Paying points is like investing in a lower monthly cost. It can be a smart move if:

You plan to stay in the home (or hold the loan) for 7+ years

You want to lower your monthly payment for budget reasons

You’re locking in a rate in a rising-rate environment

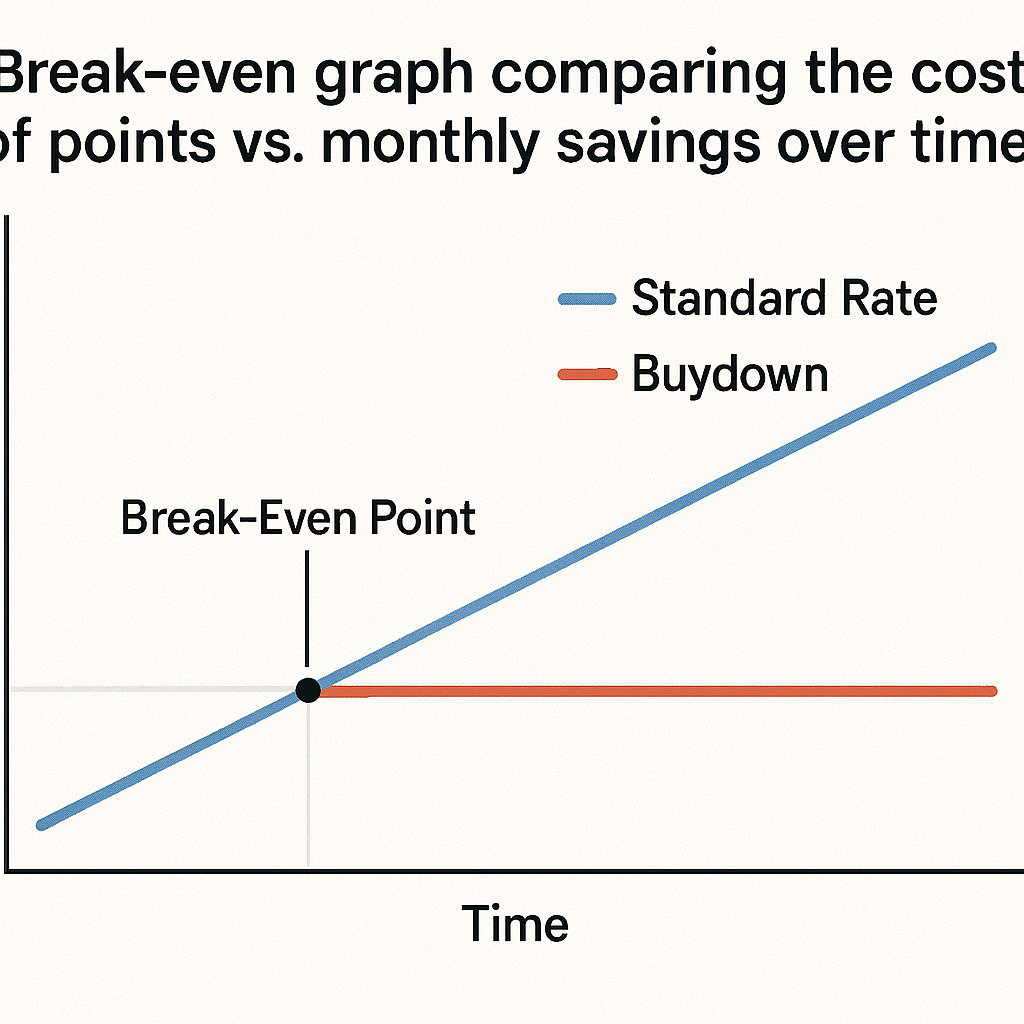

What’s the Break-Even Point?

Here’s the key question: How long will it take for the monthly savings to equal the cost you paid upfront?

Example:

Pay $4,000 to reduce rate by 0.375%

Save $75/month

Break-even = 54 months (~4.5 years)

If you’ll keep the loan longer than 4.5 years? You win. Sell or refinance earlier? You may not recoup the cost.

Understanding your complete loan structure helps with the points decision. Calculate your Conventional Purchase Loan Payment now to see how different rate and point combinations affect your monthly payment and total loan costs.

When NOT to Pay Points

Paying points may not be smart if:

You’re buying a starter home and plan to move in a few years

You think you’ll refinance soon (if rates drop or income improves)

You’d rather keep cash for renovations, investments, or reserves

Also: Some lenders pitch points as a profit tool — not a strategy. That’s why it helps to work with a team that runs the math with your goals in mind.

Points Are a Strategy, Not a Requirement

You don’t have to buy down your rate. But in the right situation, it can create serious savings.

Let’s help you figure out if it makes sense — or if your money is better used elsewhere.

Need help evaluating whether to pay points? Visit our Buy a House page for comprehensive resources about mortgage strategies, rate structures, and making informed financing decisions.

Want help comparing options?

At Stairway Mortgage, we help you make strategic decisions about points, rates, and loan structure based on your actual timeline and goals.

Skip the guesswork. Take our quick Discovery Quiz to uncover your top financial priorities, so we can guide you toward the wealth-building strategies that fit your life.