closing Day 12: Appraisal completed ($325,000 value)

Day 15: Final loan approval received (“clear to close”) Day 18: Final walkthrough confirms repairs completed Day 21 (May 6): Closing at title company

Total time from offer acceptance to closing: 21 days

“The process was smooth because I was prepared financially, the property was in good condition, and the seller was motivated to close quickly,” Michael said. “Having strong pre-approval before finding the off-market deal was critical.”

Understanding tax break for buying a house as investment property helped Michael plan for first-year tax benefits.

Michael closed on his off-market deal on May 6th and immediately began his journey as a rental property owner. Here’s what happened during his first 12 months:

Months 1-4 (May-August): The Learning Curve

The existing tenant stayed in place, which gave Michael valuable time to learn property management without immediate tenant placement pressure.

Month 1 (May):

“The first rent payment arriving on time was exciting,” Michael said. “Made it feel real.”

Month 2 (June):

Month 3 (July):

“July was the first month I experienced negative cash flow,” Michael said. “The maintenance items were minor but they added up. I reminded myself I’d conservatively budgeted for this.”

Month 4 (August):

Months 1-4 totals:

“The first four months taught me that property management wasn’t as scary as I’d feared,” Michael said. “The tenant communicated well, issues were minor, and I was building systems for tracking everything.”

Month 5 (September): First Rent Increase

When the tenant’s lease came up for renewal in September, Michael faced his first major decision: how much to increase rent without losing a good tenant.

Market analysis showed similar properties renting for $2,250-$2,300. The tenant was currently paying $2,100—below market by $150-$200.

“I didn’t want to shock the tenant with a huge increase,” Michael said. “They’d been excellent—paid on time, maintained the property well, communicated clearly. I wanted to balance market rent with tenant retention.”

Michael’s rent increase strategy:

He sent the tenant a lease renewal notice 60 days before expiration, proposing:

The tenant accepted immediately, appreciating the below-market rate and stability of a full-year lease.

Month 5-12 (September-April): Positive Cash Flow Achieved

With the new rent of $2,225/month, Michael’s cash flow improved significantly:

Revised monthly numbers after rent increase:

Monthly income: $2,225

Monthly expenses:

Total monthly expenses: $2,275

Monthly cash flow: -$50 (still slightly negative on paper)

“But my actual maintenance costs ran lower than projected,” Michael explained. “The property was well-maintained, and in months without maintenance I was significantly cash flow positive.”

Months 5-12 actual results:

Months 5-12 cash flow: +$389

Complete First Year Financial Summary:

Income:

Expenses:

Financing cost: $1,407 × 12 = $16,884

Property tax: $4,728 Insurance: $1,500 Actual maintenance: $1,335 Property management: $0 (self-managed) Vacancy: $0 (tenant stayed full year) CapEx reserve: $1,200 (set aside)

Total expenses: $25,647

First year cash flow: +$553

“Modest cash flow, but positive in year one,” Michael said. “For a first property focused on learning, this exceeded my expectations.”

Additional First-Year Returns:

Profit Center 1: Cash flow = $553

Profit Center 2: Equity buildup through mortgage principal reduction = $3,247

“Every financing cost includes principal and interest,” Michael explained. “The principal portion is forced savings—equity I’m building with the tenant’s rent.”

Profit Center 3: Property appreciation

Property values in Michael’s neighborhood increased approximately 4% during his first year of ownership.

“I didn’t cause this appreciation—the market did,” Michael acknowledged. “But I captured it by owning the property during a strong market year.”

Profit Center 4: Tax benefits

Michael worked with his CPA to understand first-year tax advantages:

Tax deductions claimed:

At Michael’s 24% marginal tax rate: $8,190 in tax savings

“These deductions lowered my overall tax liability significantly,” Michael said. “My CPA said rental real estate offers some of the best tax advantages available.”

