Save $400+/Month with a Conventional Refinance: This Couple Did It—Here’s How

By

Jim Blackburn

on

Client Profile

Names: Jasmine & Tyler B.

Ages: 34 & 36

Location: Denver, CO

Home Type: 3-bed single-family home

Original Loan: FHA at 4.75% with monthly PMI

New Loan: Conventional 30-Year Fixed at 5.375%

Equity at Time of Refi: 21%

Monthly Savings: $412

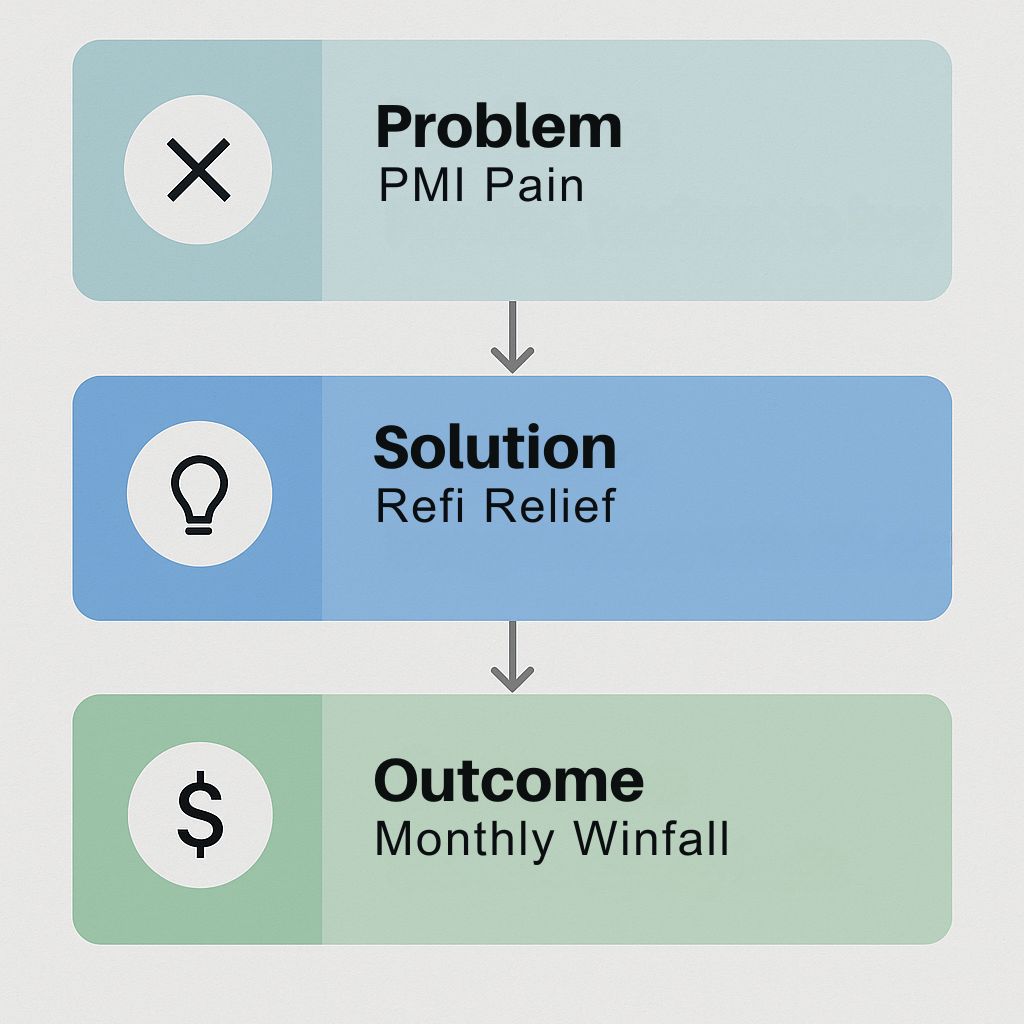

The Challenge

Jasmine and Tyler had purchased their home three years earlier with an FHA loan. While the interest rate was decent, the $188/month in mortgage insurance was dragging down their cash flow.

They’d improved their credit and their home had appreciated—but they weren’t sure if they had enough equity to drop PMI or if it made sense to refinance.

The Strategy

We ran a value check and found their home had appreciated from $385K to $495K—giving them enough equity to refinance into a conventional loan with no PMI.

We structured:

New 30-year conventional fixed loan

No private mortgage insurance

Lender credit to offset closing costs

Slightly higher rate but significantly lower monthly cost

The Outcome

Monthly mortgage dropped from $2,215 to $1,803

PMI was completely eliminated

Closing costs were fully offset through lender credits

The couple is saving $412/month, which they now invest in retirement accounts

Quote from Jasmine:

“We didn’t know we could get rid of PMI. We were just hoping to shave off $100. This refinance gave us so much more breathing room.”

Ready to Take Your First Step?

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.