1099 Mortgage Loans | Buy a Home Without W-2s or Tax Returns

Qualify Using Your 1099 Forms—Not Your Tax Returns. No W-2s Required. As Little as 10% Down.

You’re a High-Earner—but You Don’t Have W-2s. That’s Where This Loan Comes In.

If you’re a contractor, gig worker, or freelancer earning great income but struggling to show it on paper, a 1099 income loan might be exactly what you need.

Instead of using tax returns or pay stubs, this loan qualifies you based on your 1099 forms and/or bank deposits—giving you a flexible, realistic way to buy or refinance.

What Is a 1099 Mortgage Loan?

A 1099 mortgage is a type of Non-QM (Non-Qualified Mortgage) loan that allows independent contractors or self-employed workers to qualify using:

- Yearly 1099 forms

- Or monthly bank deposits that match your contract income

It’s designed specifically for those who earn consistently but don’t fit into a W-2 box.

Common 1099 Professions:

- Realtors

- Consultants

- Insurance agents

- Uber/Lyft drivers

- Nurses & traveling medical staff

- Construction contractors

- Creatives: photographers, designers, musicians

How Does a 1099 Mortgage Loan Work?

Unlike conventional mortgages that rely heavily on W-2 income verification and two years of tax returns, a 1099 mortgage loan uses a simplified income calculation method. Here’s the typical process:

Income Verification Options:

- 1099 Form Method – Lenders review your most recent 12-24 months of 1099 forms and calculate an average of your gross receipts

- Bank Statement Method – Some 1099 mortgage loan programs also accept 12-24 months of bank statements showing consistent deposits

The key advantage? Your income is calculated before business deductions, giving you a much higher qualifying amount than traditional mortgage programs that use your adjusted gross income (AGI).

What Do Lenders Look For in a 1099 Borrower?

Lenders offering 1099 income loans typically want to see:

- 12–24 months of 1099s

- Or bank statements matching the deposits

- Credit Score: 620+ (some prefer 680+)

- Down Payment: 10–20%

- Clean credit with no recent major delinquencies

- Strong DTI (below 45% preferred)

Don’t have 1099s but have great cash flow? Check out Bank Statement Loans.

Key Benefits of a 1099 Mortgage Loan

Choosing a 1099 mortgage loan offers several advantages for self-employed and contract workers:

No Tax Return Required – Your 1099 forms tell the income story, so aggressive write-offs won’t hurt your qualification. This is perhaps the biggest benefit of a 1099 mortgage loan for self-employed borrowers.

Faster Processing – Without the need to analyze complex Schedule Cs, profit and loss statements, or multiple years of business tax returns, 1099 mortgage loans often close faster than traditional self-employed mortgages.

Higher Qualifying Income – Because the 1099 mortgage loan uses gross income rather than net income after deductions, most borrowers qualify for significantly more home than they would with a conventional loan.

Flexible Documentation – Many 1099 mortgage loan programs accept alternative documentation like signed contracts or CPA letters to support your income claims.