Total First-Year Return Calculation:

Return on invested capital:

“When you look at all five profit centers together—cash flow, equity, appreciation, tax benefits, and leverage—the returns were incredible,” Michael said. “This off-market deal that took four months of relationship building produced a 77% first-year return.”

What Michael Learned About Managing His First Property:

Lesson 1: Communication prevents problems

Michael sent his tenant a friendly check-in email every quarter asking if anything needed attention. “Proactive communication meant small issues got handled before becoming expensive problems,” he said.

Lesson 2: Quality tenants are worth below-market rent

“When I calculate what tenant turnover costs—vacancy, cleaning, repairs, advertising, screening, showing—keeping a good tenant at $25 below market rent is great business,” Michael explained.

Lesson 3: Conservative budgeting reduces stress

Because Michael budgeted conservatively for maintenance, when actual costs ran lower, he felt like he was winning. “If I’d budgeted optimistically and costs ran higher, I’d have been stressed,” he said.

Lesson 4: Systems beat motivation

Michael created simple systems for rent collection (automated), maintenance tracking (spreadsheet), and expense recording (property management software). “Systems meant I didn’t have to remember everything—it was documented,” he said.

Lesson 5: Self-management teaches valuable skills

“Managing my first property myself taught me what good property management looks like,” Michael said. “When I eventually hire a manager for future properties, I’ll know what questions to ask and what standards to expect.”

Understanding long term rental vs short term rental strategies helped Michael confirm his long-term rental approach was right for his first off-market deal.

After successfully purchasing, managing, and profiting from his first off-market deal, Michael reflected on the key lessons that transformed him from frustrated online browser to confident investor:

Lesson 1: Relationships Trump Algorithms Every Time

“I spent six months searching online and found nothing,” Michael said. “I spent four months networking at REIA and got an off-market deal $40,000 below market value. Personal relationships beat technology for off-market deal sourcing.”

Why relationships matter more than online searching:

Michael’s relationship-building approach:

“I didn’t network transactionally,” Michael explained. “I wasn’t asking ‘Got any deals?’ every conversation. I was building genuine relationships by providing value, staying consistent, and being someone people wanted to help.”

Lesson 2: Provide Value Before Asking for Help

The breakthrough moment in Michael’s networking came when he stopped just attending meetings and started contributing to the community.

“When I volunteered to redesign the REIA website, I wasn’t thinking ‘This will get me deals,'” Michael said. “I was thinking ‘I have skills that can help this community.’ But that value-first approach made me memorable when David had an off-market deal that was too small for his portfolio.”

Ways to provide value as a beginner off-market deal investor:

“Every experienced investor remembers what it was like being a beginner,” Michael said. “When you show you’re willing to help the community rather than just take, people want to see you succeed.”

Lesson 3: Get Specific About Your Off-Market Deal Criteria

Michael’s turning point came when David asked what he was looking for and Michael couldn’t give a specific answer beyond “a good deal.”

“David helped me get specific—exact property type, specific neighborhoods, defined price range, clear cash flow target,” Michael recalled. “Once I had that specific buy box, I created business cards and everyone knew exactly what off-market deals to send me.”

The power of specificity:

“When you say ‘I’m looking for off-market deals,’ nobody remembers you,” Michael said. “When you say ‘I’m looking for 3-bedroom single-family homes in these three ZIP codes between $280-350K that cash flow $300+ monthly,’ people remember you.”

Lesson 4: Speed Matters With Off-Market Deals

When David called about the off-market deal, Michael acted within hours—not days or weeks.

“Off-market deals move faster than MLS properties because there’s no listing period,” Michael explained. “If I’d said ‘Let me think about it for a few days,’ another investor would have grabbed it.”

Michael’s speed playbook:

Within 2 hours of hearing about off-market deal:

Within 24 hours:

“Speed doesn’t mean being reckless,” Michael said. “It means being prepared so you can move quickly when the right off-market deal appears.”

Lesson 5: Solve the Seller’s Problem, Not Just Negotiate Price

Michael’s successful negotiation came from understanding the seller’s true priorities beyond price.

