“I think I’ll wait until the market cools down.” “I want to save more first.” “I’ll buy next year — when rates drop.”

These are all valid thoughts. But here’s the problem: the market doesn’t wait.

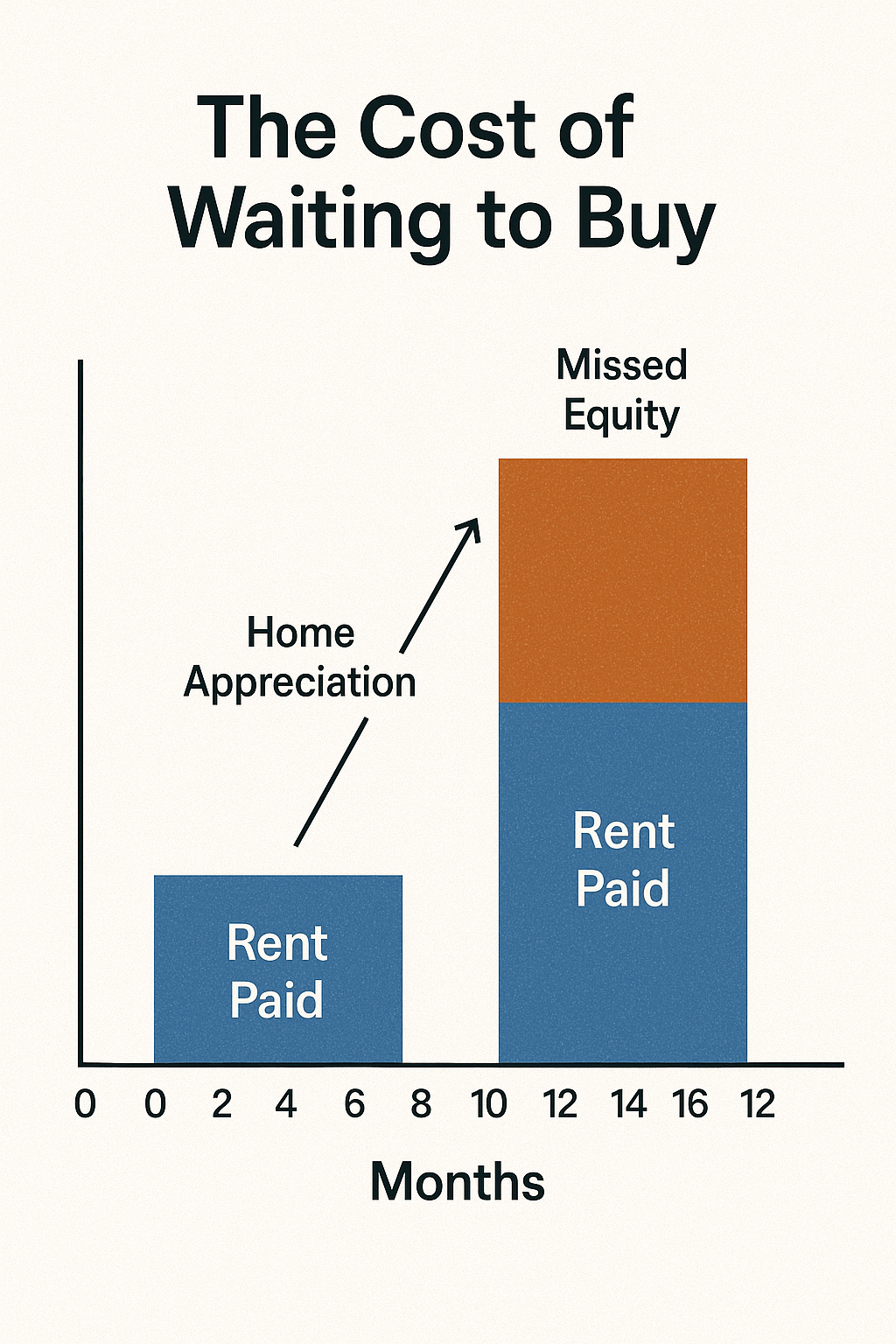

And the cost of waiting to buy a home is often far higher than people realize — especially when you factor in appreciation, rent payments, and missed equity.

Let’s break it down.

1. Home Prices Rarely Drop Long-Term

Even if prices slow temporarily, history shows that real estate almost always trends up over time.

The longer you wait, the less your savings are worth. That $50,000 down payment you’re building? It buys less each year.Meanwhile, home values and construction costs rise — meaning:

You may get less house later

You may have less control over the transaction

And you’ll face more competition from buyers who act sooner

4. Rates Can Go Up, Too

Everyone’s hoping rates drop. But what if they don’t?

Or worse… what if they go up first?

Higher rates + higher home prices = significantly higher monthly payments Even a 1% rate increase can mean hundreds more per month.

If limited savings are your reason for waiting, explore accessible options now. Calculate your FHA Purchase Loan Payment now to see how 3.5% down makes buying possible sooner rather than waiting years to save 20%.

You Don’t Have to Rush — But You Should Run the Numbers

If you’re waiting because you’re uncertain — that’s fair. But if you’re waiting because you think it’s “cheaper” later… that’s worth a second look.

Let us run a few real-world projections for you. You might be closer than you think.

Want to find out if waiting is helping or hurting your wealth plan?

At Stairway Mortgage, we help you understand the true cost of waiting—so timing decisions are based on math, not fear.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.