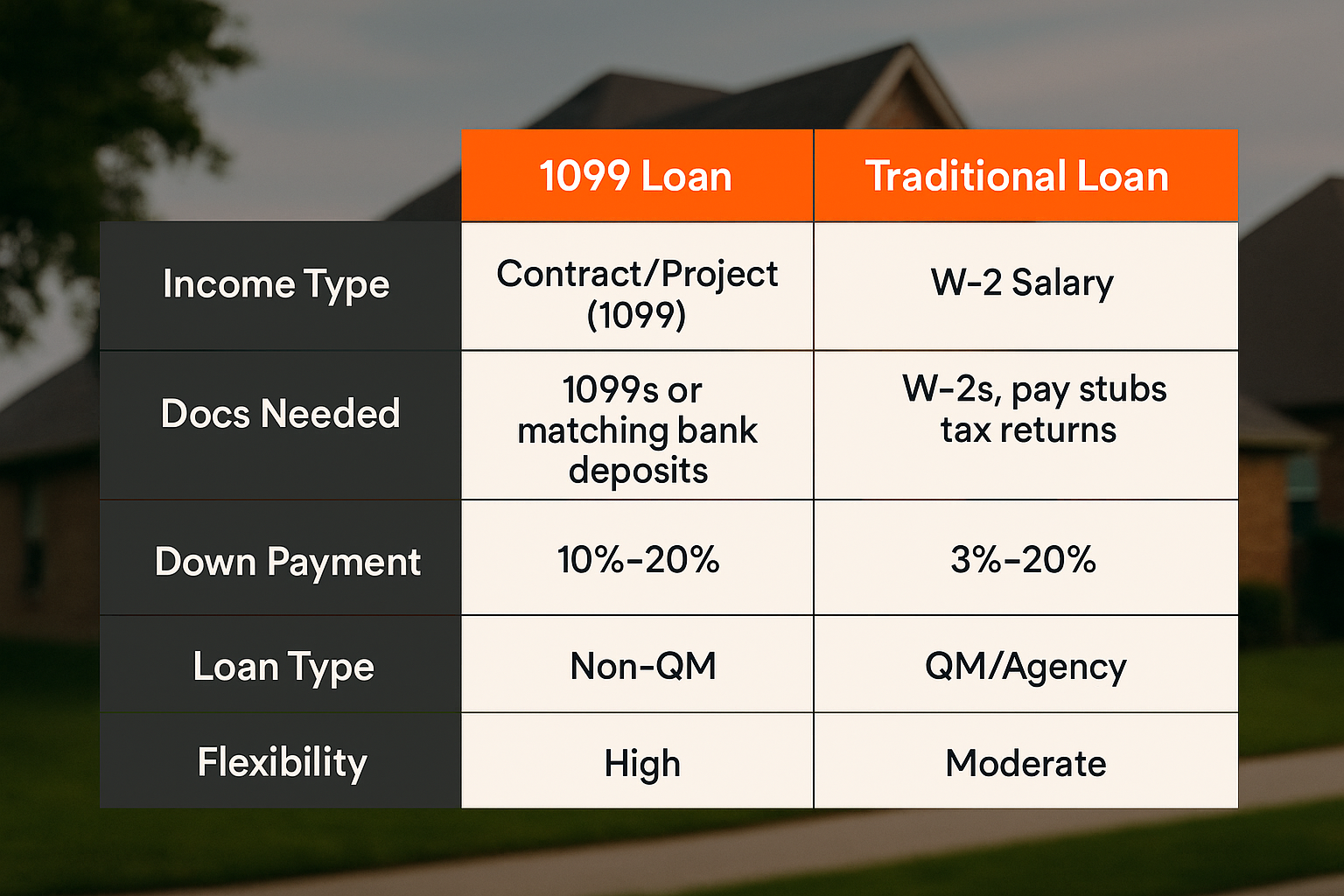

1099 Mortgage Loan vs. Traditional Self-Employed Mortgage

Understanding how a 1099 mortgage loan differs from conventional self-employed financing helps you choose the right path:

| Feature | 1099 Mortgage Loan | Traditional Self-Employed Loan |

|---|---|---|

| Tax Returns | Not required | 2 years required |

| Income Calculation | Gross 1099 income | Net taxable income (AGI) |

| Documentation | 1099 forms + deposits | Full tax returns + P&Ls |

| Processing Time | 2-3 weeks typical | 30-45 days typical |

| Business Deductions | Don’t reduce qualifying income | Reduce qualifying income |

For many contractors and 1099 workers, a 1099 mortgage loan is simply more realistic. It recognizes that business deductions are smart tax planning—not a sign of weak income.

Who Should Consider a 1099 Mortgage Loan?

A 1099 mortgage loan makes the most sense for:

- Independent contractors with 12+ months of consistent 1099 income who take significant business deductions

- Commission-based professionals like real estate agents or insurance brokers whose income fluctuates but averages strong

- Gig economy workers with multiple 1099 income streams from platforms like Uber, DoorDash, or Upwork

- Self-employed individuals who have been denied by traditional lenders due to low taxable income

- First-time homebuyers who are self-employed and don’t have a long business history

If you’ve been told “your income doesn’t qualify” even though you know you earn enough to afford the home, a 1099 mortgage loan likely offers a solution.

Ready to Apply for a 1099 Mortgage Loan?

Stop letting your 1099 status hold you back from homeownership. Whether you’re buying your first home, upgrading to a larger property, or investing in real estate, a 1099 mortgage loan can help you get approved based on your actual earning power.

Want to see a real-world example? Read our 1099 mortgage loan case study to see how Nathan, an independent sales contractor, bought his Phoenix home in just 21 days.

Curious about your numbers? Use our 1099 mortgage calculator to estimate your qualification amount and monthly payment.

Have questions about whether a 1099 mortgage loan is right for you? Contact our team of Non-QM specialists today.

Just Because You’re 1099 Doesn’t Mean You’re Not Qualified

You work hard, earn well, and manage your finances like a pro. It’s time your mortgage options recognized that. A 1099 income loan helps you buy a home using real-world income—not outdated paperwork.

Book Your 1099 Income Loan Strategy Call Today

Ready to Take Your First Step?

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.

- Takes just 5 minutes

- Tailored results based on your answers

- No credit check required

Need a Pre-Approval Letter—Fast?

Buying a home soon? Complete our short form and we’ll connect you with the best loan options for your target property and financial situation—fast.

- Only 2 minutes to complete

- Quick turnaround on pre-approval

- No credit score impact

Got a Few Questions First?

Let’s talk it through. Book a call and one of our friendly advisors will be in touch to guide you personally.