“The seller needed certainty, speed, and simplicity more than maximum price,” Michael said. “When I structured my offer to solve his housing transition problem with 45-day post-close occupancy, that was worth more than $20,000 in price negotiations.”

Questions to ask sellers of off-market deals:

“When you understand seller motivations, you can structure off-market deals that create value beyond just price,” Michael explained. “Win-win negotiations beat haggling every time.”

Lesson 6: Conservative Analysis Prevents Expensive Mistakes

Michael ran the numbers multiple ways before making his offer, using conservative assumptions throughout.

“I assumed higher maintenance costs than needed, included vacancy reserve even though tenant was staying, and modeled different purchase price scenarios,” Michael said. “This conservative analysis prevented me from overpaying or buying an off-market deal that couldn’t actually cash flow.”

Michael’s analysis discipline:

“I’d rather be conservative and pleasantly surprised than optimistic and financially stressed,” Michael said.

Lesson 7: The First Off-Market Deal Is About Education, Not Maximizing Returns

Michael’s cash flow in year one was modest—$553 total for the year. But he valued the education as much as the returns.

“My first property taught me tenant screening, lease agreements, maintenance coordination, expense tracking, rent collection systems, and dealing with small repairs,” Michael said. “Those skills are worth far more than a few hundred dollars monthly because they let me scale confidently.”

What Michael learned from his first off-market deal:

“Property number one is your MBA in real estate investing,” Michael said. “You’re paying tuition through modest returns and time commitment, but you’re learning skills that make properties 2, 3, and 4 much easier.”

Lesson 8: Network Consistently, Not Just When You Need Something

After buying his property, Michael continued attending REIA meetings monthly.

“I still go to REIA even though I own my property,” Michael said. “I’m building relationships for off-market deals 2, 3, and 4. Networking is a long-term relationship strategy, not a one-time transaction.”

Michael’s ongoing networking approach:

“The investors with the best off-market deal flow are the ones who show up consistently for years,” Michael said. “You can’t network only when you need something. You network because you’re part of a community.”

Lesson 9: Documentation and Systems Enable Scale

From day one, Michael documented everything systematically.

“I tracked every expense, saved every receipt, recorded every maintenance issue, and documented every tenant communication,” Michael said. “These systems mean I can scale to multiple properties without chaos.”

Michael’s documentation systems:

“Systems beat motivation,” Michael explained. “When you have systems, managing properties becomes process-driven rather than dependent on remembering everything.”

Lesson 10: Leverage Every Success for the Next Opportunity

Michael’s first off-market deal success opened doors for future opportunities.

“Now when I attend REIA meetings or talk to investors, I’m not just the beginner,” Michael said. “I’m the investor who actually closed an off-market deal. That credibility changes conversations.”

How Michael leverages his first success:

“Every property makes the next property easier,” Michael said. “Your first off-market deal proves you’re not just browsing—you’re a real investor who executes.”

Michael isn’t stopping at one property. His first off-market deal success has created momentum toward building a multi-property portfolio.

Year 2 Goals:

Property #2 using cash-out refinance equity extraction:

Michael plans to use a cash-out refinance on his current property to fund the initial capital for property #2.

“My property purchased at $285,000, appraised at $325,000, and is now worth approximately $338,000 based on recent comps,” Michael explained. “I owe $210,000 on my loan. If I refinance at 75% loan-to-value, I can access approximately $35,000 in equity to use as initial capital on property #2.”

Cash-out refinance math:

“The cash-out refinance will increase my monthly financing cost on property #1 slightly,” Michael said. “But the additional cost is more than offset by cash flow from property #2. This is how investors scale—they recycle equity rather than needing new savings for every property.”

Continued REIA networking for off-market deal #2:

Michael continues attending REIA monthly and has established himself as a credible buyer.

“Now when wholesalers and investors have off-market deals, they think of me because I’ve proven I analyze properties thoroughly and close transactions quickly,” Michael said. “My reputation for executing is my biggest asset for finding property #2.”

Potentially hiring property management:

“Once I have 2-3 properties, I’ll likely hire professional property management,” Michael said. “Right now I’m self-managing to learn the business and maximize cash flow. But eventually my time is better spent finding off-market deals #3, #4, and #5 than handling maintenance calls.”

Five-Year Vision:

Michael’s goal is owning 5-7 rental properties by age 37.

Projected portfolio in 5 years:

“If each off-market deal generates modest cash flow and appreciates reasonably, I’ll have substantial equity and passive income within five years,” Michael said. “But it all started with showing up consistently to REIA meetings and building genuine relationships.”

Michael’s Advice to Aspiring Off-Market Deal Investors:

“Stop browsing Zillow and start attending your local REIA meetings,” Michael said. “Find one meeting, put it on your calendar for the next six months, and commit to showing up consistently regardless of immediate results. Provide value to the community before asking for help. Get specific about your buy box criteria. Move fast when opportunities appear. And remember—your first off-market deal is about education as much as returns.”

Understanding DSCR loan meaning will help Michael as he scales to multiple properties and wants to qualify based on property cash flow rather than personal income.

At Stairway Mortgage, we understand that off-market deals often move quickly and require flexible, responsive financing.

We helped Michael by:

Fast pre-approval before property search:

Michael was pre-approved and ready to act immediately when David called about the off-market deal. We provided clear guidance on purchase price limits, initial capital requirements, and qualification criteria so Michael knew his boundaries before searching.

Education on investment property financing:

We walked Michael through conventional loan requirements for investment properties so he understood what properties would qualify before making offers on off-market deals.

Quick closing timeline (21 days):

When Michael found his off-market deal with a motivated seller needing fast close, we moved quickly through underwriting to meet his timeline. This responsiveness helped Michael compete against all-cash offers.

Rental income consideration:

Because Michael’s property had an existing tenant with a lease, we could count 75% of the rental income in his debt-to-income calculation, making qualification easier.

Planning for future growth:

We’re already discussing cash-out refinance options so Michael can extract equity for property #2. We provide long-term partnership, not just one-time transactions.

For first-time investors building off-market deal sourcing strategies, we offer:

Fast pre-approvals – Be ready to act within 24-48 hours when off-market deals appear

Investment property expertise – We understand the unique challenges of off-market deal financing across multiple loan programs

Education on deal analysis – We help you understand how lenders evaluate properties so you make sound financial decisions on off-market deals

Flexible financing options – As you scale your off-market deal portfolio, we have programs that grow with you

Quick response times – Off-market deals move fast, and we move fast too

Partnership approach – We educate you on financing strategies that help you build wealth through off-market deals, not just push loans

Ready to start finding off-market deals through relationship building?

Get pre-approved so you’re ready to act when opportunities appear, or schedule a call to discuss financing strategies for your first investment property purchased through off-market deal networking.

Like Michael, your first off-market deal probably won’t come from Zillow—it will come from relationships you build in your local investing community. We help you be financially ready when those relationships produce opportunities.

An off-market deal is a property that sells without being publicly listed on the Multiple Listing Service (MLS) or major real estate websites like Zillow or Realtor.com. These properties typically sell through direct relationships between buyers and sellers, often facilitated by investors, wholesalers, or agents specializing in off-market deals.

The key differences between off-market deals and MLS properties:

Competition: Off-market deals typically have few or no competing buyers, while MLS properties often receive multiple offers within days. This lack of competition often allows off-market deal buyers to negotiate better pricing and terms.

Timing: Off-market deals move faster because there’s no listing period, professional photography, or open houses required. Sellers choosing off-market deals usually prioritize speed and certainty over maximum price.

Pricing: Off-market deals are often priced below market value because sellers save on agent commissions and accept lower prices in exchange for convenience and quick closing.

Access: You can’t find true off-market deals through online searches—they come exclusively through personal relationships with wholesalers, other investors, agents, or property owners directly.

Michael’s off-market deal came through REIA networking, sold $40,000 below comparable MLS properties, and closed in 21 days without competition. This is typical of off-market deal transactions.

Michael’s timeline was four months of consistent REIA networking from first meeting to closing his off-market deal, but timeframes vary significantly based on several factors.

Factors affecting off-market deal timeline:

Networking consistency: Attending monthly meetings consistently (like Michael did) builds relationships faster than sporadic attendance. Most successful off-market deal investors attend every meeting for at least 3-6 months before seeing results.

Value provided: Investors who contribute to the community (like Michael’s website redesign) become memorable faster than those who only ask for deals.

Market conditions: In competitive markets with high demand, off-market deals move even faster once you find them. In slower markets, you may find opportunities more quickly but at different pricing.

Buy box specificity: Having specific criteria (like Michael’s detailed buy box) makes it easier for people to remember you and send relevant off-market deals your way.

Network size: Larger real estate investing associations with 100+ active members generate more off-market deal flow than smaller groups with 20-30 members.

Realistic expectations for finding your first off-market deal:

“I attended REIA for four months before finding my off-market deal, but I was building relationships the entire time,” Michael said. “If you’re going to networking events expecting immediate results, you’ll be disappointed. Think 6-12 month timeline realistically.”

The investors who find off-market deals fastest are those who commit to consistency regardless of immediate results.

Michael’s off-market deal required 25% initial capital ($71,250) because he used a conventional investment property loan, which is standard for non-owner-occupied properties with excellent credit.

However, several financing options allow lower initial capital on off-market deals:

Lower initial capital financing strategies:

House hacking with FHA loan (3.5% initial capital):

Purchase a 2-4 unit property as your primary residence using an FHA loan, live in one unit, and rent the others. You can often find small multifamily off-market deals through the same REIA networking.

Example: $300,000 duplex with 3.5% FHA = $10,500 initial capital

VA loan for veterans (0% initial capital):

Veterans and active military can purchase properties with VA loans requiring zero upfront capital. While primarily for primary residences, you can house hack a multifamily property or later convert it to rental after moving.

Conventional primary residence (5-10% initial capital):

Purchase an off-market deal as your primary residence with conventional financing requiring 5-10% initial capital, live in it for at least a year, then convert to rental when you purchase your next primary residence.

Seller financing (negotiated terms):

Some off-market deal sellers are willing to provide financing directly, allowing you to negotiate initial capital percentage, terms, and interest rates. This works best when sellers own properties free and clear.

Example: $285,000 off-market deal with seller carrying $240,000 note at 6% interest, buyer provides $45,000 (15.8%) initial capital

Partnerships (split initial capital requirement):

Partner with another investor to split the required initial capital and jointly purchase off-market deals. Each partner might contribute 12.5% instead of 25% solo.

DSCR loans (variable initial capital, typically 20-25%):

DSCR loans qualify based on property cash flow rather than personal income and typically require 20-25% initial capital. Useful for off-market deal investors who are self-employed or have complex income.

“I used conventional 25% initial capital because I had stable W-2 income and good credit,” Michael said. “But I know investors who found off-market deals and used FHA house-hacking with only 3.5% initial capital. Explore options based on your situation.”

Finding quality real estate investing associations where off-market deals are shared is essential for building your network.

Resources for finding REIA meetings and investment groups:

National REIA website: Visit nationalreia.org and use their “Find a Local REIA” search tool. This database includes hundreds of affiliated real estate investing associations across the United States.

Meetup.com: Search for “real estate investing,” “rental property,” or “off-market deals” in your city on Meetup.com. Many cities have multiple investing groups meeting monthly.

Facebook groups: Search Facebook for “[Your City] Real Estate Investing” or “[Your City] Rental Property Investors.” Many groups announce monthly meeting schedules and off-market deal opportunities.

BiggerPockets local forums: The BiggerPockets website has local forums for most major markets where investors share information about meetings, events, and off-market deal networking opportunities.

Ask local agents and investors: Real estate agents specializing in investment properties usually know which REIA meetings are most active. Ask agents, property managers, or investors you meet where they network for off-market deals.

Google search: Search “[Your City] real estate investors association” or “[Your City] REIA meeting” to find local groups.

What to look for in quality REIA meetings for off-market deals:

Meeting size: Groups with 50-100+ attendees typically have more off-market deal flow than small groups with 10-20 members.

Active investors: Best meetings have experienced investors actively purchasing properties, not just beginners or people selling courses.

Networking time: Meetings should include dedicated networking time, not just presentations. Off-market deals come from relationships built during networking.

Local focus: Groups focused on your specific local market (not national strategies) provide better off-market deal opportunities and relevant market information.

Regular schedule: Monthly meetings on consistent schedule (like third Thursday every month) make it easy to commit to consistent attendance.

Wholesaler attendance: Meetings where wholesalers share off-market deals with the group tend to have higher deal flow than meetings focused only on education.

“I found Austin REIA through Google search and visited once to see if it was legitimate,” Michael said. “After seeing 100+ investors, experienced presenters, and active off-market deal discussions, I committed to attending every month. Visit a few meetings before deciding which group to commit to long-term.”

Michael faced exactly this situation—the seller initially thought his property was worth $370,000 when comparable sales showed $330,000-$338,000 market value. Here’s his approach to negotiating off-market deals respectfully:

Professional negotiation strategies for off-market deals:

Step 1: Prepare objective data

Create a simple one-page comparable sales analysis showing:

“I showed the seller clear evidence rather than just saying ‘Your price is too high,'” Michael said. “Data is less personal than opinions.”

Step 2: Lead with understanding

Begin negotiations by acknowledging the seller’s perspective and situation before discussing price:

“I understand you were thinking around $370,000 based on online estimates. I’d like to share the recent comparable sales I researched in your neighborhood so we’re both working from the same market data.”

This approach shows respect for the seller’s position while introducing objective information about the off-market deal value.

Step 3: Focus on non-price value

Emphasize benefits beyond purchase price that off-market deal sellers value:

Certainty: Pre-approved financing, strong financial profile, no financing contingency risk

Speed: Quick close (14-30 days), flexible timing to match seller’s needs Convenience: No showings, no open houses, no agent coordination required

Simplicity: Minimal contingencies, straightforward transaction, easy communication Flexibility: Post-close occupancy, solving timing problems, creative terms

“When I offered the seller 45 days post-close occupancy, that solved his California transition problem and was worth more than $20,000 in price,” Michael explained. “Look for ways to add value beyond the purchase price on off-market deals.”

Step 4: Explain your offer rationale

Don’t just state your offer price—explain the thinking behind it:

“Based on the three comparable sales showing $328K-$338K, and accounting for your property’s good condition, I’m offering $285,000. This is below the comps because you’re saving approximately $20,000 in agent commissions and getting certainty of close within 21 days. My offer reflects market value minus the costs you’re avoiding through this off-market deal.”

Step 5: Stay friendly regardless of outcome

If the seller rejects your offer or counters too high on the off-market deal:

“I appreciate you considering my offer. I understand if the price doesn’t work for your situation. Please keep my contact information—if circumstances change or you don’t find another buyer, I’d be happy to revisit this conversation. I wish you the best with the sale.”

This leaves the door open for the seller to come back later if their off-market deal falls through or expectations change.

“I negotiated respectfully and never made the seller feel like I was trying to take advantage of him,” Michael said. “Even when we had a $85,000 gap between his expectation ($370K) and my offer ($285K), I stayed friendly and used objective data. That professionalism helped us find common ground and close the off-market deal successfully.”

Building your off-market deal network and investing skills? These resources provide additional depth:

Also helpful for first-time off-market deal investors:

Financing options for off-market deals:

Different off-market deal sources and property types require different financing approaches: